Revisiting M4.0 Maturity at a Critical Juncture in Innovation

Fostering digital maturity means building a strategy where tech investments are made to reach specific goals.

![]()

TAKEAWAYS:

● While many manufacturers associate digital maturity with investing in AI, that investment alone is not a strategy.

● Manufacturers must ask themselves a series of key questions about their desired future state, current shortcomings, and possible challenges.

● Continuous progress means supporting change management and evolving strategies to adapt to shifting needs and priorities.

What is Industry 4.0 Maturity?

Innovation is in manufacturers’ DNA. Technological advancements have enabled the manufacturing industry to increase the speed and complexity of production and remain a primary driver of U.S. economic growth over centuries of change. The printing press enabled the mass production of books. Centuries later, robotic arms allowed manufacturers to assemble thousands of automobiles to exact specifications. Today, advancements in AI are starting to enable manufacturers to engineer better products, improve their decision-making capabilities, glean deeper insights, and automate tasks beyond what was possible before.

Industry 4.0 technologies can help manufacturers gain a better sense of customer needs, boost quality control, improve factory safety, and much more. AI in particular carries promise for businesses to become more agile, efficient, and safe. According to BDO’s 2024 Manufacturing CFO Outlook Survey, 47% of manufacturers will increase investment in AI or machine learning this year. However, investments in AI that are not backed by a business strategy will not guarantee business success, nor do they signify Industry 4.0 maturity.

To nurture Industry 4.0 maturity, manufacturers need to develop a business strategy where investments in technology are made to reach specific business goals. For example, a more Industry 4.0 mature manufacturer would evaluate how AI could augment their existing Industry 4.0 strategy, and pilot use cases before rolling it out more broadly. A nonstrategic manufacturer would pour resources into expensive AI tools without giving much thought to which goals the tools could achieve.

“Investments in AI that are not backed by a business strategy will not guarantee business success, nor do they signify Industry 4.0 maturity.”

As competitors tout AI investments, manufacturers are under pressure to keep up and appease stakeholders asking about their own AI investments. To stay competitive, leaders will need to separate AI hype for real growth opportunities. AI can power a growth strategy, but investing in AI alone is not a strategy. Instead, manufacturers should take the opportunity to revisit their Industry 4.0 strategies, assess AI opportunities, and determine their capacity to pivot their approaches.

Developing Industry 4.0 Goals

Before a manufacturer launches or revisits an Industry 4.0 initiative, it is crucial that their teams identify the challenges they want to address — what is the desired future state? What internal and external dynamics have contributed to the current gap? What is likely to impede realizing the future state? Only once manufacturers have answered these questions can they begin to articulate their goals and create a quality list of stakeholders.

Below is a hypothetical scenario where a U.S.-based furniture manufacturer asks these important questions to develop their Industry 4.0 goals.

Question 1: What is the desired future state?

This manufacturer wants to have its finger on the pulse of evolving consumer demands and develop the capacity to capitalize on those market opportunities with new products. The company’s customers are increasingly swayed by what they see on social media, trend cycles are shorter, and shoppers want the latest designs immediately. If this company cannot speed up, it will lose market share to its more agile competitors.

Question 2: What internal and external dynamics have contributed to the current gap?

The organization lacks the capabilities to track consumer behavior data in real-time, and even for the data that it does have, it does not possess the analytics capabilities necessary to extract insights from that information. Additionally, the company does not have the operational agility to pivot product strategy to capture new trends in furniture design.

Question 3: What is likely to impede realizing the future state?

To achieve the desired future state, the furniture manufacturer will have to invest in its data analytics capabilities. This includes its ability to capture data, particularly consumer data, from around the business. To extract meaning from this data, the company would need to invest in AI tools to develop deeper insights into consumer behavior. To allow the AI to work with its data analytics tools, the manufacturer will need to consolidate data from across the enterprise into one well-governed source of truth. The company will also need to hire and train the right people to stand up the AI program and refine AI-derived insights into an action plan.

After improving its analytics capabilities, the manufacturer may discover that there are potential customers it has not reached, or that their existing customer base’s buying behaviors are evolving. However, even after uncovering these insights, it will need to determine whether it’s profitable to act on them. For example, it will need to consider the cost and time needed to develop new designs, get those designs into production, evaluate prototypes for quality, and then bring them to market before the trend peaks. Making this kind of product pivot fast requires significant operational agility and can be costly.

Gathering Input

When starting an Industry 4.0 initiative, teams should solicit ideas and concerns from their stakeholders in a joint problem-solving effort. It is also important to gather insights from cross-functional leadership to get a full picture of potential gaps in the business strategy, as well as align the direction of the business strategy with its technology investments.

If those leading an Industry 4.0 initiative demand perfection, it puts pressure on the teams tasked with achieving an ideal future state. A defined vision is important, but teams that adopt an agile approach to goal setting may be more successful. Leaders can help prime their teams for change by helping them understand that goals should always be informed by business needs, which are almost always evolving.

Supporting Change Management

Companies that are the more mature in Industry 4.0 appreciate that change management is a continuous process that does not start or end with the launch of an initiative. This means change management tactics should be used throughout the industry 4.0 initiative to create all-important buy-in.

“Manufacturers should revisit their Industry 4.0 strategies, assess AI opportunities, and determine their capacity to pivot. ”

One tactic that may be particularly effective in engaging stakeholders, gathering critical insights, and building support is conducting a pre-mortem. This exercise involves scenario-mapping the initiative two, three, or five years from now and observing two potential outcomes: success and failure. In each scenario, stakeholders articulate the details of the future they imagine. For example, a failure scenario might be ‘reliability is low,’ or ‘costs have risen to unsustainable levels.’ Then the team would list the challenges they faced and what they could have done differently to avoid or mitigate failure. When scenario-mapping success, stakeholders also document what success looks like, such as growth or lower marginal costs, and the steps that were critical to achieving those outcomes.

Through this iterative exercise, leaders of Industry 4.0 initiatives can gain important insights from stakeholders and increase buy-in for the initiative. By exploring failure, skeptics are given plenty of space to articulate their concerns and opportunities to document what the company could do to increase success, even in a worst-case scenario.

Evolving Your Industry 4.0 Strategy

As a manufacturer’s needs evolve, so should its Industry 4.0 strategy. Before considering a shift in Industry 4.0 strategy, manufacturers should ask themselves: Where do we need to grow? How can new technologies amplify these growth objectives? Where do we need to defend our market position? How can new technology help us outpace competitors?

The furniture manufacturer described earlier needed to improve its data analytics and demand forecasting capabilities to tap into trend-focused consumers. With the rise of AI, it evolved its Industry 4.0 strategy to integrate AI to improve its ability to understand the desires of customers.

Manufacturers should educate themselves about the latest advancements but avoid pursuing any new technology or idea without careful forethought and planning. Leaders should challenge themselves and their teams to think broadly and creatively about their current limitations and potential but avoid locking in on a specific solution without rigorous root cause analysis.

Agility and Communication

Even among capable organizations, the process to adopt a new Industry 4.0 strategy comes with challenges. To help prepare and reduce the impact of these issues, leaders should foster resilience within the organization, as employees will likely need to pivot mid-stream.

A common complaint from middle managers and front-line employees is that they do not understand the strategy behind the initiatives that are adopted or shelved. When these employees do not have sufficient understanding, they become disengaged and lose faith in leadership. However, delivering the necessary level of transparency is far from easy.

“When starting an Industry 4.0 initiative, teams should solicit ideas and concerns from their stakeholders in a joint problem-solving effort.”

Once the organization has committed to a specific direction, there is often significant inertial pressure to continue in that direction, even when that direction isn’t delivering desired results. To stay on the right path, leaders of Industry 4.0 initiatives should define metrics and collect data to determine whether the strategy is working for the organization. These metrics force teams to monitor for signs the strategy isn’t working as intended from the outset and greatly increase the speed and quality of decision-making.

