SURVEY: Manufacturing Supply Disruptions to Last Well Into 2023

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

SURVEY: Future Outlook: Hazy

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

Manufacturing’s Sustainability Challenge: The Race is On

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

Pedal to the Metal

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

Growing Pains

Manufacturers see data’s massive potential to improve operations, predict disruptions, and bring about new revenue streams, but realizing that promise continues to be a work in progress.

![]()

Data could be described as the lifeblood that enables the digital enterprise. In the 18-plus months that the COVID-19 pandemic has been roiling supply chains, forcing once-live interactions to go virtual, and necessitating remote work and collaboration, manufacturers have seen the immense value of using data to keep operations going and make better-informed decisions. It isn’t hard to imagine a far worse scenario if this once-in-a-generation disruption had happened in a time of less (or no) digital maturity.

But while former IBM CEO Ginni Rometty once said that big data is the new oil, a more apt comparison might be that data is like sunlight – in infinite supply, unyielding, quite often blinding. But it can also be illuminating, shedding light on former dark spots by improving transparency and visibility, enabling businesses to grow and thrive.

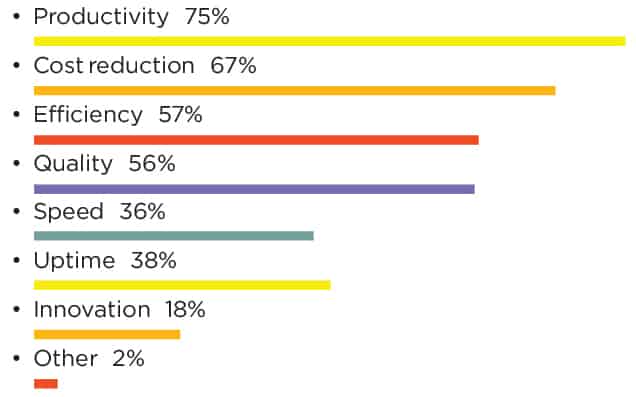

Manufacturing data mastery is in its tween years for most enterprises – certainly past its infancy, but still awkward and gawky and not quite fully formed. It is often unclear who is responsible for data strategy, what the data strategy is, or what data is actually worth to an organization. But manufacturers also say data has helped them to grow their productivity, lower their costs, boost efficiency, and improve quality.

These findings and others from the MLC’s new M4.0 Data Mastery Survey provide insights on where manufacturers are on their journey to harness the power of data and its revolutionary promise.

Where Improvement is Needed

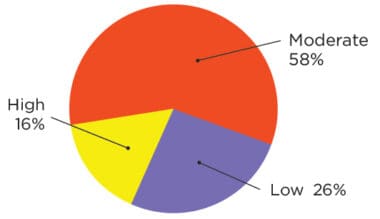

Most manufacturers rate themselves as just average at their organizational data skills, and they struggle not only to collect the right data but also to interpret it. Fifty-eight percent said that their company had just a moderate ability to collect data that is meaningful and impactful for their business needs (Chart 11). More than a quarter ranked themselves as low in this area.

It is often unclear who is responsible for data strategy, what that strategy is, or what organizational data is actually worth.

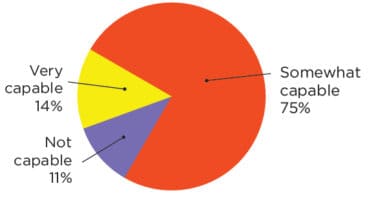

But data collection is not the greatest struggle. Even more respondents said they had room for improvement in terms of finding insights from that data, with 75% ranking their organizations as only somewhat capable in their ability to analyze their manufacturing operations data (Chart 12). In this area, 11% of respondents said their organizations were not capable of this type of analysis.

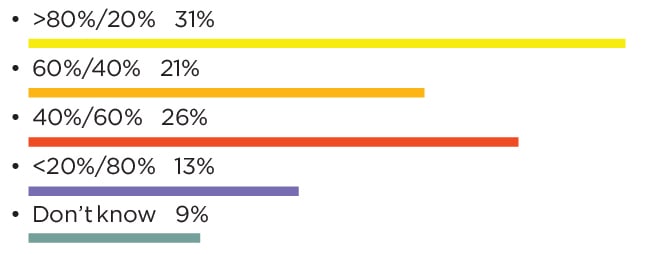

Furthermore, a gap remains between the effort to collect and sort data and the effort to apply insights and create value from that data. Almost a third said they expend greater than 80% effort in gathering and organizing data vs. the effort expended to analyze and apply insights from the data (Chart 8).

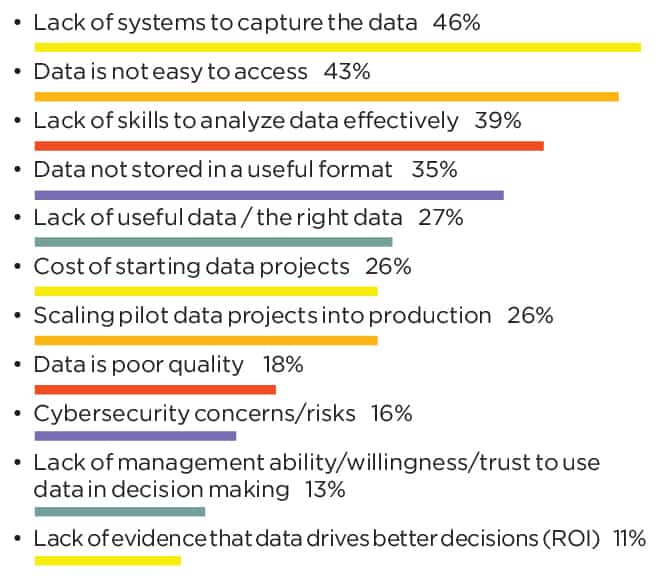

Other stumbling blocks to utilizing data to a greater extent speak to the unwieldy tangle that manufacturers often find when undertaking data projects. This includes a lack of systems to capture the data (46%), followed by data inaccessibility (43%) and a lack of skills to effectively analyze data (39%) (Chart 16).

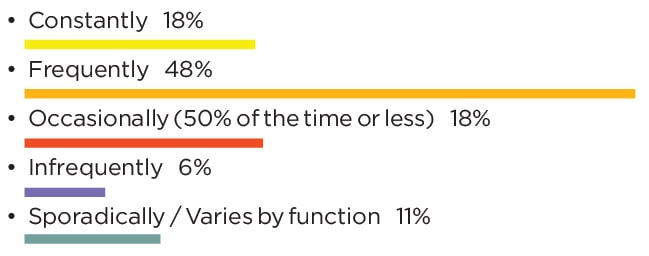

However, for what they are able to collect and analyze, more often than not organizations are leveraging that data to make informed decisions. Forty-eight percent say that their organization makes data-driven decisions frequently, while 18% say that they make data-driven decisions constantly (Chart 13).

Tools of Collection and Analysis

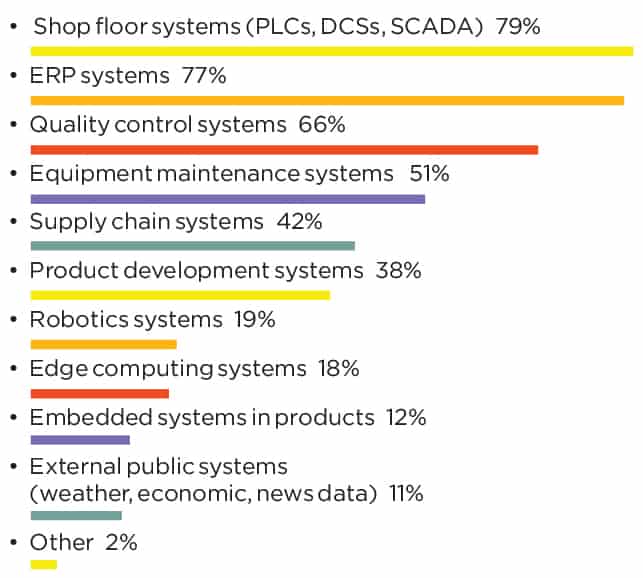

Digging a bit deeper into organizational data tactics, 79% said their shop floor systems are the primary source of manufacturing data, followed closely by ERP systems at 77% (Chart 6). This may not be surprising given the near-ubiquitous nature of those technologies within many manufacturing facilities.

What could be a trend to watch, though, is the growing use of edge computing systems (18%) and even embedded systems in products (12%). The former shows that manufacturers are taking advantage of faster networking technologies to process and store data closer to where it is produced and consumed, while the latter could hold promise for monitoring product lifecycle and performance, in addition to sustainability by making products more efficient and reducing materials usage and waste.

“Manufacturing organizations have serious governance issues to address, such as having a formal plan and somebody ultimately in charge of data management.

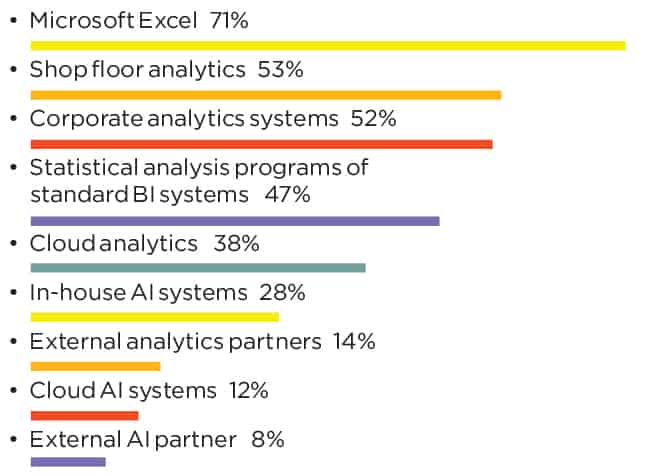

But among those emerging technologies lie some old faithful ones. CPA favorite Microsoft Excel is still the leader as the manufacturing data analysis tool of choice 34 years after its initial release, with 71% of respondents saying they use it (Chart 9). Meanwhile, AI is making inroads in its use for analysis, with nearly a third saying they are using in-house AI systems (28%), and others using cloud AI systems (12%) or an external AI partner (8%).

The Fundamental Flaws

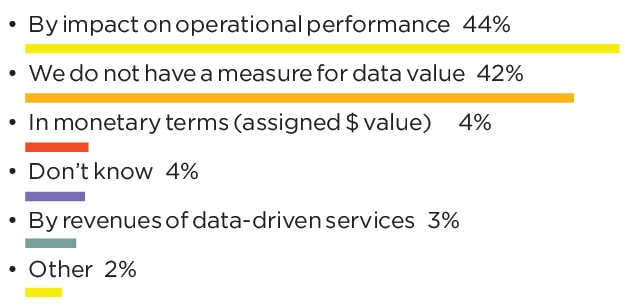

Assigning value to data is an elusive undertaking for many manufacturers. Of those who do, most measure it by impact on operational performance (44%), as it is likely the easiest way to see the results of manufacturing data projects (Chart 1). But nearly as many admitted that their organization has no measure for data value (42%), a somewhat troublesome finding given the time, resources, and effort that go into data collection and analysis.

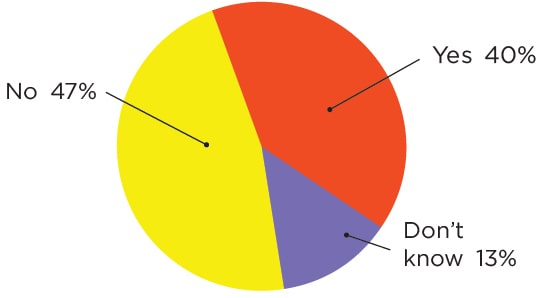

It’s difficult to determine if this is merely an oversight, or if reliable models just haven’t yet been developed to assess ROI, but this will be an important and necessary undertaking for manufacturers to make impactful data-led decisions. The good news is, though, that executives appear motivated to take on this pursuit, as 40% of respondents said data collection, management, and analysis were included as part of annual objectives for company executives (Chart 3).