For example, a manufacturer may use predictive analytics to create a maintenance schedule for all equipment in one of their plants. Predictive maintenance can help improve efficiency by allowing more maintenance to happen during planned downtime. But while the manufacturer had good intentions, the investment ran into issues in implementation – setup was costly, frontline workers were not adequately trained on how to use the new system, and while there were some successes in detecting problems before they grew to be a major issue, the time and resources spent far outweighed the benefits.

The leaders of this company were determined to make it work and decided to call the pilot a success and roll it out to other plants, where similar issues occurred. If the leaders instead had taken a step back to reevaluate their approach and triage the challenges, they could have found a solution that was worth rolling out to other plants or stopped the project before costs spiraled.

Preparing for the Future

As technological innovation continues, manufacturers need to remain disciplined in their approach to technology. Successful manufacturers will treat any new advancement the same as they always have by revisiting their Industry 4.0 strategy, determining if the new tool can help them achieve their goals, and assess how they need to pivot.

At companies that have greater Industry 4.0 maturity, strategy is not set in stone. It is continually evolving and adaptable. Leaders regularly discuss changes in the marketplace and their implications with teams so employees begin to understand the nuances. Ultimately, companies with more advanced Industry 4.0 maturity are often met with employee enthusiasm and a readiness to embrace evolving strategies for an evolving world. M

About the authors:

Val Laufenberg is Management Consulting Market Leader at BDO USA

Maurice Liddell is Manufacturing Market Leader at BDO Digital

Jessica Wadd is Strategy & Innovation Segment Leader at BDO USA

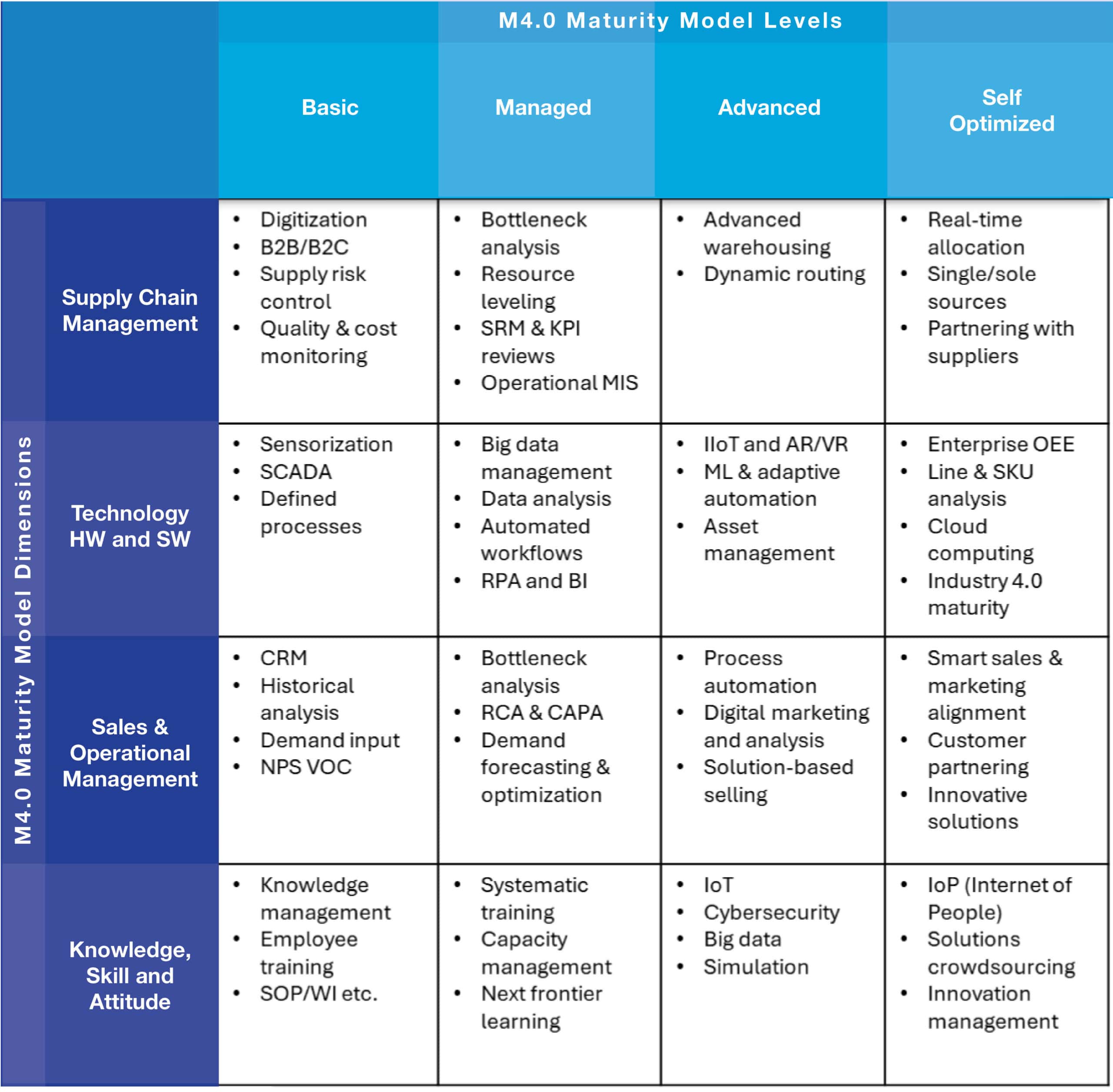

Unlocking Manufacturing Excellence with the M4.0 Maturity Model

The M4.0 maturity model offers manufacturers a thorough and effective way to evaluate current and desired maturity levels.

![]()

TAKEAWAYS:

● The M4.0 maturity model assesses readiness and capabilities across four dimensions: supply chain management, technology, sales and operational management, and knowledge, skills, and attitude.

● The M4.0 maturity model offers a structured approach to evaluate the current state, set realistic goals, and remain on a path of continuous improvement.

● By using the model, companies can uncover valuable information about their current and desired maturity levels, including gaps and areas for growth.

Navigating the complexities of new technology adoption and process improvement, many organizations (particularly small and medium-sized enterprises) are often hindered by the diverse maturity levels across key organizational dimensions. Challenges range from bridging the gap between strategic vision and execution due to skill and cultural gaps, to aligning advanced technology investments with the right organizational structures. The Manufacturing 4.0 (M4.0) maturity model emerges as a pivotal framework, offering companies a structured approach to evaluate their current situation, set realistic goals, and remain on a path of continuous improvement across critical areas. In this article, we explore the strategic impact of the M4.0 maturity model on the journey to manufacturing excellence.

What Is the M4.0 Maturity Model?

The M4.0 maturity model serves as a framework designed to assess the readiness and capabilities of organizations across four main dimensions:

1. Supply Chain Management

2. Technology (Hardware and Software)

3. Sales and Operational Management

4. Knowledge, Skill, and Attitude

The model also lays out four maturity levels within the M4.0 spectrum, from basic awareness to the self-optimization of practices throughout the value chain. It empowers organizations to take meaningful steps towards enhancing their operational performance and competitive stance within their industry.

Why Implement the Model?

The M4.0 maturity model offers a nuanced way to evaluate the health and potential of your business, or specific projects, moving beyond mere goal achievement to assess their capacity, respectively, for continuous improvement. This model excels where traditional models may fall short, as it can interpret qualitative data to determine a company’s long-term trajectory and performance. By defining different levels of effectiveness, it can identify the current position of any person, team, project, or company within the model.

“It [the M4.0 maturity model] empowers organizations to take meaningful steps towards enhancing their operational performance and competitive stance within their industry.””

Implementing the M4.0 maturity model can reveal valuable information about a company’s performance and potential, highlighting areas for learning and growth by bridging the gap between the current and desired maturity levels. Let’s explore the model’s structure, starting with its levels and then its dimensions.

M4.0 maturity model levels

- Basic: Characterized by a reactive approach, the organization has minimal visibility and control over its processes; it relies on manual and compartmentalized systems, which limits its flexibility to changes and opportunities.

- Managed: The organization adheres to some established standards and best practices, using basic tools and technologies for process oversight and enhancement. It can navigate some changes but struggles with cross-functional coordination and collaboration.

- Advanced: With the adoption of tools like cloud computing, the Internet of Things (IoT), artificial intelligence (AI), and big data analytics, the organization has high visibility and control, allowing it to proactively optimize operations. At this level, the organization demonstrates a culture of innovation and continuous improvement across functions and partners.

- Self-optimized: The organization is a leader in its industry, with significant competitive advantages in quality, efficiency, agility, and customer satisfaction. It leverages cutting-edge tech, such as digital twins, blockchain, and 5G, to create smart and connected offerings. It’s also highly adaptable and resilient, excelling in new market ventures and opportunity capitalization. Organizations at this level take their culture of innovation and continuous improvement to the next level, setting a standard for a culture of excellence and empowerment across functions and partners.

M4.0 maturity model dimensions

- Supply Chain Management: Measures the effectiveness of managing the supply chain from sourcing to delivery, aiming to meet customer needs proficiently.

- Technology: Assesses the integration of relevant technologies to boost operational efficiency and product/service quality.

- Sales Operation Strategy: Evaluates how well the sales strategy aligns with business objectives and customer segmentation, focusing on resource and process optimization.

- Knowledge, Skill, and Attitude (People and Culture): Gauges the development and engagement of human capital, both internally and externally, in alignment with the organization’s vision, mission, and values.

We present the full M4.0 maturity model matrix (Figure 1).

Figure 1: The Full M4.0 Maturity Model matrix

M4.0 Maturity Model FAQs

Q: Is striving to reach the “Self-optimized” level necessary for all companies using the maturity model?

A: While not every company may need to reach the “Self-optimized” level across all dimensions, focusing on key areas where M4.0 technologies can drive significant competitive advantage remains crucial. The implementation of IoT solutions, for instance, allows companies to visualize overall equipment effectiveness (OEE) metrics through easy-to-use dashboards, gain real-time insights into production, and optimize processes. Activities like this can significantly enhance manufacturing efficiency and sustainability, despite being much closer to the “Advanced” level than they are to the “Self-optimized” level.

Q: How does this model, which may seem theoretical, get put into practice?

A: The model primarily serves as a benchmarking tool, allowing companies to compare technology domains across different areas and maturity levels with their current operational state and future goals. This comparison highlights gaps in digital capabilities, illuminating areas ripe for strategic improvement. The real shift from theory to practice occurs when companies begin the phases of adoption, after reaching a consensus on their focus areas and desired technologies. At this point, navigating this transformation involves working with the right partners, adapting management strategies, and ensuring technological integration that goes beyond mere adoption to fully embedding these advancements into the organizational fabric. For more on the practical application of the M4.0 maturity model, see our article “Four Steps to Scale M4.0 Adoption Organization-Wide.”

“Ultimately, it [the model] guides companies through incremental improvements, both in the short and long term, ensuring that enhancements contribute to a unified vision.”

Q: What is the role of plant managers within the model?

A: Plant managers play a crucial role in the digital transformation journey within manufacturing facilities. As digital technologies are increasingly adopted, plant managers emerge as essential leaders of this shift. Their responsibilities extend across several key areas: leading change, integrating data across systems, managing transitions smoothly, and supporting collaboration among teams. As adoption leaders, plant managers ensure their teams are aligned and equipped to excel as the manufacturing technology environment evolves.

Q: Which key performance indicators (KPIs) should a company track when applying the model?

A: Companies should monitor KPIs that align with the model’s four areas, ensuring a holistic view of progress and areas for continuous improvement:

- Supply Chain Management: Focus on KPIs like lead times, inventory turnover rates, supplier performance metrics, and logistics cost to gauge efficiency and responsiveness.

- Technology (Hardware and Software): Track system uptime, response times, frequency of software deployments, and rates of security incidents to evaluate the reliability and efficiency of technological infrastructure and workflows.

- Sales and Operational Management: Measure sales performance, customer satisfaction levels, order fulfillment speeds, and revenue growth to assess the effectiveness of sales strategies and operations.

- Knowledge, Skill, and Attitude: Mature organizations invest in continuous learning and empower employees to contribute effectively. Monitor employee training completion rates, progress in skill development, and employee engagement scores.

Q: How does the model, which categorizes maturity into separate areas and levels, promote organizational integration and visibility?

A: The model, while visually segmented, is designed to promote holistic organizational growth. Its structure allows companies to assess and advance each area systematically without losing sight of overall operational cohesion. By providing clear benchmarks for each area, at each area, at each maturity level, the model enables organizations to see how progress in one segment influences and is influenced by others, fostering end-to-end visibility and integration. Ultimately, it guides companies through incremental improvements, both in the short and long term, ensuring that enhancements contribute to a unified vision.

M4.0 Maturity Model in Action: A Case Study in the Cable Sector

We present a brief case study to demonstrate how the M4.0 Maturity Model works in action.

Challenge

Amidst significant SAP implementations across new plants, our client faced challenges in goal setting and project management due to uneven technology adoption. While advanced systems were deployed in some departments, other areas remained heavily reliant on manual processes, lacking real-time data and streamlined operations. This challenge, a common issue in Latin American markets, hindered operational efficiency and adaptability.

“By leveraging the M4.0 maturity model, companies can unlock manufacturing excellence, enhance operational performance, and secure a competitive advantage within their industry.”

Our Approach

We leveraged a proprietary solution accelerator to integrate IoT sensors with the client’s existing programmable logic controllers and SAP systems and funnel insights into powerful efficiency dashboards. While a more conventional approach would involve developing solutions on one of the main cloud platforms, this often leads to extended project timelines and complex integration processes. Given the client’s concurrent project engagements, they were particularly averse to the risks associated with extensive development and integration phases. By aligning our solution accelerator with the client’s current technological ecosystem, we accelerated adoption timelines while significantly reducing the likelihood of operational disruptions.

Impact

Integrating IoT with the client’s systems propelled them from a basic to an advanced level within the Technology dimension of the M4.0 maturity model in just a few months. This transformation not only showcases the potential for swift operational efficiency improvements using solution accelerators but also highlights the important balance between innovation and execution. By embedding advanced technology within existing infrastructures, this phased approach to adoption bypassed the need for extensive system overhauls.

M4.0 Is a Powerful Framework

The M4.0 maturity model emerges as a powerful framework for navigating the complexities of new technology adoption and process improvement in manufacturing. By offering a structured approach to assess readiness and capabilities across critical dimensions such as supply chain management, technology, sales and operational management, and knowledge, skills, and attitude, the M4.0 model empowers organizations to set realistic goals and embark on a journey of continuous improvement. Through its four maturity levels and comprehensive dimensions, the model serves as a benchmarking tool, guiding companies towards incremental enhancements and fostering a culture of excellence and empowerment. By leveraging the M4.0 maturity model, companies can unlock manufacturing excellence, enhance operational performance, and secure a competitive advantage within their industry. M

About the authors:

Roberto Cisneros is director of IIoT Solution Architecture at Softtek.

Krishnan Venkat is director of Supply Chain Consulting at Softtek.

How Close Is the Smart Factory of the Future?

Manufacturing is marching toward a future that is highly automated, intelligent and flexible.

Increasingly, smart factories are made up of connected machines that generate large amounts of data. This opens the door for artificial intelligence–driven analysis and new opportunities for insights on improving supply chains, processes, the customer experience, product quality and more.

But realizing this transformation can be difficult. Not all manufacturers have the resources, capital or talent required for a smart factory future. How are companies progressing on this journey, and what challenges stand in the way? To find out, the Manufacturing Leadership Council—the NAM’s digital transformation arm—conducted its Smart Factories and Digital Production survey.