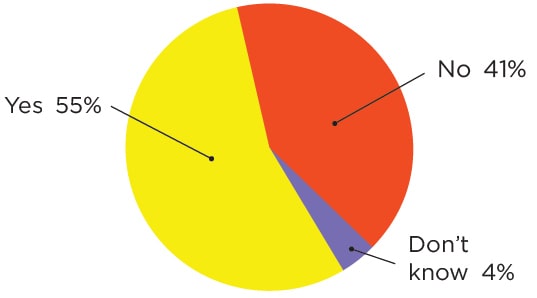

But manufacturing organizations have other serious governance issues that also must be addressed, such as having no formal plan for data management or having nobody ultimately in charge. Four out of 10 respondents said that their company had no corporate plan, strategy, or formal guidelines for how data is collected and organized across the enterprise (Chart 2), an almost-astonishing number at a time when manufacturers are making significant investments in digital technologies to build connected operations.

“In today’s algorithm-driven world, manufacturers must pay heed to data accuracy, quality, and fidelity.

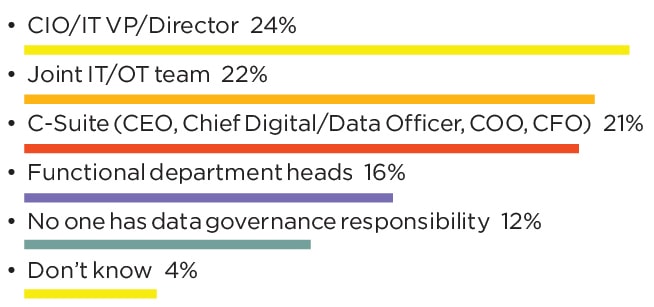

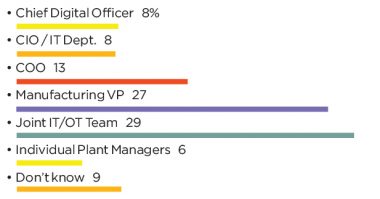

Manufacturers continue to take a scattered approach to governance and control over data, though many have a head of IT or combined IT/OT team ultimately in charge of data governance and strategy (Chart 4). However, 12% said that no one has data governance responsibility at their organization, a glaring issue that must be addressed at any company that wants to stay competitive in the long run.

Trusting the Data

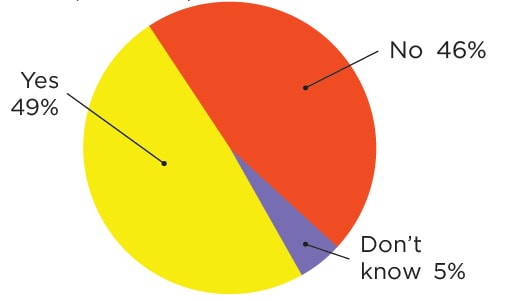

One of the oldest idioms in computer science lexicon is garbage in, garbage out, meaning that flawed input data will result in flawed output data. In today’s algorithm-driven world, manufacturers must pay heed to the accuracy, quality, and fidelity of the data they are using for all-important business decisions. But it’s nearly an even split between manufacturers who check for that accuracy – 49% saying they do vs. 46% saying they complete no such checks (Chart 10).

Whatever leads those manufacturers to believe they can trust their data, there is no question that data is driving much-improved decisions – 94% said the use of data has helped their company make better decisions, though just 35% say it has helped them to make faster decisions (Chart 15).

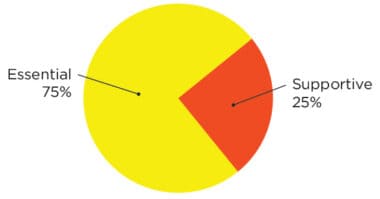

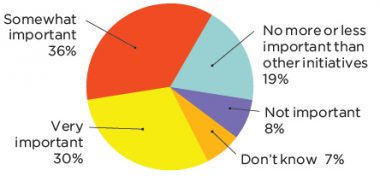

To underscore the views that manufacturers have on data’s value for competitiveness, there is little room for debate that most see it as a requirement. Seventy-five percent said that data mastery will be essential for future competitiveness, with 25% saying it will be supportive for competitiveness – and not one single respondent saying that it will have no impact at all (Chart 17).

There is little question that manufacturers see the immense value that data can bring to their businesses. As organizations grow their data competency, they will seek to move past simply monitoring and collecting data to unlocking the insights and predictive ability that will be essential to future competitiveness. But until those organizations address the fundamentals of data mastery, they are likely to feel more growing pains along the road to that promising tomorrow. M

Part 1: CORPORATE DATA GOVERNANCE & ORGANIZATION

1. Many Organizations Have No Measure for Data Value

Q: How do you measure the value of the data in your organization? (Select one)

2. Many Organizations Lack Formal Data Collection Guidelines

Q: Does your company have a corporate-wide plan, strategy, or formal guidelines for how data is collected and organized across the enterprise, including manufacturing operations? (Select one)

3. For Many, Data Mastery is an Executive Objective

Q: Is data collection / management / analysis included in some way as part of the annual objectives for company executives? (Select one)

4. CIOs, IT Teams Largely Responsible for Data Governance

Q: Who is responsible for data governance and strategy in your organization? (Select one)

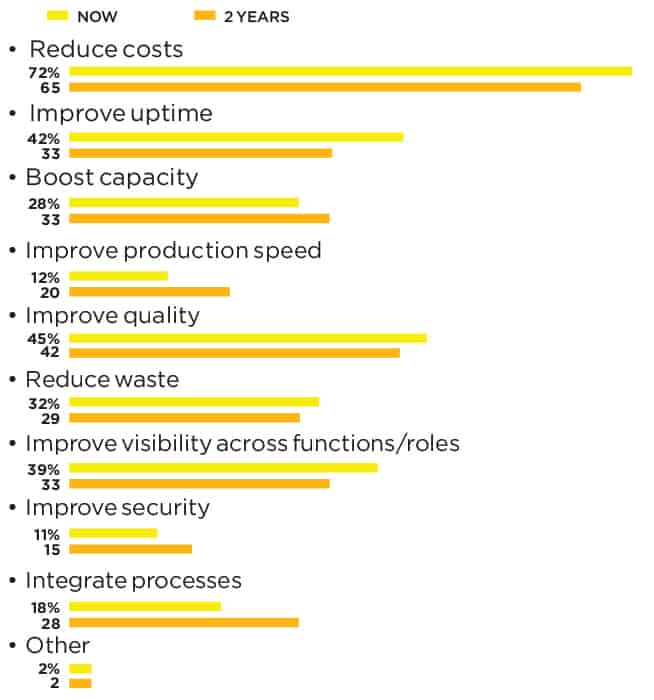

5. Cost Savings, Quality Top List of Business Objectives

Q: What are your key business outcome objectives for embarking on manufacturing data projects today and what do you expect your primary objectives to be in 2 years’ time? (Check top three for Now and top three in 2 years)

Part 2: DATA COLLECTION & ANALYSIS TACTICS

6. Shop Floor Systems, ERPs are Primary Data Sources

Q: What are the primary sources of your manufacturing data today? (Check all that apply)

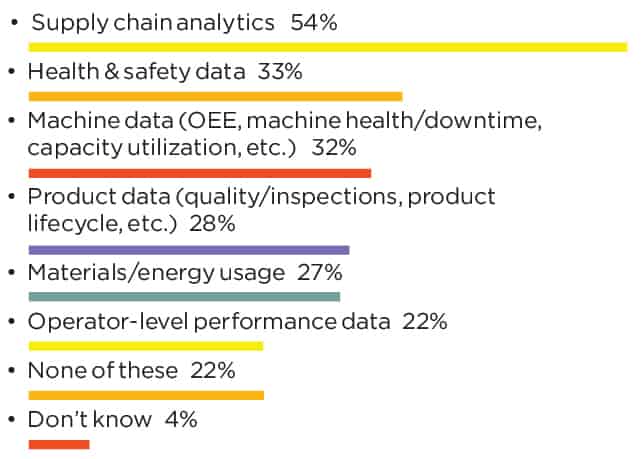

7. Pandemic Makes Supply Chain Analytics a Priority

Q: Has capturing and analyzing certain types of data become more important to your organization in the wake of the COVID-19 pandemic? (Check all that apply)

8. Gap Lies Between Data Collection and Application

Q: What is your estimate of percent effort to gather and organize data relative to the percent effort to analyze, derive insights, and apply those insights to creating value from that data? (Select one)

9. MS Excel Still Leads as Data Analysis Tool

Q: What systems do you use to analyze the manufacturing data you collect? (Check all that apply)

10. Checking Up on Data Accuracy, Quality

Q: Does your company have a process to verify the

accuracy and/or quality of the raw data before decisions are made on it? (Select one)

Part 3: ORGANIZATIONAL DATA MASTERY

11. Matching Data Collection to Business Needs

Q: How would you rank your company’s ability to collect the right data the business needs from your manufacturing operations?

12. Data Analysis Sees Room for Improvement

Q: How would you rank your company’s ability to analyze the data from your manufacturing operations?

13. Data Leads More Decisions, More Often

Q:How often would you say your organization makes data-driven decisions? (Select one)

Part 2: DATA-DRIVEN OUTCOMES & CHALLENGES

14. Data Boosts Productivity, Lowers Costs

Q: How has the increase in manufacturing data

helped you to improve your manufacturing organization? (Check all that apply)

15. Quality, Speed of Decision-Making Improves

Q: How has the use of data affected your

company’s decision-making? (Check all that apply)

16. Data Capture, AccessRemains an Obstacle

Q: What are the most important challenges or obstacles hindering your organization from making more data driven decisions? (Check top three)

17. Most See Data Mastery as Essential to Competitiveness

Q: Looking forward, how important do you think mastering manufacturing data will become to your competitiveness as a future business? (Select one)

Survey development was led by Penelope Brown, with input from the MLC editorial team and the MLC’s Board of Governors.

Reimagining the Art of the Possible

COVID has instigated a host of strategic and tactical changes in manufacturing which will be permanent features of the industrial landscape for years to come, rewriting leadership’s playbook and redefining the rules of competition.

![]()

The fallout of COVID-19 has affected many aspects of the manufacturing industry over the past year, but one of the most significant has been a heightened urgency about adopting Manufacturing 4.0 technologies and techniques to deal with what was and continues to be unprecedented business disruption.

Many manufacturing executives acknowledge that the equivalent of several years’ change has been compressed into the past year. Companies had to respond quickly to the pandemic crisis, adapting production environments, standing up new health and safety protocols, enabling more front-line workers to do their jobs remotely, and, in some cases, pivoting to produce products, such as life-saving ventilators and masks, that they had never produced before.

A key ally enabling such rapid change, many found out, was M4.0 digitization. Those that had already embraced the digital model had an easier time adapting; those that did not had greater difficulty.

For manufacturing leadership, the time has been both a test and an opportunity. Leaders have had to deal with the daily stress of keeping the business running, making sure employees were safe and engaged, and reacting to often unpredictable changes in demand. But they have also been able to arrive at a broader view of what’s possible. Now, executives across the industry are in the process of deciding what COVID-compelled changes may take root in their companies and which may not.

The Manufacturing Leadership Council’s new research survey on Next-Generation Leadership and the Changing Workforce, one of MLC’s Critical Issues facing the industry, sheds considerable light on what COVID-related changes are top of mind for leaders, how leaders are thinking about their role in the digital era, what knowledge and expertise will be needed in the future, and what key challenges they envision along the way.