Manufacturers are committed to M4.0: When it comes to digital technology, manufacturers are spending at a steady—and in some cases growing—basis.

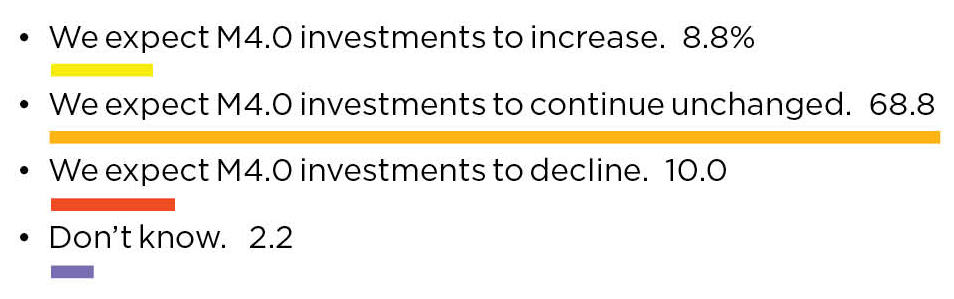

- Nearly 69% of survey respondents said their M4.0 investments this year would continue unchanged from last year.

- Nearly 19% said they would increase investments, while just 10% said their investments would likely decline.

- Some 58% assessed their company’s digital maturity level in manufacturing operations at three to five on a scale of 10, suggesting the industry has moved beyond the initial stages of M4.0 and has reached an early majority of digital-model adoption.

How widespread are digital factories? Only about 7% of manufacturers say they have digitized their factory operations extensively.

- Approximately 15% expect to have their manufacturing operations digitized end-to-end by 2026.

- About 5% say their factories are already “very smart.”

- Approximately 53% say their factories and plants are getting smarter but are still works in progress.

In the future, will factories run themselves? While some manufacturers foresee a future of “lights out” factories, or those that mostly run themselves, most don’t think they will ever reach that state.

- About 49% of respondents expect fully or partially autonomous factories in the future.

- Some 40% say AI will be either very significant or somewhat significant in the years to come.

- Approximately 56% cite organizational resistance to change as the top barrier to implementing a smart factory.

For more details on these findings and the impact of smart factories as a whole, read the survey report: Smart Factories Are Still a Work in Progress.

What’s Ahead for Manufacturing in 2024?

Getting a solid forecast of the year’s key issues in manufacturing can help your business prepare for anything. A panel of experts recently shared their 2024 outlook in the webinar “What’s Ahead for Manufacturing in 2024?” hosted by the Manufacturing Leadership Council, the NAM’s digital transformation arm.

They offered insights on the 2024 manufacturing economy, legislative climate, digital trends, resilience strategies and more.

Economic outlook: NAM Chief Economist Chad Moutray provided a manufacturing economic update.

Key takeaways:

- The NAM Q4 2023 Manufacturers’ Outlook Survey revealed that more than 66% of member companies have a positive economic outlook for 2024, yet opinions are mixed on whether there will be a recession.

- The top economic challenge this year will be the workforce, with the labor market cooling substantially but remaining tight, Moutray said.

- Private manufacturing construction spending is at an all-time high of $210 billion thanks to the production of semiconductors, electric vehicles and batteries, and general reshoring.

- Risks this year include geopolitical turmoil, slow global economic growth, cost pressures, talk of a recession and labor issues, among others.

Policy perspective: NAM Vice President of Domestic Policy Charles Crain gave an overview of the current climate in Washington, D.C., and the NAM’s legislative priorities.

Key takeaways:

- The NAM will continue its focus on tax policy following House passage of an NAM-supported bipartisan tax package that would reinstate three manufacturing-critical tax provisions.

- Manufacturing is facing a regulatory onslaught, with the average manufacturer paying $29,000 per employee per year due to unbalanced, burdensome regulations, according to a recent NAM-commissioned study.

- Artificial intelligence is a hot topic on Capitol Hill, with 60 AI-related bills introduced in Congress last year. The NAM is working to help policymakers understand the benefits of AI, including safety, worker training, product design and development, and efficiency.

Manufacturing 4.0 Trends: MLC Senior Content Director Penelope Brown offered a look at digital manufacturing trends on the horizon.

Key takeaways:

- Manufacturers can expect to see a broader adoption of existing AI applications, including predictive/preventative maintenance, improved processes and enhanced productivity.

- According to the MLC’s recent Smart Factories and Digital Production survey, 65% of manufacturers anticipate their level of M4.0 investment this year will stay the same as last year.

- Other trends to watch include the rise of global partnerships such as Catena-X and CESMII, digitized supply chains and reshoring.

Resilience perspective: Cooley Group President and CEO (and MLC Board of Governors Chair) Dan Dwight shared his approach to resilience in 2024 and the years to come.

Key takeaways:

- Business leaders should prioritize agility and adaptability, even if it means admitting to suboptimal results that require redirection.

- Resilience doesn’t mean perfection; it means learning from failures.

- AI and machine learning contribute to resilience by building out end-to-end visibility across an organization—from vendors to manufacturing operations to customers.

For additional details from these experts, watch “What’s Ahead for Manufacturing in 2024?”

What’s Ahead for Manufacturing in 2024?

Getting a solid forecast of the year’s key issues in manufacturing can help your business prepare for anything. A panel of experts recently shared their 2024 outlook in the webinar “What’s Ahead for Manufacturing in 2024?” hosted by the Manufacturing Leadership Council, the NAM’s digital transformation arm.

They offered insights on the 2024 manufacturing economy, legislative climate, digital trends, resilience strategies and more.

Economic outlook: NAM Chief Economist Chad Moutray provided a manufacturing economic update.

Key takeaways:

- The NAM Q4 2023 Manufacturers’ Outlook Survey revealed that more than 66% of member companies have a positive economic outlook for 2024, yet opinions are mixed on whether there will be a recession.

- The top economic challenge this year will be the workforce, with the labor market cooling substantially but remaining tight, Moutray said.

- Private manufacturing construction spending is at an all-time high of $210 billion thanks to the production of semiconductors, electric vehicles and batteries, and general reshoring.

- Risks this year include geopolitical turmoil, slow global economic growth, cost pressures, talk of a recession and labor issues, among others.

Policy perspective: NAM Vice President of Domestic Policy Charles Crain gave an overview of the current climate in Washington, D.C., and the NAM’s legislative priorities.

Key takeaways:

- The NAM will continue its focus on tax policy following House passage of an NAM-supported bipartisan tax package that would reinstate three manufacturing-critical tax provisions.

- Manufacturing is facing a regulatory onslaught, with the average manufacturer paying $29,000 per employee per year due to unbalanced, burdensome regulations, according to a recent NAM-commissioned study.

- Artificial intelligence is a hot topic on Capitol Hill, with 60 AI-related bills introduced in Congress last year. The NAM is working to help policymakers understand the benefits of AI, including safety, worker training, product design and development, and efficiency.

Manufacturing 4.0 Trends: MLC Senior Content Director Penelope Brown offered a look at digital manufacturing trends on the horizon.

Key takeaways:

- Manufacturers can expect to see a broader adoption of existing AI applications, including predictive/preventative maintenance, improved processes and enhanced productivity.

- According to the MLC’s recent Smart Factories and Digital Production survey, 65% of manufacturers anticipate their level of M4.0 investment this year will stay the same as last year.

- Other trends to watch include the rise of global partnerships such as Catena-X and CESMII, digitized supply chains and reshoring.

Resilience perspective: Cooley Group President and CEO (and MLC Board of Governors Chair) Dan Dwight shared his approach to resilience in 2024 and the years to come.

Key takeaways:

- Business leaders should prioritize agility and adaptability, even if it means admitting to suboptimal results that require redirection.

- Resilience doesn’t mean perfection; it means learning from failures.

- AI and machine learning contribute to resilience by building out end-to-end visibility across an organization—from vendors to manufacturing operations to customers.

For additional details from these experts, watch “What’s Ahead for Manufacturing in 2024?”

Connect, Analyze, Improve — Then Rinse and Repeat

A focus on connecting equipment and then using data to make improvements can create a solid foundation for smart manufacturing.

![]()

TAKEAWAYS:

● While manufacturers have embarked on the M4.0 journey and expect it to accelerate, many are still struggling with where to begin.

● A good place to focus is on connecting equipment and then using the data and AI to make improvements in operations.

● As pilot projects build organizational confidence and knowledge, the lessons learned can be applied to other areas of the business.

From conversations at the Manufacturing Leadership Council’s December 2023 Manufacturing in 2030 event, it became clear that the industry is still far from delivering on the vision of Industry 4.0. Although we have been discussing the value of industry 4.0 for over 20 years, companies continue to be challenged on how to drive progress – and for some on even how to get started.

There’s a natural tendency to want to have a cohesive plan or strategy for moving ahead. In the MLC’s recent study, Manufacturers Go All-In on AI, 42% of manufacturing executives cited the lack of comprehensive M4.0 strategy as the top challenge to adopting and using those technologies. Another 37% said the biggest hurdle is their ability to assess the cost/benefit of deployment.

Navigating through the wide array of technologies to develop a M4.0 strategy is challenging. Thinking too broadly can lead to analysis paralysis; thinking too narrowly can make it difficult to demonstrate a level of ROI that warrants investment—especially in the current economic climate.

Cooley Group president and CEO Dan Dwight spoke at the event and offered advice that resonated: “Just get started.”

What does that mean? In our experience working with manufacturing organizations to become digital, making positive strides doesn’t have to be complicated or time-consuming, or even expensive. Find a clear business problem — increasing throughput by improving overall equipment effectiveness or reducing costs by improving quality — that can be solved with better or more timely data from your equipment. Gather data from the equipment involved and analyze that data using a readily available technologies like an industrial AI operating system consisting of an edge platform (data collection), machine learning platform (data analytics), and cloud platform (data management) for a hybrid unified analytics experience. Manufacturers win when they trust their digital partners (system integrators) in deploying these technology solutions in production, at scale.

When done well, this not only solves a problem but also creates a foundation for expanding beyond the pilot and exploring more opportunities to benefit from the technology investment and what your organization has learned.

A Case Study in “Just Get Started”

Our partnership in working for a pet food manufacturer highlights the potential for this approach.

Pet adoptions swelled during the pandemic, accelerating the company’s already rapid growth and challenging its ability to meet demand. Management wanted to increase operational agility to respond better to shifts in demand.

A rapid assessment of operations revealed an opportunity to pilot smart manufacturing technology to better understand what was happening on production lines, including machine availability, to improve efficiency and throughput. We used an industrial automation platform to connect 31 machines across four departments to gather and analyze performance data.

“Thinking too broadly can lead to analysis paralysis; thinking too narrowly can make it difficult to demonstrate a level of ROI that warrants investment.”

This allowed frontline leaders to visualize what machines were doing: Were they up, down, or idle when not expected? Engineers could then look more closely at potential maintenance or other issues. For example, the cumulative production volume would briefly zero out. Further analysis found that trays were getting stuck, thus shutting down the line. Through investigation, we found that operators had performed a hard shutdown of the line to clear the issue, which had negative consequences for the computer equipment. This is a prime example of how root cause analysis, enabled by insight from machine data, helped the company identify and take action for technical, behavioral, and process issues.

The project coupled data insights from the connected equipment with basic management practices to develop new metrics and scorecards, controls, and communication processes across functions and shifts so that employees from management to the shop floor had access to the right data and could use it to optimize operations. Because the machines are connected and delivering real-time data, teams can now see production line status and take action closer to real-time, all without the need for manual data collection.

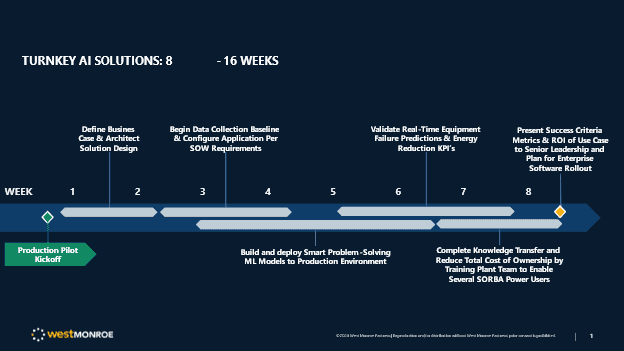

This solution was simple to set up, allowing us to begin connecting machines within eight weeks. Within 16 weeks, the company was using data to improve its production loss tracking process. The increased throughput translated to an estimated $13 million in incremental capacity, and the project paid for itself within 16 weeks — 10 weeks before it ended. This allowed extra attention to change management to increase knowledge, ownership, and buy-in.

It’s important to reinforce that this was the company’s first foray into smart manufacturing. Four key factors made our efforts successful:

- Identifying a specific and focused business problem and goal for the insight required to address the problem

- Getting buy-in from management to “just get started” as opposed to ongoing debate on the potential value

- Employing available technology to gather the data required

- Using analysis to make operational changes, addressing the people side of change as well as the technology

With this success, the company now had a M4.0 foundation on which it could continue building.

A Case Study in Building on the Foundation

This particular application of M4.0 technology can address multiple operational needs and goals around predictive maintenance, quality control, supply chain optimization, and energy efficiency and sustainability.

In a report for the U.S. Department of Energy, the Lawrence Berkeley National Laboratory studied motor systems in the industrial and commercial building sectors. Among the findings: 75% of industrial motor system electricity consumption is attributed to 1-1500 hp motor systems; however, a lack of sufficient data is a major barrier to capturing energy savings potential in these motor systems. With the increasing pressure on mid-market manufacturers to demonstrate their efforts to curb carbon emissions by their customers, energy monitoring and reduction in manufacturing operations benefits both the top-line and bottom-line.

Starting the journey with a focus on energy efficiency often leads to opportunities to use the same technology to derive benefits in other areas. This has been the case for a Fortune 100 food and beverage company. The organization wanted to reduce fuel waste in high-use assets like compressors and boilers, particularly the steam consumption of wort kettles. In this case, lack of machine data and insights prevented the company from addressing this issue effectively.

The company wanted to pilot a program that allowed real-time AI industrial optimization techniques to improve energy consumption and efficiency, using a platform that would work in different brewery environments. The focus of the pilot project centered around using the SORBA.ai platform to connect the following energy and fluids functions (machine profiles):

- Compressors (ammonia and air) and condensers

- Boilers (biofuel and natural gas), filtration skids, and wort kettles

- Heat exchangers, cooling towers, HVAC equipment, and co-gen turbine engines

The goal for the AI was to optimize performance and improve machine efficiencies, which directly correlates to a reduction in energy consumption. The AI allowed the company to autonomously draw and analyze real-time data to produce insights for optimizing the control of equipment use.

In conjunction, the company equipped 200+ front-line AI users — including developers, engineers, operators, and consultants — with enhanced skills and digital tools to abstract insight, use it to optimize operations, and sustain that performance over time.

“Starting the journey with a focus on energy efficiency often leads to opportunities to use the same technology to derive benefits in other areas.”

The pilot project reduced fuel and electricity consumption by 5-10%, translating to $100,000 in annual savings per facility/per two use cases—generating a 5x return on investment in less than two years.

More significantly, what started as an energy efficiency project has today grown to include use cases and benefits in other parts of the business:

- Offset of carbon emissions per ton reporting, validated by Department of Energy audits.

- Production capacity increases. By using the same AI technology to optimize control of filtration skids, the company removed capacity constraints, maximizing material flow. As a result, it was able to produce hundreds more barrels of product per specialized membrane filter machine, per production run. This increased production throughput equates to a forecasted gain of $50 million in revenue realized over five years.