New disaster preparedness, resiliency, and remote working strategies will become permanent features of manufacturing leadership’s playbook.

The Effects of COVID

MLC research over the past year has clearly documented that manufacturers want to accelerate their adoption and use of M4.0 as a direct result of the pandemic. The new Next-Generation Leadership survey reveals the implications of this tighter embrace.

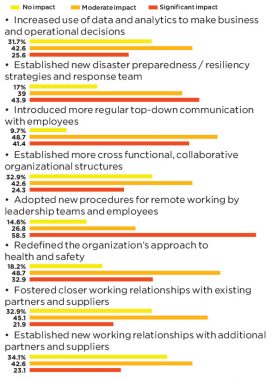

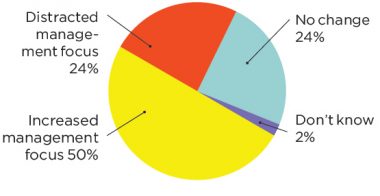

A solid majority of the new survey’s respondents, 54.8%, confirm that COVID-19 has increased management’s focus on digital transformation (chart 1). New procedures for remote working by leadership teams and employees, new disaster preparedness and resiliency strategies, and more cross-functional organizational structures are among the most significant implications cited by survey respondents (chart 2).

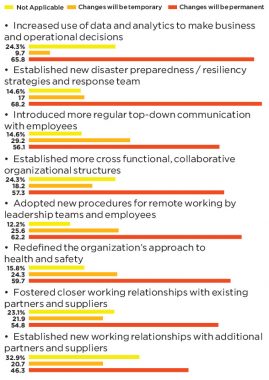

But when asked whether these and other management strategies and tactics will end up being permanent elements in leadership’s playbook going forward or just temporary, a result extraordinary in the annals of MLC research occurred.

Powerful majorities said that most of the changes they were asked about will become permanent elements of their leadership approach. For example, 68.2% said that new disaster preparedness plans, resiliency strategies, and response teams will become permanent features in their companies. Likewise, 57.3% said that more collaborative, cross-functional organizational structures will take root. And 62.2% expect that remote working by both leadership teams and employees will continue (Chart 3).

Defining Leadership

As these changes take place, the definition of what operational leadership means in the digital era is becoming more deeply engraved in that metaphorical playbook.

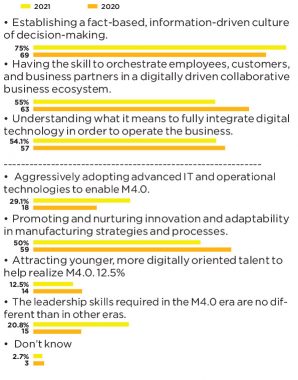

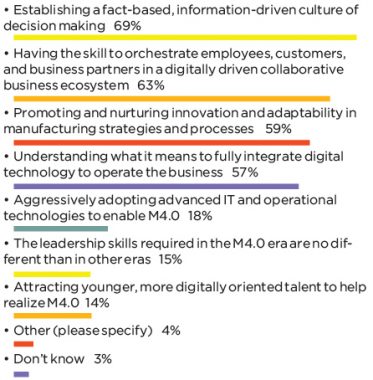

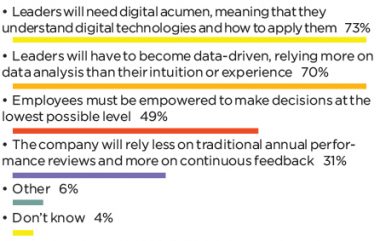

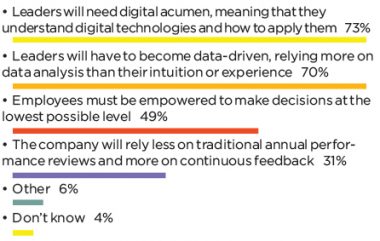

In the new survey, 75% of respondents say that establishing a fact-based, information-driven culture of decision-making in their organizations is the statement which best describes what leadership means in the M4.0 era. This finding is up six points from 2020’s survey.

The two other statements which received the highest responses (survey takers were asked to rank their top three choices from a list of seven options) are: having the skills to orchestrate employees, customers, and business partners in a digitally driven, collaborative business ecosystem, at 55.5%, and understanding what it means to fully integrate digital technology in order to operate the business, at 54.1% (chart 4).

Notable, though, is the finding on aggressively adopting advanced IT and operational technologies. This year, the percentage of respondents citing this statement leapt 11 points to 29.1% of the sample compared to 2020, an increase which may reflect the desired acceleration of M4.0 as a result of the pandemic.

“Establishing a fact-based, information-driven culture of decision-making is once again the most popular definition of what leadership means in the M4.0 era.”

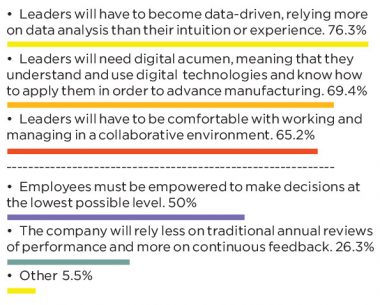

And when it comes to new skills that will be important for the digital era, survey respondents have reinforced the message about culture and collaboration by citing data analysis skills, understanding how to use digital technologies to advance manufacturing, and working in a collaborative environment as key areas of development (chart 5).

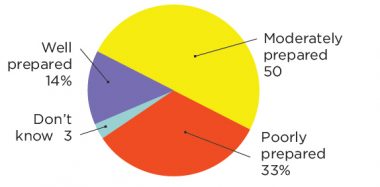

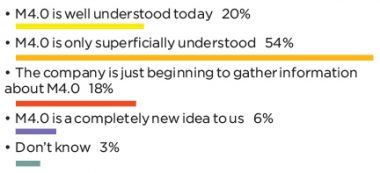

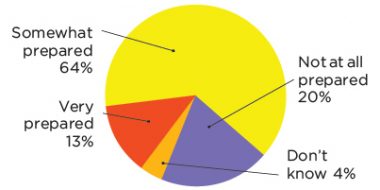

Perhaps as a result of the amount of change that has occurred in the past year, manufacturing executives are feeling somewhat better about how well prepared they and their teams are to manage the journey to M4.0.

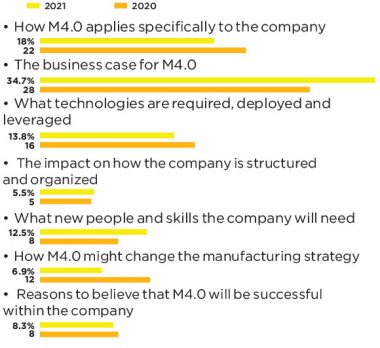

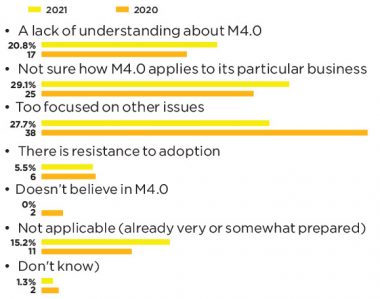

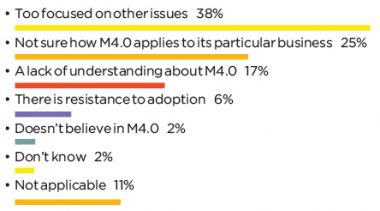

The percentage of leaders who indicate they are not prepared for the journey has dropped nearly five points in this year’s survey, to 15.2% of the sample, while the percentage of those who have some degree of preparedness has rise slightly over last year (chart 7). For those who still feel that they are not prepared, the most cited reason, by 29.1%, is that they are simply not sure how M4.0 applies to their particular business (chart 8).

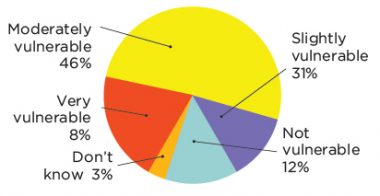

Nevertheless, perceptions about how vulnerable their company’s future success might be as a result of their level of M4.0 preparedness remain a mixed bag, with the percentage of those feeling very vulnerable rising to 15.2% of respondents this year, compared with eight percent in 2020, and those not feeling vulnerable at all dropping to 6.9%, from 12% last year (chart 9).

Desired Knowledge and Expertise

Looking ahead, what do manufacturing executives say are the most important leadership skills and abilities they feel they must develop to be successful with M4.0?

This year, once again survey respondents attach the highest degree of importance to the ability to rethink the business and successfully embrace the digital model. Even though the percentage of those indicating a high degree of importance to this ability dropped nearly six points from 2020, to 66.1% this year, this ability remains far ahead of other factors such as reducing costs and process integration. (chart 11).

“For manufacturing leadership, the past year has been an unprecedented test. But it has also been a time for more expansive thinking about what’s possible.”

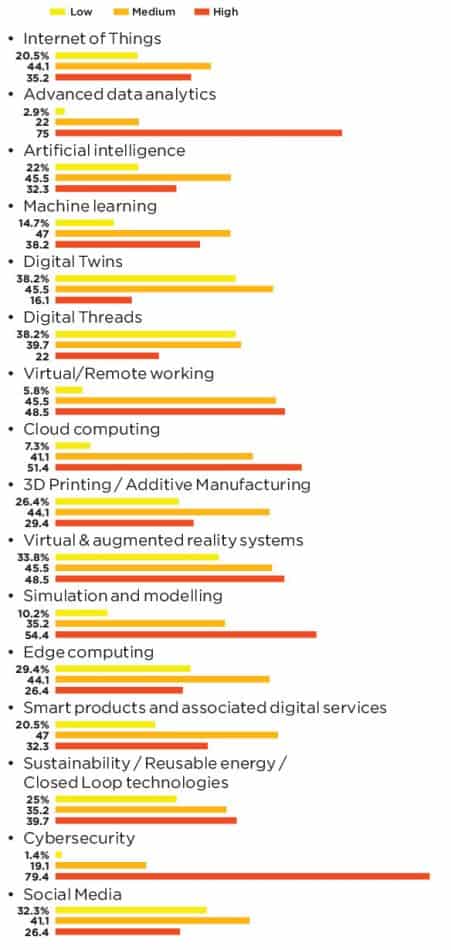

And when it comes to a variety of technologies with which they feel they need to develop knowledge and expertise, this year’s survey findings strongly mirror last year’s results. For example, this year manufacturing executives once again attach a high level of emphasis to developing expertise around cybersecurity, advanced data analytics, and simulation and modeling (chart 12).

The quest for knowledge and expertise will play out against a backdrop of demographic and organizational challenges that will reverberate deeply in manufacturing companies.

The Challenges Ahead

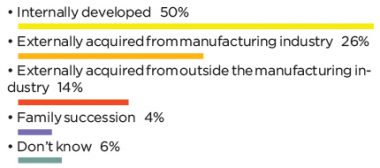

As baby boomers retire, companies grapple with the persistent open job problem, and as they seek to understand what functions and skills they will need in an increasingly digital-influenced workforce, many manufacturers executives today see the primary source of next-generation leaders coming from their internal ranks.

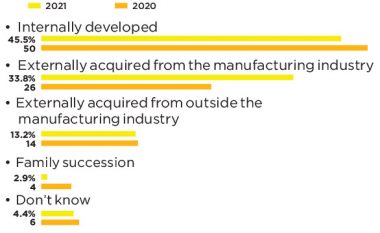

But this year’s finding of 45.5% of respondents citing internal sources dropped nearly five points from last year’s survey, with a modest shift occurring in favor of finding talent elsewhere in the manufacturing industry. Fully one-third of respondents this year said they would be looking within the industry for talent. Only a fraction, 13.2%, expect to be sourcing candidates from other industries (chart 13).

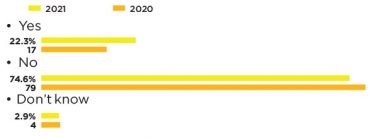

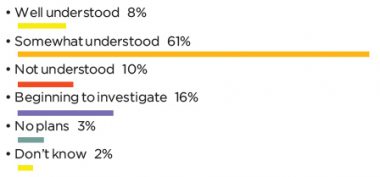

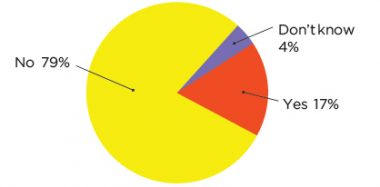

These number could shift, of course, as manufacturers attain a greater understanding of what functions and skills they will need in the future. Today, only a fraction of survey takers, 7.4%, indicate they have a solid understanding of the new digital roles and skills they will need. About 65%, however, say these requirements are somewhat understood, up several points from last year, an encouraging sign. But where there is substantial headroom for improvement is in training. Only 22.3% of survey takers this year indicate they have formal training programs in place to educate workers and leadership about the requirements of M4.0 (charts 15,16).

As they work out these issues, leaders today will also be grappling with the structure within which people will work, a structure which has been slowly but inexorably changing over the years to a flatter, more collaborative model of working. In this year’s survey, nearly half of survey respondents, 48.5%, identified understanding how the company should be organized as a result of new technologies as a key challenge for leadership, a finding up a whopping 23 points from last year. No doubt this finding has been flavored by the pandemic experience as more people have had to work remotely, but the effects of M4.0 technologies in empowering more people with information and thereby changing decision-making processes may also be a mounting factor (chart 14).

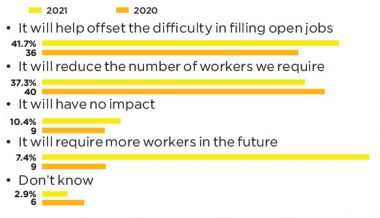

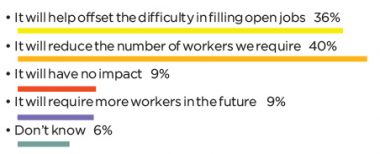

The effects of M4.0 technologies will also have an impact on workforce size, as a significant number of manufacturers are looking at automation and advanced M4.0 technologies as ways to address the open jobs problem. This year, 41.7% of respondents said these technologies will help offset the difficulty in filling open jobs, up from 36% last year.

What the Future May Hold

As historians have pointed out, sometimes great crises give rise to new and better ways of doing things, enabling progress. The heightened sense of urgency in created digitally-powered agility as a result of the pandemic has fostered a broad set of strategic and tactical changes across manufacturing, all adding up to an opportunity to redraw the boundaries of what was thought possible.

Now, manufacturing leadership has the responsibility to see these changes through. If they are successful in doing so, they will take the industry to a new and better level, raising the bar for all and redefining the rules of competition. M

Part 1: COVID-19 Impact

1. A Majority Says COVID Has Increased Focus on M4.0

Q: What impact has COVID-19 had on your leadership team’s focus on digital / M4.0 transformation? (select one)

2. Remote Working, Resiliency Top List of COVID-Related Changes

Q: What impact has COVID-19 had on your leadership approaches to managing your manufacturing enterprise? (rank each category)

3. Solid Majorities Say Many Changes Will Be Permanent

Q: How long do you expect these new leadership approaches to continue? (rank each category)

Part 2: Defining the Leadership Role

4. Once Again, Building a Fact-Based Culture is Top Leadership Definition

Q: Which statement best describes what leadership means in the Manufacturing 4.0 era? (Rank top 3)

5. Data Orientation, Digital Acumen Lead Desired Skills

Q: Which new approaches and skills do you feel will be most important for the M4.0 era? (Rank top 3)

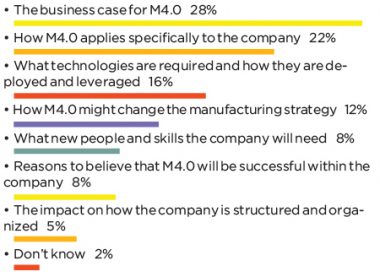

6. The M4.0 Business Case Remains Key Question

Q: What’s the most important thing your company’s executive management team wants to know about M4.0? (Select one)

7. Slight Improvement in M4.0 Preparedness

Q:How prepared do you think your company’s executive management team is to lead and manage the journey to M4.0? (Select one)

8. M4.0 Applicability is Key Issue in Preparedness

Q: If your company’s executive management is not well prepared for M4.0, what is the most important reason for the lack of preparedness? (Select one)

9. Perceptions of M4.0 Vulnerability Rise

Q: How vulnerable will your company’s future success be as a direct result of your company’s current level of M4.0 preparedness? (Select one)

10. M4.0 is Largely a Collaborative Effort

Q: Who is leading the charge around your digital

transformation efforts in your organization? (Select one)

Part 3: Developing Knowledge and Expertise

11. Rethinking the Business is Key M4.0 Skill

Q: Looking ahead, what degree of importance would you assign to the following M4.0 leadership skills and abilities? (Rate each on scale of Low/Medium/High

12. Cyber, Analytics Top List of Desired Knowledge

Q: Looking ahead, what degree of emphasis would you place on the following technology areas in terms of developing knowledge and expertise? (Rate each on scale of Low/Medium/High)

Part 4: Assessing Leadership Challenges

13. Most See Next Gen Leaders Sourced Internally

Q:Where do you see the next generation of leaders coming from for your company? (Select one)

14. M4.0 Organizational Impact is Top Challenge

Q: In thinking about the requirements and implications of M4.0, what do you think are the most important challenges for leadership? (Rank top 3)

Part 4: Workforce Development and Transition

15. Understanding Digital Skills Makes Little Progress

Q: How well prepared do you think your company is in understanding the new digital roles and skills that you will need in the next few years? (Select one)

16. Vast Majority Still Without Formal M4.0 Training

Q: Does your company have a formal training plan to educate workers and leadership around the requirements of Manufacturing 4.0?

17. Automation Seen as an Open Jobs Remediator

Q: What impact do you think the increasing adoption of automation and advanced M4.0 technologies will have on workforce levels in your company in the future? (Select one)

Survey development was led by David R. Brousell, with input from the MLC editorial team and the MLC’s Board of Governors.

COVID-19: A Catalyst for M4.0 Culture

The pandemic has spurred a paradigm shift in cultural transformation as manufacturing companies have leveraged M4.0 to accelerate digital adoption, collaboration, innovation, and integration across their enterprises, reveals the Manufacturing Leadership Council’s latest M4.0 Cultures survey.

By Sue Pelletier

It’s undeniable that the COVID-19 pandemic has caused massive disruption in the manufacturing environment over the past year. Supply chain disruption, already a growing problem pre-pandemic, became more acute as different areas of the world shut down to slow the spread of the virus. Some manufacturers pivoted to retool their factories to supply much-needed personal protective equipment (PPE) and other COVID-necessitated supplies, while others struggled to keep shop floor workers safe and learned on the fly how to manage employees who suddenly had to work remotely.

The impact on manufacturing cultures has been significant. The results of the Manufacturing Research Council’s latest M4.0 Cultures survey reveal that the abrupt shifts and continued disruptions of the COVID-19 crisis have driven leaders to sharpen their focus on M4.0 and accelerate adoption across everything from enterprise connectivity and corporate collaboration, to functional integration and innovation, and to start redefining what health and safety should mean for their employees in the future.

What’s more, while some of the workforce cultural changes, such as PPE and masking for front-line employees, may be temporary, the survey results clearly indicate that a major shift toward an M4.0 culture that is digitally enabled, collaborative, innovative, and data-driven is not only underway more rapidly than ever before, but is also here to stay.

There will continue to be a few bumps in the road ahead, of course. While corporate cultures are increasingly becoming more customer-centric and collaborative, the journey toward M4.0 is still a work in progress for many companies as concerns about the costs and ROI of M4.0 transformation, along with getting full buy-in from both employees and leadership, stubbornly continue to impede the progress of cultural changes. But it is clear that the COVID viral firestorm has made manufacturers acutely aware of the need to continue along that M4.0 journey. With many saying the recent changes in their corporate culture will now be permanent, it’s clear that they are already beginning to see the results, from improved morale and a more efficient workforce, to more productive and innovative operations. And those are exactly the kinds of benefits that will spur them to continue to overcome any remaining hurdles.

“Manufacturers now believe that the M4.0 paradigm shift that has accelerated over the past year has led to permanent changes that will have a lasting impact on their organizations for many years to come.”

Culture Change Accelerates During COVID

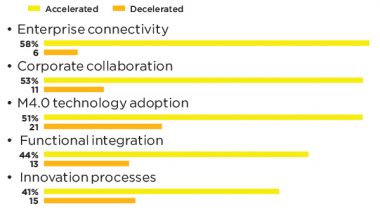

While it might be expected that the pandemic’s disruptions could have slowed the adoption of digital M4.0 plans, that turned out not to be the case. As leadership teams have intensified their focus on M4.0 over the past year (Chart 2), more than half said they have accelerated both enterprise connectivity and M4.0 technology adoption since COVID-19 hit (Chart 1). Corporate collaboration initiatives also sped up for more than 50% of companies, with ramped up functional integration strategies and faster innovation processes also reported by more than 40% of survey respondents.

While COVID has clearly had a significant impact on many areas of corporate culture, one of the key takeaways from the survey is that these are not quick fixes to patch operations until the crisis passes. The results make it clear that manufacturers now believe that the M4.0 paradigm shift that has accelerated over the past year has led to permanent changes that will have a lasting impact on their organizations for many years to come.

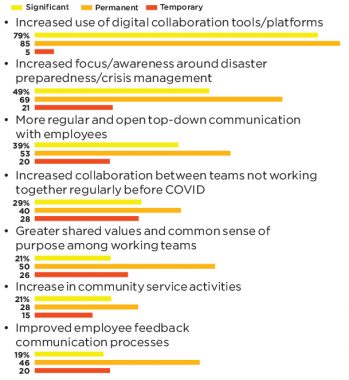

For example, one of COVID’s biggest impacts on corporate culture has been an increased use of digital collaboration tools and platforms, which a full 79% ranked as “significant” (Chart 3). An overwhelming 85% said this change is likely to be permanent. Another change spurred by the pandemic that the majority expect to become permanent is the shift toward increased focus on disaster preparedness and crisis management.

Other significant changes slated to become permanent fixtures in corporate culture for many include more regular and open top-down communication with employees, more collaboration between teams who did not previously work together, and an increased sense of purpose and shared values among working teams. Improved employee feedback and communication from the bottom up, while not as widely instituted, is a change almost half of those who have made improvements plan to make permanent.

“The survey results clearly indicate that a major shift toward an M4.0 culture that is digitally enabled, collaborative, innovative, and data-driven is not only underway more rapidly than ever before, but is also here to stay.”

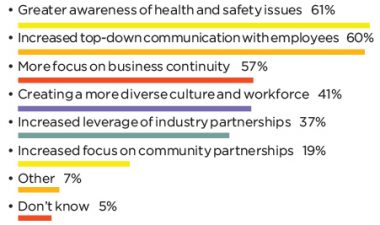

While widely implemented pandemic-specific health and safety shifts such as PPE and mask requirements are only planned to become permanent for a quarter of respondents, health and safety strategies are being extensively redefined and are going to mean much more than just accident prevention moving forward, said 61% (Chart 4). Seventy percent of those who shifted to remote and virtual work strategies also say they intend to enable at least some of their workforce to continue working from home in the future. This also reflects the increasing use of digital collaboration tools and platforms that make remote work feasible for many more employees, and which will continue to move companies toward creating a more empowered, collaborative, and responsive workforce for the future.