- Supply chain optimization. The company reduced technical debt (custom models, rework, data integration) across the supply chain by 33% from raw material (harvested grains) to packaging (bottled and shipped product).

- Quality control. An ancillary benefit of reducing energy through AI process optimization technology helped quality control technicians responsible for the wort kettle process analyze random batch samples and reduce protein coagulation in real-time.

Build the Foundation while Building the Future

Connecting equipment and leveraging machine data is a great way to begin building the foundation for smart manufacturing, and move in the direction of robust strategy around advanced capabilities such as digital twin or simulation. It also helps the organization increase M4.0 maturity, as people learn to use insight and optimize operations.

If you’re struggling with where to focus effort or even where to begin, you aren’t alone. A good way to establish and build momentum is to focus on connecting equipment to gather and use data. Find a use case. Use available technology to connect equipment and gather data. Then analyze the data, learn, apply what you’ve learned, and repeat. As you do, you’ll see the momentum begin to build as the data leads you. M

About the authors:

Randal Kenworthy is Senior Partner, Consumer & Industrial Products at West Monroe

Kris Slozak is Director, Consumer & Industrial Products at West Monroe

AJ Alexander is Managing Director at Sorba.ai

Safeguarding Smart Manufacturing Against Cyberattacks

Placing risk management and threat scenario planning at the intersection of smart manufacturing and cybersecurity can fortify organizations.

![]()

TAKEAWAYS:

● The arrival of smart manufacturing, driven by AI and advanced technologies, necessitates a paradigm shift in how manufacturers approach cybersecurity.

● Manufacturing systems and facilities are interconnected, making them vulnerable to cyberattacks that can exploit systems at scale.

● Manufacturers can safeguard against cybersecurity threats by leveraging threat scenarios and adopting vigilant but practical risk management practices.

Manufacturers are increasingly leveraging AI-driven or smart manufacturing technologies to enhance their production processes and improve their bottom line. As businesses chart their course for the next five years, data analytics, increased automation, and the adoption of smart manufacturing and cloud technologies are driving forces for growth. Predictive maintenance, quality control, inventory management, supply chain optimization, and autonomous robots are revolutionizing manufacturing by boosting efficiency, quality, and safety. According to the Rockwell State of Smart Manufacturing Survey, most organizations recognize the importance of smart manufacturing, with 45% planning to adopt it within the next year and an additional 39% within 1-2 years. Over 50% more manufacturers are using machine learning and AI technologies than just a year ago, so the transformation is accelerating quickly. In fact, the Manufacturing Leadership Council’s 2023 Transformative Technology survey reveals that 63% of respondents expect Manufacturing 4.0 technology adoption to accelerate in the next two years.

All these transformative technologies share a common requirement: the need for a fortified cybersecurity strategy. Manufacturers must recognize cybersecurity as an integral component of their digital transformation journey. It is not just an afterthought, but rather the first and last question on the journey toward realizing smart manufacturing’s full potential. Establishing a robust cybersecurity strategy involves setting up the right governance structure, integrating technology with people, and focusing on progress over perfection.

The Complexity of Manufacturing Systems

Manufacturing systems are intricately interconnected, making them susceptible to cascading impacts in the event of a cyberattack. As technology evolves, manufacturers are moving from heterogeneous to homogeneous infrastructures, transitioning from purpose-built control system environments with different integrators, OEMs, and profiles to common operating systems, network protocols, and software stacks.

An attack on one system can reverberate through an entire plant, resulting in substantial revenue losses. The similarities between environments also provide an unintended advantage for adversaries – the learning curve is easier, and groups can develop impactful malware at scale.

“An attack on one system can reverberate through an entire plant, resulting in substantial revenue losses.”

The consequences of cyberattacks on manufacturing operations can be far-reaching and detrimental, affecting key components for operations, productivity, and safety. Depending on the malware functions and attack intentions, attacks can target manufacturing operations by affecting any of the three main systems of a plant:

- Manufacturing Execution Systems (MES): MES systems play a pivotal role in data interchange between business and operations, making them prime targets for cyberattacks.

- Plant Floor Assets: Assets like Human Machine Interfaces (HMIs) and controllers are indispensable for controlling equipment and processes. Disruption of these systems can bring manufacturing production to a standstill.

- Enterprise Resource Management (ERP): ERP systems, centralizing plant data, downtimes, and production constraints, are crucial to the manufacturing industry’s corporate side.

These interdependencies underscore the importance of threat scenarios as essential components of cybersecurity planning for operational technology environments.

Threat scenarios simplify the process of risk assessment by identifying and prioritizing vulnerabilities that hold the utmost relevance in your specific environment, thus aiding in the allocation of resources. Simulated threat scenarios serve as litmus tests for assessing your level of preparedness, enabling manufacturers to pinpoint security control gaps effectively. By using realistic scenarios, you can strategically engineer your architectures to defend against the most probable Tactics, Techniques, and Procedures (TTPs).

Threat scenario analysis concentrates the deployment of security controls on those areas with the highest risks, fostering proactive defense measures. These scenarios enhance incident response planning, facilitating the development of effective strategies, role definitions, and containment and recovery procedures. Well-understood threat scenarios unite different teams across your enterprise, and you can rally around them to promote a continuous improvement culture through regular employee training.

“The consequences of cyberattacks on manufacturing operations can be far-reaching and detrimental for operations, productivity and safety.”

Step-by-Step Guidance for Using Threat Scenarios to Improve Your Cybersecurity Program

Step 1: Choose Threat Scenarios: Select three to four threat scenarios that resonate most with your sub-sector and environment. These will be the focal points of your cybersecurity strategy.

Dragos recommends starting with these four common scenarios for manufacturing environments:

- Ransomware: Ransomware attacks are a significant concern, with their initial access stemming from various sources such as remote connections or leveraging information technologies/operational technologies (IT/OT) dependencies. These attacks involve exfiltrating information, encrypting files, and locking compromised computing systems, demanding ransom payments for their release.

- Trusted Vendor Compromise: Trusted vendors may unwittingly become conduits for cyberattacks when their software becomes compromised before distribution. These attacks can disrupt the supply chain.

- Shared IT/OT Dependencies: OT systems’ reliance on IT systems or insecure remote access into OT environments can result in IT compromises affecting OT, potentially causing disruptions.

- PIPEDREAM: PIPEDREAM is a highly scalable industrial malware that targets industrial control systems. While it was detected and analyzed in 2022, it remains a potential threat, underlining the need for preparedness.

Step 2: Identify Crown Jewels: Identify the critical assets within your environment — typically constituting about 25% of your infrastructure — and prioritize their protection.

Step 3: Align Around the SANS Five Critical Controls: Dragos and the SANS Institute undertook extensive research to discern the most effective measures to counter incidents within Industrial Control System (ICS) environments. These efforts resulted in the formulation of the SANS Five Critical Controls, a concise framework that outlines essential steps manufacturers must take to establish a robust security strategy against genuine threats.

“Threat scenarios simplify the process of risk assessment by identifying and prioritizing vulnerabilities that hold the utmost relevance.”

The SANS Five Critical Controls include:

- Incident Response: To effectively address cybersecurity incidents, it is imperative to envision and plan for the worst-case scenarios. What does a “bad day” look like, and how should your security program respond to such scenarios? Focus on scenarios that hold real relevance to your specific industry and environment, avoiding theoretical exercises in favor of real-life, industry-specific threats. Get a thorough understanding of the risks involved by meticulously examining each scenario from inception to resolution. Select three to four scenarios, like the ones listed above, and reverse-engineer strategies for handling them effectively.

- Defensible Architecture: A well-designed and segmented architecture forms the bedrock of a defensible cybersecurity strategy. It should empower human defenders to thwart human adversaries effectively. Consider whether your architecture can support the collection of critical data needed for incident response. While IT predominantly deals with data and systems, OT encompasses systems of systems and physics. Failing to account for the transient nature of data in OT can be detrimental during investigations and incident recovery.