M4.0 Culture Moving into the Mainstream

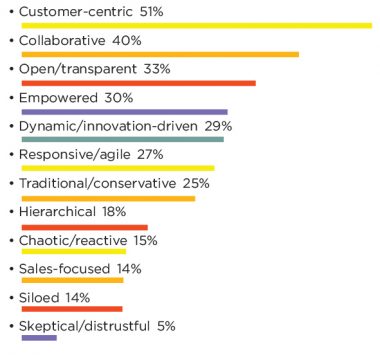

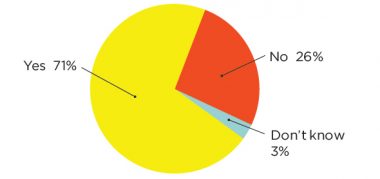

The shift toward a more M4.0-based overall corporate culture is evident in the terms manufacturers now use to describe the current state of their corporate cultures, with customer-centric and collaborative topping the list. (Chart 5). What is clear, however, is that there is a strong belief that continued culture change will be essential in the digital age, with a substantial 71% saying they will need to continue to transform their cultures in the future to fully take advantage of all the M4.0 era offers (Chart 6). For example, 60% consider a move toward more data-driven decision-making should be on top of their change agenda, and more than half believe better integrated, more cross-functional teams would help drive future success. Increased responsiveness, more agile operations, faster innovation and time-to-market for new products, and even more of an emphasis on customer and supplier centricity are also likely to be key elements of necessary culture change (Chart 7).

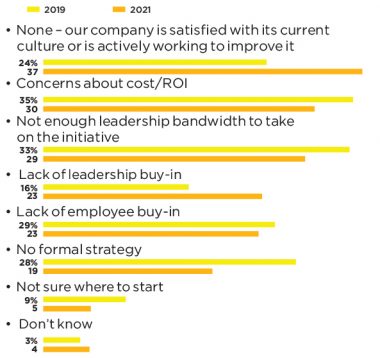

Many of those changes are already underway. Thirty-seven percent now say they are either satisfied with their current culture or actively working to make the needed changes, up from 24% in 2019 (Chart 8). While these changes may be incremental, there are still many ongoing challenges to cultural transformation, with top concerns such as cost/ROI and a lack of leadership bandwidth/buy in dominating the list, followed by a lack of employee buy-in and no formal strategy.

Collaborative Cultures on the Rise

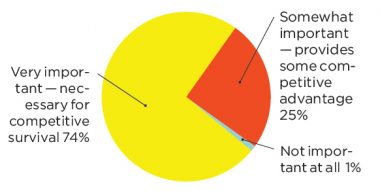

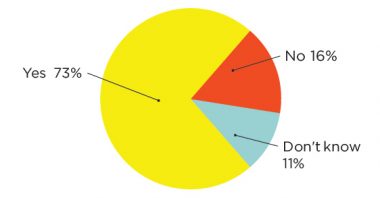

With almost unanimous agreement that a collaborative culture is either very or somewhat important to future competitiveness, and three quarters (74%) identifying it as necessary for competitive survival, it is evident that collaboration is top of mind for today’s manufacturers (Chart 10). While the immediate needs of dealing with the pandemic likely led to the slight rise in traditional command-and-control hierarchical structures in some organizations, from 30% in 2019 to 34% in 2021, only 14% of manufacturers predicted that this approach would still hold true two years from now. Even more telling is the rapid rise of those who describe their culture as collaborative, which went from 17% in 2019 to 26% in 2021, and is predicted to surge to a substantial 51% by 2023 (Chart 9).

The key enablers to achieve that desired collaborative culture, according to 61% of respondents, are M4.0 technologies and approaches (Chart 11). This is reflected in the significant increase in the adoption of digital threads across all company functions over the past two years. In manufacturing operations, for example, the use of digital threads shot up from 45% in 2019 to 70% of companies today, while supply chain digital threads are now being used in 50% of organizations (up from 35% in 2019), and further increases are evident in design and engineering, IT, and even in more customer-focused areas such as sales and marketing and customer service and support (Chart 12).

M4.0 Drives Faster Innovation

Innovation processes have also accelerated in many manufacturing companies over the last two years, with 25% saying they are continually developing new products and embracing change, up from just 19% in 2019. More than half aren’t far behind, defining their culture as “moderately innovative,” and being willing to experiment with new technologies, products, and services (Chart 13). Perhaps most importantly for the future though, almost three-quarters of companies now credit M4.0 technologies and approaches as key drivers to faster and more effective innovation in the years to come (Chart 14).

The source of ideas for these new products, processes, and/or business models has also shifted slightly since 2019, with suppliers kickstarting innovation for 47% of manufacturers, up from just 28% two years ago (Chart 15). External partners and academic and research institutions also are taking on an increasing role in innovation. But, that pales in comparison to the growing role of company employees, whom 86% of manufacturers now credit as the source for new ideas, compared to 74% in 2019.

“While many were already on the road toward M4.0 before the pandemic hit, COVID-19 proved to be a wake-up call that the time is now to start implementing the changes to corporate culture needed for today’s, and tomorrow’s, manufacturers.”

M4.0 Essential to Integration

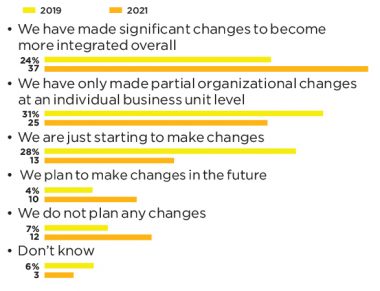

The flattening of corporate hierarchies, the elimination of siloes, and the increase in communication and cross-function and cross-training in the workforce are resulting in an increasingly integrated business. More than a third of companies in the survey say they have already made significant changes to become more integrated, up from less than a quarter in 2019 (Chart 16).

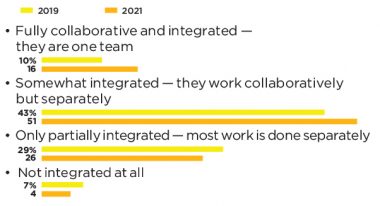

As with collaboration, M4.0 technologies and approaches also are regarded as essential ingredients to successful integration, according to 69% of respondents (Chart 17). But when it comes to integrating IT and OT teams, there’s still some progress to be made. While more than half now have at least somewhat integrated OT and IT functions, up from 43% in 2019, only 16% say these areas are fully integrated so far (Chart 18).

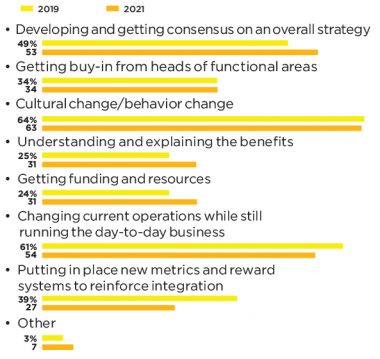

Creating a more integrated enterprise remains challenging, however. Issues around effectively managing cultural/behavior change, having the leadership time and focus to change operations while still running the business, and developing the consensus needed for an implementable overall strategy, continue to be the most significant barriers to integration. However, the latest survey also suggests there also growing concerns over getting buy-in from heads of functional areas, understanding the benefits, and obtaining funding and resources to make it happen (Chart 19).

While many were already on the road toward M4.0 before the pandemic hit, COVID-19 proved to be a wake-up call that the time is now to start implementing the changes to corporate culture needed for today’s, and tomorrow’s, manufacturers. The key to future success will be to keep that momentum, born in many cases of necessity, going once the immediate crisis subsides. The role of M4.0 in that continued transformation now seems abundantly clear. M

Part 1: COVID-19 Impact

1 COVID-19 Has Accelerated M4.0 Transformation Across Multiple Areas

Q:What impact has COVID-19 had on your M4.0 transformation strategy in the following areas?

2 50% Say COVID-19 Has Also Increased Leadership Focus on M4.0

Q: What impact has COVID-19 had on your leadership team/management’s focus on digital/M4.0 transformation?

3 85% Expect Increased Use of Digital Collaboration Tools to Be Permanent

Q: What impact has COVID had on your corporate culture, and how long do you expect these impacts to continue?

4 Working Cultures Shifting to Remote, Safer Strategies for Employees

Q: What impact has COVID-19 had on your workforce culture, and how long do you expect these impacts to continue?

Part 2: Overall Company Culture

5 Corporate Cultures Increasingly Customer-Centric and Collaborative

Q: What term would you use to describe your company’s culture today?

6 Strong Majority Believe Culture Change Needed in Digital Era

Q: Thinking about the requirements of the digital age, does your company believe it needs to change its culture to embrace this new era?

7 Data-Driven Decision-Making & Functional Integration Top Culture

Change Agenda

Q:If a culture change is needed, which description would best capture what that change would encompass?

8 ROI Concerns & Leadership Bandwidth Remain Key Challenges to Change

Q: What are your company’s biggest challenges

to cultural change?

Part 3: Collaboration

9 51% Predict Collaborative Structures Will Dominate in 2 Years

Q: How would you describe your overall corporate structure today, and where do you expect it to be in 2 years’ time?

10 Three Quarters Say Collaboration is Essential to Competitiveness

Q: How important do you think a collaborative

culture is for competitiveness?

11 M4.0 Key to Enabling a Collaborative Culture

Q: Is there a clear belief that M4.0 technologies and approaches are key to enabling a more collaborative culture?

12 Extensive Adoption of Digital Threads Across All Functions in Last 2 Years

Q: Which of your company functions are connected to a digital thread to enable end-to-end data sharing and collaboration?

Part 4: Innovation

13 Three-Quarters Say They Are Already Moderately to Highly Innovative

Q:How would you describe your company’s current level of innovation?

14 Almost Three-Quarters Believe M4.0 is Key to Driving Innovation

Q: Is there a clear belief that M4.0 technologies and approaches are key to enabling faster and more effective innovation?

15 Increasing Role for Employees & Suppliers as Source of Innovative Ideas

Q: Where does your company source its ideas for new products, processes, and/or business models?

Part 5: Integration

16 More Than a Third Have Significantly Integrated Organizational Structures

Q: To what extent has your company made changes to its organizational structure in order to create a more integrated enterprise?

17 M4.0 Seen as Key to Enabling Integration

Q: Is there a clear belief that M4.0 technologies and approaches are key to enabling more integrated operations?

18 Increasingly Integrated OT & IT Teams in Last 2 Years

Q: How would you describe the level of

integration between your IT and OT teams?

19 Culture Change Remains Key Challenge to Successful Integration

Q: What are the most significant challenges to improving your company’s integration?

Survey development was led by Executive Editor Paul Tate, with input from the MLC editorial team and the MLC’s Board of Governors.

Fast Forward for Future Factories

The COVID pandemic has triggered a surge in M4.0 adoption across almost every function of manufacturing production that promises to rapidly transform the way factories are designed, operated, and managed in the next decade, reveals the MLC’s latest Factories of the Future survey. By Paul Tate

Every journey of digital transformation takes time. Manufacturers must wrestle with, and overcome, a multitude of technical, cultural, management, organizational, and partnership issues to swiftly and effectively reach their ultimate digital goals.

Then something happens that suddenly makes rapid progress more urgent than ever. A global event that forces leadership teams to respond by hitting the fast forward button on their strategic plans. The impact of the continuing COVID pandemic on manufacturing is proving to be exactly that kind of catalyst.

The results of the Manufacturing Leadership Council’s 2021 survey on Factories of the Future clearly show that, over the last year, the impact of the pandemic has forced a broad range of industrial companies to make fundamental and rapid changes across their manufacturing value chains. And the implications for the future of the industry are only just beginning to be understood. The fallout from the pandemic is already spurring more and more manufacturing companies to accelerate their digital progress and change the way that factories will be designed and operated in the future.

M4.0 Inflection Point

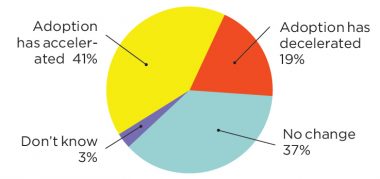

When the MLC first surveyed its membership to understand more about the pandemic’s potential impact on M4.0 adoption during the height of the first COVID wave in April and May of last year, just over 50% of respondents indicated that it had prompted them to accelerate their adoption of M4.0 technologies across their organizations and factory floors. At that time, it was not clear if that initial response was simply driven by the urgent need for immediate mitigation tactics to cope with the sudden disruption.

The MLC’s latest research, however, clearly indicates that this acceleration surge was far from a temporary fix. Over 40% of respondents in our latest survey now confirm that they will continue to accelerate their rate of M4.0 adoption for the foreseeable future (Chart 1). For two in five manufacturers, this marks an inflection point in M4.0 adoption that is set to drive digital transformation faster than ever before.

A further third, the same proportion as in the initial survey, also confirm that they will continue with their M4.0 adoption plans at the same rate as before the pandemic, despite widespread disruption to their businesses over the last few months.

Nevertheless, some companies have also seen revenues dive during that period, forcing a reduction in budgets across multiple areas of the company, including their M4.0 plans. Today, around one in five say they have been forced to decelerate their M4.0 adoption plans accordingly, at least for the time being. As economic and business recovery progresses, however, especially with the new hope of mass immunity provided by COVID-19 vaccines, those strategic digitization plans may yet be reengaged.

Permanent Health Changes

Accelerated digitization is not the only lasting impact of the COVID pandemic for manufacturers. Over the last year companies have radically revamped their plant floor health and safety procedures to protect their workers and create a safe and reassuring environment for their employees. From redesigning frontline workstation layouts and activities to allow adequate social distancing, to temperature testing on entry, multiple sanitation stations across the plant, obligatory protective clothing, staggered shifts, and remote working options, manufacturers have responded with a multitude of new safety measures in their facilities. [/et_pb_text]

“The fallout from the pandemic is already spurring more and more manufacturing companies to accelerate their digital progress and change the way that factories will be designed and operated in the future.”

“The fallout from the pandemic is already spurring more and more manufacturing companies to accelerate their digital progress and change the way that factories will be designed and operated in the future.”

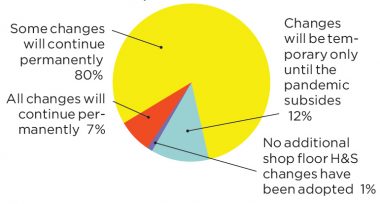

Yet looking ahead, a massive 80% of respondents in the latest survey say that they intend to continue with some of these new plant floor health and safety measures, not just for the duration of the pandemic, but permanently (Chart 2). Seven percent of respondents even suggest they intend to continue with all of their health and safety changes for the future. Clearly, some aspects of the traditional manufacturing workplace seem to have changed forever as a result of the COVID crisis.

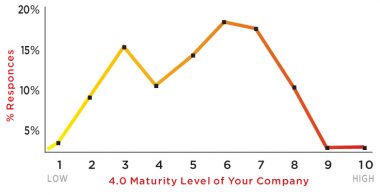

Diverse M4.0 Maturity Levels

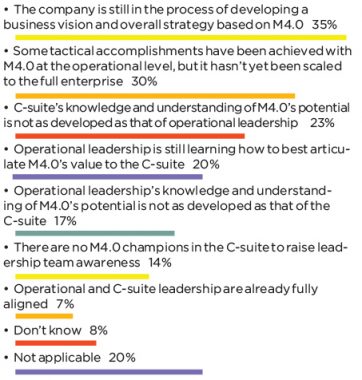

As some manufacturers begin to accelerate their M4.0 adoption and others continue with their established digitization plans, the M4.0 maturity levels across the industry remain patchy. Most consider their current maturity level in the middle range, predominantly between five and seven on a scale of ten, where ten is the highest maturity level (Chart 3). A quarter, however, feel that they are still in the early stages of digitization, scoring themselves at a low two (9%) or three (16%) on the maturity scale. It will be interesting to track changes in these results in future MLC surveys to better understand rates of progress in the months to come.

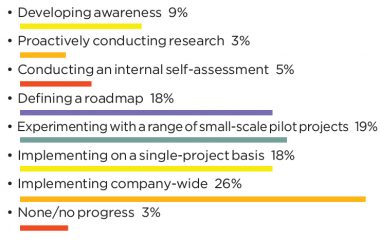

Nevertheless, for those that have grasped the digital challenge, an encouraging 26% say that they have now scaled their M4.0 efforts on a company-wide basis (Chart 4), more than double the result of two years ago when the figure was 12%. What’s more, a further 18% are now implementing M4.0 on a single project basis, again double the figure from 2019. Meanwhile, a further 19% say they have already begun experimenting with a range of small scale M4.0 pilot projects, often the forerunner of wider corporate adoption, so further widespread implementations are likely to follow in these companies too, over the next 12 months.

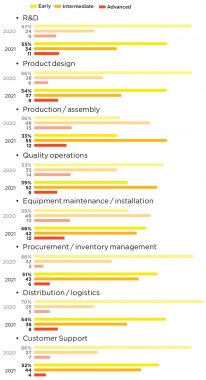

These strong indications of increasing rates of M4.0 adoption and maturity are also reflected in a breakdown of which functions are involved. Over the last year there has been a marked shift in M4.0 implementation levels across almost every function in the survey as many companies have moved from what they considered to be early-stage adoption last year, to the more mature intermediate level in 2021 (Chart 5). This shift is most notable in the areas of production and assembly, quality operations, procurement, distribution, and customer support.

Nevertheless, there is clearly still a great deal of headroom for improvement as only a minority of companies in each category so far consider their levels of adoption to have reached an advanced stage.

“Digital twins currently top the list of the top ten technologies that companies feel will be most important to them in the near future.”

Top M4.0 Technologies

Such improvements will be facilitated by the further implementation of a combination of key M4.0 technologies, and future manufacturing investment plans show these are predominantly focused around more visual, predictive, collaborative, and augmented digital tools (Chart 6).

Ranked by levels of investment intent for the next two years, the latest survey reveals that digital twins currently top the list of the top ten technologies that companies feel will be most important to them in the near future, with over a third of companies (34%) planning to expand their use of digital twins over the next 24 months.

Initially conceived to help streamline the product design process in more visual ways, digital twin technologies have begun to sweep across organizations as an effective tool to virtualize almost every aspect of the organization, from production processes, to plant floor design, workflows, supply chains, material and waste flows, and distribution networks, increasingly supported by real-time IoT data (26%), predictive analytics (23%), and AI (29%).

The ability to share these virtual models in a collaborative way across multiple functions and partners is also driving the popularity of widely connected digital threads across the organization, with 28% of companies planning to invest more extensively in the future.

Tools that help augment the workforce are also high on the investment list, including AR and VR systems (29%) allowing the remote sharing of visual data and helping train employees, and collaborative robots (29%) that can help augment a multitude of physical tasks in a safe and effective way on plant floors and beyond.

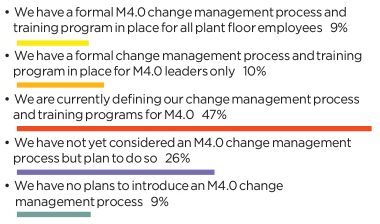

Lag in Managing Change

While M4.0 technology adoption seems to be moving swiftly, however, many companies, are still not up to speed when it comes to the associated change management processes needed to support their digital transformation (Chart 7). Almost half the companies in the survey (47%) admit that they are still defining their change management processes and training programs associated with M4.0 plant floor initiatives. Another quarter (26%) have yet to even consider developing a change management approach, although they do say they plan to do so at some stage.

This lag in the development of change management processes may become increasingly critical to both the pace and success of M4.0 adoption in the years ahead, and leadership teams clearly need to take this aspect more seriously if they wish to bring their workforce along with them to reach their digital goals.

Hybrid Future Factory Models

At a more strategic level, the survey also reveals that there are some significant trends underway in how manufacturing companies plan to structure and manage their increasingly digitally enabled factories in the future too.

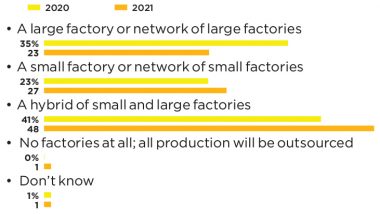

The days when companies built, and depended on, large consolidated global factories alone seem to be numbered. Perhaps intensified by the lessons of the pandemic and a rising awareness of the vulnerabilities and complexities of global mega-factory footprints in a disruptive world, the last year has seen an accelerated shift away from large factories, or networks of large factories, as a future production strategy – down from 35% in 2020 to just 23% this year (Chart 8).

The majority of companies now envisage their future factory strategy to be a hybrid mix of smaller, local production sites and large facilities (48%), or simply a network of more flexible smaller factories that operate closer and more responsively to the local markets they serve (27%).

“The lag in the development of change management processes may become increasingly critical to both the pace and success of M4.0 adoption in the years ahead.”

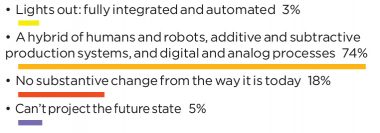

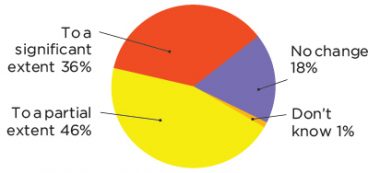

“And those smaller factory networks will be increasingly digitized, the results reveal. Three quarters of respondents (74%) expect their future factory models to operate as a hybrid of humans and digital technologies, including robotics, additive and subtractive production systems, and increasingly digital processes (Chart 9).

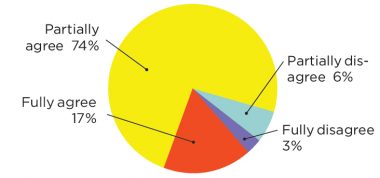

And while very few expect digital technologies to entirely automate future factories to become totally lights out, autonomous operations (3%), nine out of ten respondents either partially agree (74%) or fully agree (17%) that tomorrow’s factories will indeed evolve to be increasingly self-learning facilities, harnessing the power of technologies such as AI and machine learning (Chart 10).

A More Collaborative Future

The increasing use of advanced analytical and predictive self-learning technologies, digital twins and threads, and ever more virtual and visual tools in tomorrow’s factories makes one thing very clear, however. The way those factories will be managed will be more collaborative than ever before.

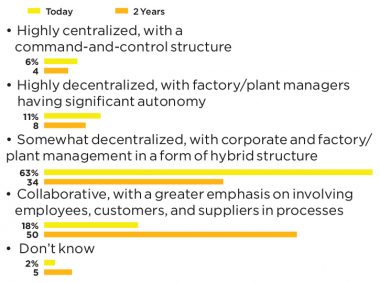

Within the next two years, half the respondents (50%) expect their factories to be managed in a more collaborative way, with a greater emphasis on involving employees, customers, and suppliers in production processes (Chart 11). That is a significant and rapid increase in collaborative management approaches from the current level of just 18% today. Traditional, highly centralized management structures are already few and far between at 6%, and look set to reduce even further to only 4% in the same period. Even today’s prevalent decentralized approaches, where corporate and plant management structures are in a hybrid form, are predicted to almost halve from 63% to 34% over the next 24 months.