- Visibility and Monitoring: Achieving comprehensive visibility across your network is indispensable. It involves monitoring control system protocols and communications within your processes, reinforcing the foundation of a defensible architecture. Operational resilience hinges on the ability to conduct root cause analysis, enabling the detection of threats and understanding the scenarios most likely to impact your environment. This should align with your organization’s unique priorities.

- Secure Remote Access: Secure remote access demands multifactor authentication and meticulous supply chain management. Interconnectedness exposes your risk to the risks of others, emphasizing the need for a robust approach to remote access.

- Vulnerability Management: Effective vulnerability management is not about indiscriminate patching but focuses on the vital 2-4% of vulnerabilities that truly matter. Identifying these vulnerabilities and knowing how to address them is essential.

In concert, these five critical controls constitute the foundation of a potent cybersecurity program and give you something to measure against.

Step 4: Conduct a Risk Assessment: Assess the current state of your environment to understand existing vulnerabilities and potential risks.

Step 5: Identify Gaps and Priorities: Based on your risk assessment, identify gaps in your cybersecurity defenses and establish priorities for mitigating them. This step forms the basis for your cybersecurity roadmap.

The Bottom Line: Adopt a Vigilant – But Practical – Risk Management Strategy

The advent of smart manufacturing, driven by AI and advanced technologies, necessitates a paradigm shift in how manufacturers approach cybersecurity. It must be an integral and proactive component of your digital transformation journey. By leveraging threat scenarios and adopting a vigilant but practical stance toward risk management, manufacturers can safeguard their operations, protect sensitive data, and position themselves for success in an evolving landscape where innovation and security must go hand in hand. M

About the Author:

Michael Sakmar is the Vice President of Professional Services at Dragos, Inc., where he leads teams of consultants in performing active defense inside of ICS/OT environments. He is responsible for a range of services such as architecture assessments, penetration testing, tabletop exercises, and incident response.

Welcome New Members of the MLC February 2024

Introducing the latest new members to the Manufacturing Leadership Council

![]()

Kelley Brna

VP, Operations

Merck & Co., Inc.

![]()

merck.com/

![]()

https://www.linkedin.com/in/kelley-brna-22037334/

Bryan Van Itallie

President

Pratt Intermodal Chassis

prattchassis.com/

![]()

https://www.linkedin.com/in/vanitallie/

Technologies for the Factory of the Future

To future-proof manufacturing, drive profits and serve customers, organizations must examine supply chains, sustainability, digital transformation and more

![]()

TAKEAWAYS:

● The foundation for manufacturing’s future is data and organizations’ ability to effectively capture and use data in every factory element.

● Manufacturers need to think beyond operations when they apply Manufacturing 4.0 so that they also evolve their supply chains and sustainability efforts.

● AI/ML and virtual tools can have big effects that can be amplified with collaboration, optimization and continuous improvement.

Globally, manufacturers are experiencing growing pressure to reduce carbon emissions in their production processes. The manufacturing industry is characterized by disruptions and volatility, supply chain problems, upcoming inflation, and increased financial costs, making it paramount that manufacturers find innovative solutions to face the challenges ahead.

Sustainability issues and digital transformation have become the main drivers for the next three to five years and that will shape the future of the manufacturing industry towards 2030. These trends drive the necessity of true innovation further. Even though there has been plenty of focus on buzzwords like Industry 5.0 and similar, this is now becoming a reality. The path forward is clear: manufacturers must engender greater resilience and future readiness by optimizing resource usage, minimizing waste, and embracing renewable energy sources. However, the difficulty lies in simultaneously ensuring profitable operations.

Embrace the Future of Manufacturing Through Data

A key component in all the trends and challenges is data, like reliable data on environmental sustainability, traceability throughout the value chain and product life cycle, and real-time data to detect supply chain disruptions.

For manufacturing companies, emerging technologies help expand the opportunities to become a data-driven factory of the future. Using low-cost sensors and IoT, gathering data throughout the manufacturing process is now possible. With advanced AI and machine learning algorithms, organizations can enable predictive maintenance of expensive manufacturing machinery and reduce costs and downtime. Digital twins can enable virtual simulation of development, testing, and validation of products, and AR/VR can even let customers try products before they are made.

Implement Resilient Supply Chains

Better visibility of the supply chain can lead to a more flexible manufacturing value network. For example, production can either be moved in-house or outsourced to an alternate location when a disruption occurs without adversely affecting operations.

Four clusters of disruptive digital technologies will enable supply chain digitization.

- Commodity IoT sensors with the ability to capture and process data and connect/exchange data with other systems over communications networks to provide transparency.

- Cloud computing and access to advanced algorithms enable organizations to derive insight, model, analyze and make accurate predictions to provide flexibility and efficiency.

- Technologies like robotics, business process management and robotic process automation, and voice assistants and chatbots enable the automation of physical and non-physical processes, leading to faster and more efficient processing.

- Combining disparate IT and OT data sources into a single system to generate digital operational insights and business KPIs at an enterprise level.

“Manufacturers must engender greater resilience and future readiness by optimizing resource usage, minimizing waste, and embracing renewable energy sources”

Achieve More Sustainable Manufacturing Practices

Reducing waste production is an important step in achieving more sustainable manufacturing practices. Currently, approximately 300 million tons of plastic waste is produced every year. By implementing a waste reduction program, designing products for sustainability, implementing lean manufacturing principles, using technology to optimize processes, product lifecycle management, e-waste management, and partnering with suppliers, manufacturers can reduce waste, conserve resources, and minimize their environmental impact. This helps meet the growing demand from eco-conscious consumers for sustainable products and benefits the bottom line of manufacturers.

Five Steps to Becoming A Future-Proof Manufacturer

A future-proof strategy for manufacturing sustainability will therefore demand internal systems that measure sustainability impacts that are commonplace to count today and those that are likely to be tomorrow. What raw materials are being used? How much fresh water is the process consuming? How much energy is being used in the process, and what are the primary energy sources? Soon we will likely see tools that automatically collect and require all digital data on sustainability indicators for products and services.

1. The Virtual Twin Experience

A virtual twin is a real-time virtual representation of a product, manufacturing or supply chain that can be used to model, visualize, predict and provide feedback on properties and performance. Virtual twin technologies provide an opportunity to reduce operational costs and waste and drive efficiency and innovation across the value chain. A Virtual Twin Experience can help companies develop the digital manufacturing and supply chain of the future.

2. Optimization

Optimization is a mathematical approach for decision-making to get the best outcome under conditions or constraints, like requiring the allocation of scarce or limited resources. A smart, autonomous and integrated optimizer is key to addressing the dynamically evolving challenges like:

- Reducing manufacturing costs and maximizing fulfillment through plant layout, facility and production planning, scheduling and sequencing

- Minimizing transportation costs through efficient flow and storage of goods from point-of-origin to point-of-consumption

- Minimizing labor costs by creating staffing plans to meet demand, while respecting shift preferences, labor regulations, vacations, etc.

“A future-proof strategy for manufacturing sustainability will demand internal systems that measure sustainability impacts that are commonplace today and those that are likely to be tomorrow”

3. Artificial Intelligence (AI) and Machine Learning (ML)

Manufacturers have more data than ever before, which makes AI/ML ripe for disruption. AI/ML is a game changer for manufacturing and supply chain as it has the potential to offer CAPEX-free productivity improvements. Through sophisticated pattern recognition, AI/ML can help enhance processes considered difficult to improve due to their complexity, seemingly unpredictable fluctuations or insufficient objective decision-making capabilities. An end-to-end, fully interconnected, digital and AI/ML ecosystem can deliver exponential and sustainable impact by driving innovation and resilience.