Preparing for Cyber Disruption

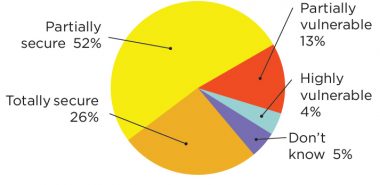

As digitization increases, of course, so do the potential levels of vulnerability of plant floor systems and assets to malicious cyberattack. Many companies have already begun to address the issue (Chart 12) and now consider themselves to be either totally secure (26%), or partially secure (53%) from cyber disruption. Nevertheless, almost one in five say they remain either partially vulnerable (13%) or highly vulnerable (4%). Obviously, there is still work to be done in some companies to improve their plant floor cyber protection strategies.

“As digitization increases, so do the potential levels of vulnerability of plant floor systems and assets to malicious cyberattack.”

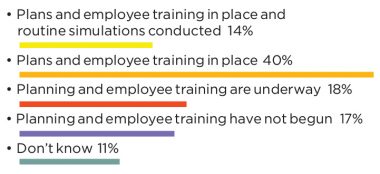

Raising workforce awareness about potential cyber threats is an essential part of that protection process. Reassuringly, survey respondents reveal that two thirds of companies now have some level of workforce preparedness program either in place or underway (Chart 13).

Fourteen percent say they already have extensive plans and employee training in place and routinely conduct simulations; 40% say they now have some form of plan and cyber awareness training available; and another 18% are now actively planning to develop those cyber training programs in the near future. Again, though, that leaves a gap of 17% of companies that have yet to catch up with the realities of potential plant floor cyber threats, and work remains to be done.

Digitization Challenges Remain

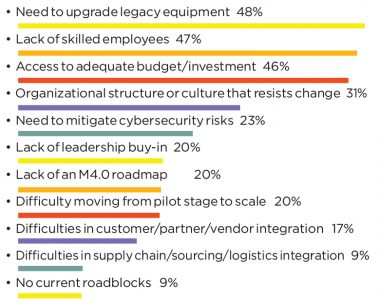

Some aspects of manufacturing’s digitization journey continue to hinder progress, however. Once again, this year, the challenges of upgrading legacy equipment (48%), the lack of skilled employees (47%), and access to adequate investment budgets (46%), continue to dominate the list of key obstacles that manufacturers face as they strive to adopt new digital technologies in their production operations (Chart 14). Even organizational structures and cultures that resist change are still an issue for almost a third of companies (31%).

While legacy systems issues and skill shortages are not easy to fix through internal changes alone, leadership teams can have a direct impact on unblocking other obstacles to progress, such as access to investment budgets and improvements to organizational structures and cultures. It is hoped that the growing awareness of the opportunity impact of digital transformation among leadership teams will make an increasingly important difference to creating a positive climate of change in many manufacturing organizations in the years ahead.

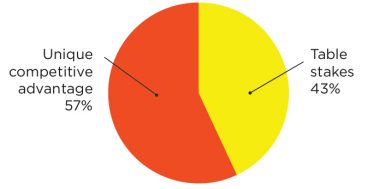

M4.0’s Competitive Imperative

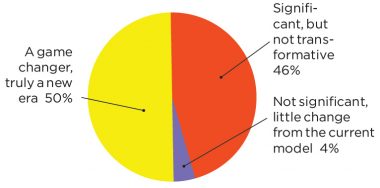

And if those leadership teams need any further evidence of the potential benefits that digital transformation can bring to help motivate them, the survey clearly indicates that a majority of survey respondents (57%) at least, believe M4.0 has the powerful ability to help manufacturing companies create a unique competitive advantage for their businesses in the future (Chart 15). What’s more, half the respondents think M4.0 represents a clear game changer for the entire manufacturing industry in the years ahead (Chart 16).

With those issues at stake, and the lessons of the COVID pandemic as a compelling spur to action, pushing the fast forward button to create increasingly digitally enabled factories of the future is becoming a more important competitive imperative than ever for the decade to come. M

Part 1: COVID-19 Impact

1 41% of Manufacturers Will Continue to Accelerate M4.0 Adoption

Q:What effect has the COVID-19 pandemic had on your company’s adoption of M4.0 in its plants or factories?

2 80% Say Some COVID-19 Health & Safety Changes Will Be Permanent

Q: Do you expect any additional plant floor health and safety measures and procedures you have introduced as a result of the COVID-19 pandemic to continue into the future?

Part 2: Status of M4.0 Adoption

3 Today’s M.40 Factory Maturity Levels Predominantly Mid-Range

Q: How would you assess the Manufacturing 4.0 maturity level of your company’s factories or plants?

4 A Quarter Already Implementing M4.0 Company-Wide: Another Third Have M4.0 Pilots or Projects Underway

Q: Which activity best describes the primary focus of your company’s M4.0 efforts today?

5 Levels of M4.0 Adoption Have Increased Across Almost All Functions in the Last Year (2020 vs 2021)

Q: At what stage of M4.0 adoption are the following functions in your company?

6 Top 10 Technology Investment Priorities for the Next 2 Years

Q: Where does your company stand regarding the following technologies?

7 Almost Half of Companies Still Defining M4.0 Change Management Processes

Q: At what stage is your organization with a change management program associated with M4.0 plant floor initiatives?

Part 3: Factory Organization & Management

8 Shift Accelerates Towards Small or Hybrid Factory Networks (2020 vs 2021)

Q: Looking ahead, which statement most closely describes what your company’s future factory strategy will be?

9 Three Quarters Expect Human/Digital Factory Model

Q: What is the expected future state of your factory model?

10 Over 90% Foresee Some Degree of Self-Learning in Tomorrow’s Factories

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-learning facility.”

11 Collaborative Management Approaches Set to Dominate Within 2 Years

Q: How would you characterize how your factories/plants are managed today and what do you anticipate will be the primary way they will be managed in the next 2 years?

Part 4: Cybersecurity Readiness

12 Cybersecurity Levels Still Leave

Room for Improvement

Q: As factories become increasingly networked and digitized, how would you rank your company’s technical security level against potential cyberattack/disruption to plant floor systems and assets?

13 Two Thirds Are Preparing Their Workforce for Cyber Attacks

Q:What is your level of workforce preparedness in the event of a cyberattack/disruption to plant floor systems and assets?

14 Legacy Systems, Skills, and Budgets Remain Biggest Obstacles to M4.0 Adoption

Q: What do you feel are your company’s primary roadblocks to implementing your M4.0 strategy?

15 57% Believe M4.0 Creates a Unique Competitive Advantage

Q: Do you believe that the adoption of M4.0 creates a unique competitive advantage for your company or is it merely table stakes to remain in the game?

16 Half Also Believe M4.0 is a True Game Changer for Manufacturing

Q: Ultimately, how significant an impact will M4.0 have on the manufacturing industry?

Survey development was led by Paul Tate, with input from the MLC editorial team and the MLC’s Board of Governors.

COVID-19: An Unlikely Inspiration

Spurred by the need for agility and flexibility in a time of crisis, manufacturers appear determined to accelerate their investments in digital technologies. By David R. Brousell

![]()

As the year 2019 was drawing to a close, it appeared that momentum was building for manufacturers to adopt advanced technologies as a key part of their journey to Manufacturing 4.0, the next wave of industrial progress based on digitization. And then, in February, the unexpected occurred — COVID-19 struck like a bolt of sustained lightning, upending life as we knew it.

By the end of June, U.S. Gross Domestic Product had fallen at a 31.7% annualized rate, the deepest decline since record keeping began in 1947. Nearly 30 million Americans were receiving unemployment checks by the week ending July 11. And by mid-September, there were 6.5 million COVID-19 cases and nearly 194,000 deaths in the U.S.

Between February and April, manufacturing production plummeted 20.3% and even after four straight months of improvement, the industry was still down 6.7% at the end of August, compared to where it was in February. Capacity utilization followed a similar pattern, dropping to 59.9% in April, the lowest rate since data gathering began in 1948, from 75.2% in February, and then recovering somewhat by the end of August when it reached 70.2%. And so the big question around Manufacturing 4.0, a nearly decade-old evolution that had been moving at a slow but steady pace, was would manufacturers be forced to put their digital technology investments on hold or scale them back significantly in order to weather the crisis and, if so, what damage would a hiatus have on the trajectory of the digital model?

The answer to that question was immediate and profound. The pandemic is shaping up to be an unlikely inspiration for change. Manufacturers’ ability to quickly pivot and produce pandemic-fighting materials and equipment was clearly linked to their digital maturity. Companies that had already invested in digital technologies were in a far better position to respond to the crisis than those that did not or did not do so sufficiently.

A poll conducted by the Manufacturing Leadership Council in May showed even stronger evidence that Manufacturing 4.0 was not going to be slowed down – 53% of respondents indicated that their companies would accelerate digital investments as a result of the pandemic.

Spending Acceleration Plans Still Robust

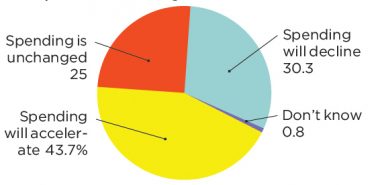

A new MLC poll, fielded in August, shows that number slipping but still robust. In that new poll, the MLC’s annual Transformative Technologies in Manufacturing survey, 43.7% of respondents indicated that their companies will accelerate spending on information and operational technologies as a result of the pandemic. Twenty-five percent indicated that spending will be unchanged (compared with 36% in the June poll) and 30.3% said that spending would decline (compared with only 7% in June). In addition, more than 79% of respondents also said that their companies would accelerate adoption of technologies that enable virtual working and remote monitoring of operations. (Charts 1, 2). As might be expected, conducting surveys in the midst of an on-going pandemic is an exercise fraught with unpredictability. Because of unknowns such as whether new surges of infection will occur, when a vaccine will be become available, and what the long-term damage to businesses might be, it is very difficult for companies to plan and budget. Current intentions around advanced technology investments could change at any time depending on circumstances.

But the new MLC Transformative Technologies poll, while raising concerns that spending may be cut back as the damage inflected by the pandemic is more fully felt in the months ahead, does offer some encouragement that manufacturers continue to be focused on the future, and what advanced technologies can do to make that future a digital one. Moreover, the new poll has certain strains of consistency with prior MLC surveys, most significant of which is manufacturers’ longer-term view of the transformative impact of advanced technologies.

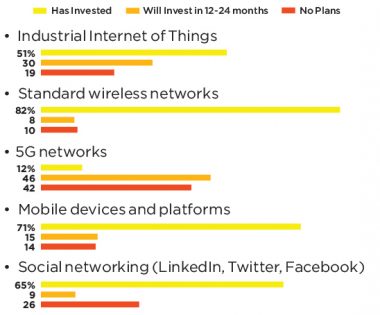

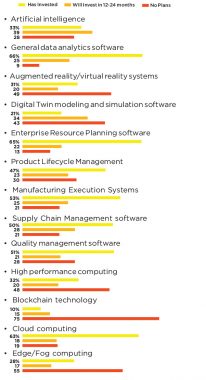

For example, across a range of 13 technologies surveyed, artificial intelligence once again this year strongly leads in respondents’ investment intentions over the next two years, a position that AI has held in MLC surveys for the past several years. This year, 38.7% of respondents indicated that their companies would invest in AI in the next 12 to 24 months. Digital twin modeling and simulation software comes in second, with 34.5% of respondents saying their companies will invest in this technology within the next two years, and supply chain management software comes in third, with 28.7% (Chart 4).

Manufacturers continue to be focused on the future and what advanced technologies can do to make that future a digital one.

The Promise of AI

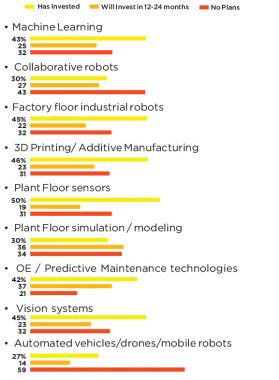

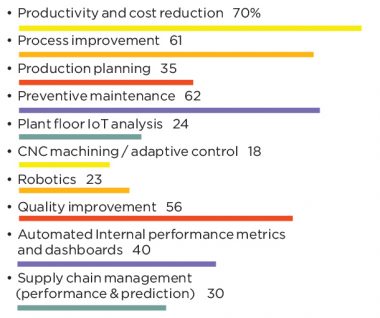

AI has apparently captured the imagination of manufacturers for what it promises to do to improve the effectiveness of automation, mine increasingly growing volumes of data from operations including factory floor equipment, and, as a result, cut costs and boost productivity. In fact, across eight application areas asked about in the survey, AI applied to preventative maintenance of plant floor equipment was clearly the stand-out, with 62% of respondents indicating it as a key application area, the highest by far in the survey. Quality and production planning came in second and third, with 56% and 35%, respectively (Chart 8).

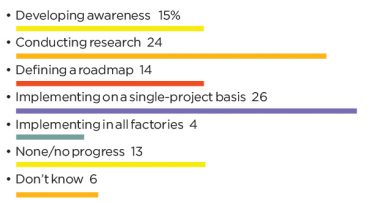

But as it is with all advanced technologies, adopting, implementing, and optimizing their use takes time, and usually more time than initially expected. Right now, just over one-quarter of respondents indicate they are underway with AI on a single-project basis; only 3.6% say they have implemented AI enterprise-wide in all of their factories. Many others are in the process of becoming aware of the technology, conducting research, or defining a roadmap for adoption and implementation (Chart 7).

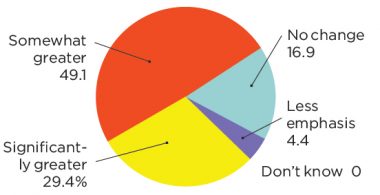

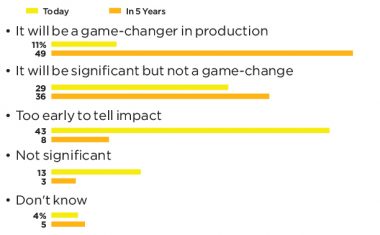

And when MLC asked about the potential impact of AI and its cousin machine learning, an interesting divergence of opinion emerged, one likely influenced by where on the AI maturity curve a company may stand. Today, only 11% of respondents are of the opinion that AI will be a “game-changer” in production. But over the next five years, this number jumps to 48.6%. </p?

On the other hand, 29.3% of respondents today see AI as significant but not a game-changer. Over the next five years, this group grows to 35.7%, but the rate of growth is markedly less than those who believe that AI will indeed be that game-changer the current hype would have us all believe.

Strong Interest in 5G

Other advanced technologies are also showing robust investment intentions.

Among communications and networking technologies, so-called 5G technology, in which only 11.7% of respondents have currently invested, is slated for significant growth over the next two years. By then, 45.9% of survey takers expect that their companies will have invested in the technology.

The Internet of Things, which has a much higher current penetration rate of 51.3%, is also showing strength, with 29.7% saying they will invest in the next 12 to 24 months (Chart 3).

In production technologies, predictive maintenance, plant floor simulation and modeling, and collaborative robots garnered the strongest buying intentions over the next two years (Chart 5). And the adoption of digital thread technology, a key factor in enabling companies to share data across different systems and processes, is also expected to grow strongly (Chart 6).

The Challenges Ahead

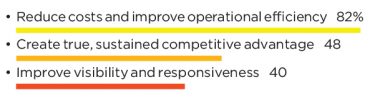

The most important reasons manufacturing companies want to invest in these advanced technologies are that they are looking to reduce costs and improve operational efficiency, improve visibility of operations and create agility and flexibility, and, a result, up their game competitively.

But many face an array of obstacles in reaching these goals. Asked to assess a list of 12 challenges associated with adopting and using transformative technologies, survey respondents indicated that the top three hurdles are migrating from or integrating with legacy systems, assessing cost and benefit of the new technologies, and developing a cohesive M4.0 roadmap (Chart 16).

The roadmap issue continues to bedevil many companies. A lack of a roadmap most likely indicates a low level of digital maturity. It may also reflect that companies may not have figured out how to organize around the digital opportunity.

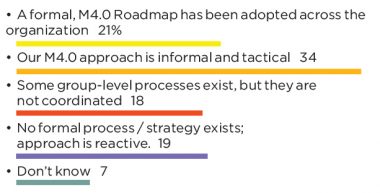

Only about 21% of respondents indicate they have a formal M4.0 roadmap that has been adopted across their organization. About one-third say their approach is informal and tactical and nearly 20% say they really don’t have a strategy at all (Chart 10).

Part of the reason for the lack of organizational cohesiveness around M4.0 may be that responsibility for M4.0 continues to be quite diffused. Who should take the reins in developing a strategy that will affect the entire organization?

Artificial intelligence has captured the imagination of manufacturers by what it promises to do to improve operations.

About 29% of survey takers say that joint IT/OT teams have been charged with responsibility for devising and implementing M4.0 technology strategy and a roadmap, while 27% say that responsibility is the domain of the manufacturing vice president. Another 12.6% say the job rests with their chief operating officer (Chart 11).

As companies strive to sort out the responsibility question, they also struggling with two other key issues – developing M4.0 ROI models that make sense for their companies and finding people with the digital skills that can execute an M4.0 plan (Chart 13). Given the state of the manufacturing workforce, which is still suffering from hundreds of thousands of open jobs, the latter issue may be solved earlier than the former.

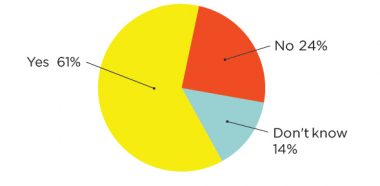

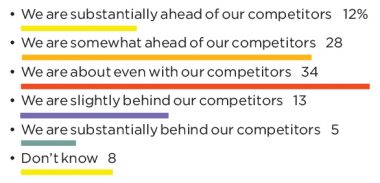

Despite all of the challenges, many companies feel they are in front of or at least keeping pace with competitors in the race for digital advantage. Nearly 40% of survey respondents think they are ahead of their competitors to one degree or another, but only about 11% would say they are substantially ahead. About one-third claim they are even with competitors and about 18% believe they are behind (Chart 15).

In coming months, the race will play out against a backdrop of continued economic uncertainty instigated by the pandemic. The pace of digital technology adoption will certainly be influenced by the larger economic context. It may slow down or speed up depending on the circumstances, but one thing appears certain – the road to the future is digital and nothing, not even a pandemic, will change that. M

Part 1: TECHNOLOGY INVESTMENTS AND PLANS

1 Many to Accelerate IT, OT Spending as a Result of COVID

Q: What effect has the COVID-19 pandemic had on your company’s investment posture for information and operational technologies?

2 Pandemic Spurs Remote Technologies

Q: To what extent has the pandemic accelerated the adoption of technologies that can enable virtual working and remote monitoring of operations?

3 5G, IIoT Slated for Greater Adoption

Q: Please indicate your company’s investment posture for the following communications and networking technologies.

4 AI, Digital Twins Lead in Investment Intentions

Q: Please indicate your company’s investment posture for the following IT-related technologies.

5 Simulation, Predictive Technologies to Further Penetrate Plant Floors

Q: Please indicate your company’s investment posture for the following production technologies.

6 Nearly One Quarter Has Implemented a Digital Thread

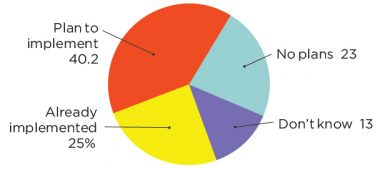

Q: Has your company implemented a digital thread approach to sharing the data generated by one or more of the M4.0 technologies you have adopted?

Part 2: ADOPTION OF AI AND MACHINE LEARNING

7 One Quarter Underway With AI Projects

Q: Where does your company stand today in adopting AI in plants and factories?

8 Preventative Maintenance is Key AI Application

Q: What are the key application areas for AI and Machine Learning technologies in your plants and factories?

9 Nearly a Majority See AI/ML as Game-Changer in Future

Q: What is your current assessment of the potential of artificial intelligence and machine learning, both today and in five years’ time?

Part 3: TECHNOLOGY ASSESSMENT & IMPLEMENTATION PROCESS

10 Only One-Fifth Has Formal M4.0 Approach

Q: Which statement best describes your company’s current approach to adopting a M4.0 technology roadmap or strategy?

11 Joint IT/OT Teams Lead in M4.0 Strategy

Q: Who is responsible for devising and implementing your M4.0 technology roadmap / strategy?

12 Cost Reduction, OpEx Are Top Motivators for M4.0

Q: What are the three most important reasons your company invests in transformative M4.0 technologies?

Part 4: CHALLENGES WITH M4.0

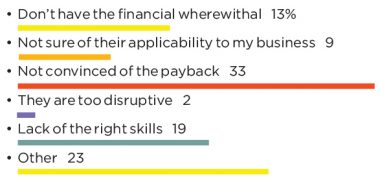

13 Proof of Payback, Skills Are Chief Inhibitors to M4.0

Q: If your company does not invest in M4.0 technologies, what’s the primary reason?

14 A Majority Struggles to Keep Pace With Technologies

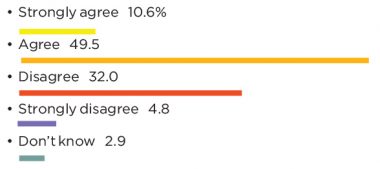

Q: Please indicate the extent to which you agree with the following statement: The accelerating pace at which new technologies are emerging is causing us to fall behind in our efforts to evaluate and understand their potential.

15 A Mixed Bag on Competitive Position on M4.0

Q: Where do you think your company stands in relation to its primary competitors’ adoption of transformative M4.0 technologies?

16 Legacy System Migration is Greatest M4.0 Challenge

Q: How would you assess the following challenges related to adopting and using transformative M4.0 technologies?

17 Few Are ‘Well Prepared’ to Deal With Data Volumes

Q: How prepared is your company to organize, evaluate, and make decisions on the volumes of data that are or will be generated from greater connectivity of devices and equipment?

Survey development was led by David R. Brousell, with input from the MLC editorial team and the MLC’s Board of Governors.

COVID-19 brought a new sense of urgency to digital manufacturing, but M4.0 leadership is still a work in progress, reveals the Manufacturing Leadership Council’s new survey on Next Generation Leadership and the Changing Workforce.

By Penelope Brown

![]()

In many ways, the coronavirus pandemic has forced a reckoning with Manufacturing 4.0 and many of its dimensions. In the technology space, it has meant relying on data to help overcome shifts in demand, supply shortages, and, in some cases, the need to institute remote operations. For organizations, it has meant shifting employees’ physical work locations and implementing sometimes complex social distancing protocols at production sites.

For leadership, however, the reckoning may be most pronounced. When the crisis hit, leaders were charged with making decisions for which there was no precedent. They needed to communicate with their teams and colleagues around the clock. They often needed to set up an entirely new infrastructure to keep operations going. Perhaps most importantly of all, they needed to maintain a calm and measured approach at a time of high anxiety, doing their best to ease employees’ fears when they very likely had many fears of their own.

Part 1: Defining the Leadership Role

1 Leadership means data,

collaboration, and integration

Q: Which statement best describes what leadership means in the Manufacturing 4.0 era?

2 COVID-19 has added urgency to M4.0 investment

Q: To what extent has the COVID-19 pandemic created a greater sense of urgency about M4.0 digitization within your company’s leadership ranks?

3 Most agree that M4.0 leadership requires a different approach

Q: Please indicate the extent to which you agree with this statement: The emergence of the M4.0 era of information-driven factories will require a substantially different approach and set of skills on the part of manufacturing company leadership.