4. Continuous Improvement and Real-time Operations

The enterprise business process is to enable greater visibility and easy access to information for all stakeholders. The data driven platform technology empowers end-to-end transparency and performance management reporting to reassess strategic priorities. At the same time, it facilitates ad hoc, agile problem-solving to identify supply chain issues, perform root-cause analysis and ensure corrective actions are taken on the most important opportunities. KPIs are tracked to ensure improvement, especially in times of uncertainty.

5. Collaboration

A systematic approach is required to effectively and inclusively consider multiple perspectives on decisions and work efficiently with all relevant stakeholders for shared understanding and mutual benefit across the organization. Lean collaborative platform-based solutions enable teams to leverage modern, cloud-native, interactive environments, equipped with lean boards and widgets to digitalize shop floor activities, which allow teams to systematically bring people together and collaborate, facilitate structured problem solving, and nurture better team relationships, ultimately driving synergy, better decision-making and a competitive advantage.

Sample Customer Case Study:

A leading consumer packaged goods and retail (CPGR) manufacturer has implemented a factory of the future plan to deliver innovation faster, cheaper, and smarter, achieving the following:

- Brand integrity with interlocking traceability, including suppliers

- Best practices enforced across evolving supply chain

- New product introductions delivered up to 20% faster

- Cost-of-Goods Sold lowered by up to 27%

- Visibility and control over 30 sites

- Globally coordinating new product introduction (NPI)

Benefits of Technologies for the Factory of the Future

- Increase flexibility to respond to long-term or fundamental changes in the supply chain and market environment by adjusting the configuration.

- Bring in agility to efficiently change operating states as a response to environmental uncertainty or volatile market conditions.

Enable collaboration to work efficiently with other entities for mutual benefit across the organization. - Reduce redundancy with strategic and selective use of spare capacity and inventory that can be invoked to cope with a crisis, such as demand surges or supply changes.

Conclusion

Manufacturing and operations are complex, and today’s hyper-connected, fast-evolving markets only add to the challenge. To address a global economy in an advanced digital age and sustainability requirements, manufacturers must have the visibility and control to satisfy customers who are demanding more than products and services — they want individualized, emotional experiences that they can “own.” M

About the author:

Prashanth Mysore is Senior Director: Global Strategic Business Development at Dassault Systèmes

Survey: Smart Factories Are Still a Work in Progress

Manufacturers are moving ahead with creating smarter factories as they grapple with cultural resistance and integrating new technologies.

![]()

TAKEAWAYS:

● A majority of manufacturers say their investments in M4.0 technologies to create smart factories will continue unchanged this year.

● Most manufacturers are at an intermediate stage with M4.0 adoption.

● The most significant roadblock to implementing a smart factory strategy is an organizational structure or culture that resists change.

Tracking the evolution of factories and plants to become so-called smart facilities is a bit like trying to discern the movement of a glacier. You can watch intently but it is hard to detect change. And when change does occur, it is measured in inches. But like a glacier, over time the movement to smart factories and plants will encompass all a production facility does and in a profound way.

The manufacturing industry is inexorably marching toward a day when smart factories and plants, powered by intelligent, sensor-based networks that generate vast volumes of data that are analyzed by artificial intelligence systems, will operate with less human intervention. Highly automated, increasingly intelligent and flexible, the smart factory of the future beckons.

As we head toward that promised land, we look for markers along the way, indications that may tell us where we are making progress and where the obstacles to that progress may lie. The Manufacturing Leadership Council’s new Smart Factories and Digital Production survey sheds light on those markers.

Section 1: STATUS OF DIGITAL INVESTMENT AND ADOPTION

At the highest level, the industry’s posture with regards to investing in Manufacturing 4.0 technologies to create smart factories appears to be on solid footing. In the new survey, nearly 69% of respondents indicated that their M4.0 investments this year would continue unchanged from last year. Nearly 19% said they would increase investments and only 10% said their investments would decline (Chart 1). Concerns about a recession have evidently eased.

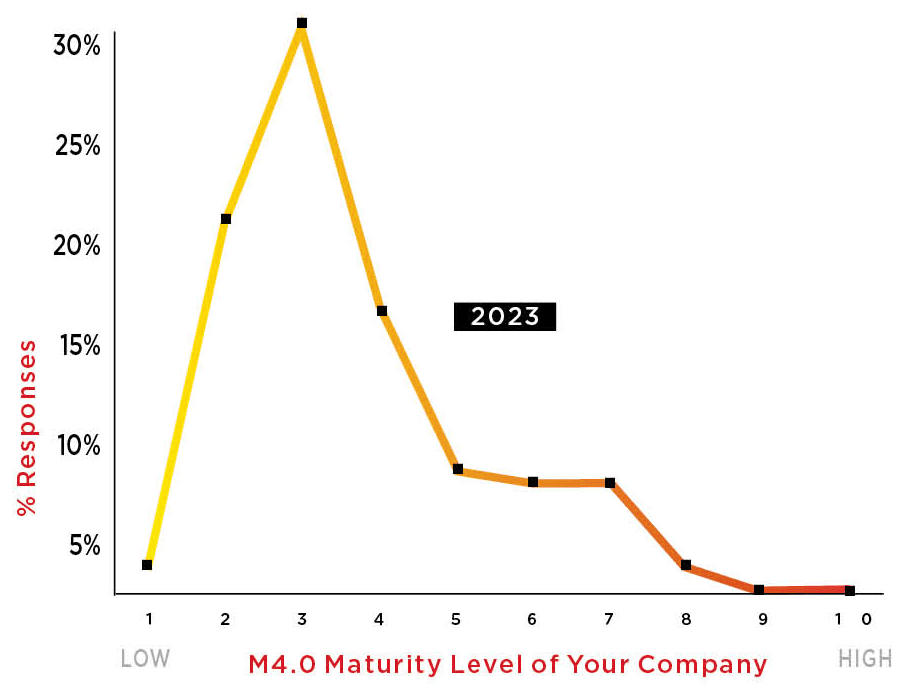

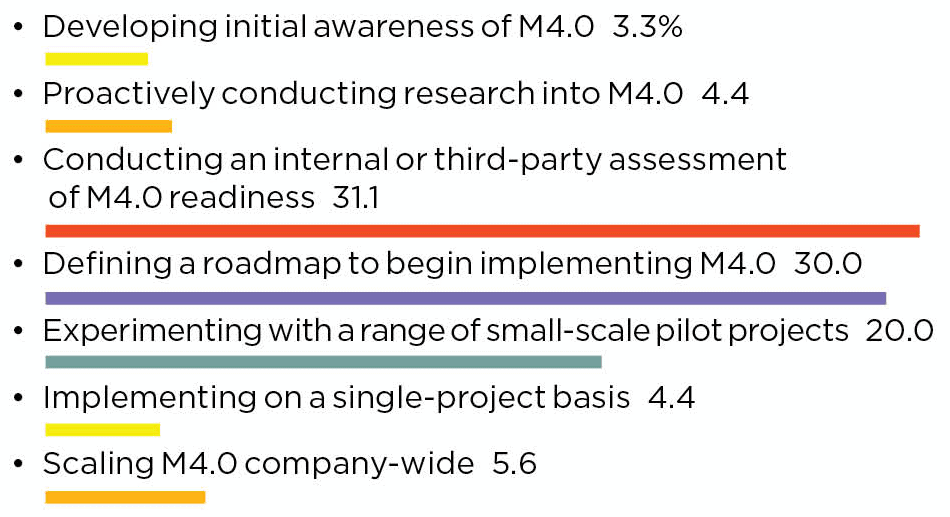

As manufacturers continue to invest in digitalization, they have moved from the initial stages of developing awareness and conducting research into M4.0 to action. Thirty percent of the respondents to the survey say they implementing small-scale pilots, experimenting with a range of projects, or scaling M4.0 companywide. Interestingly, about 31% report they are at the stage of conducting M4.0 readiness assessments, which, when completed, should spawn many pilots and projects (Chart 3).

“The manufacturing industry is inexorably moving toward a day when smart factories and plants …will operate with less human intervention.”

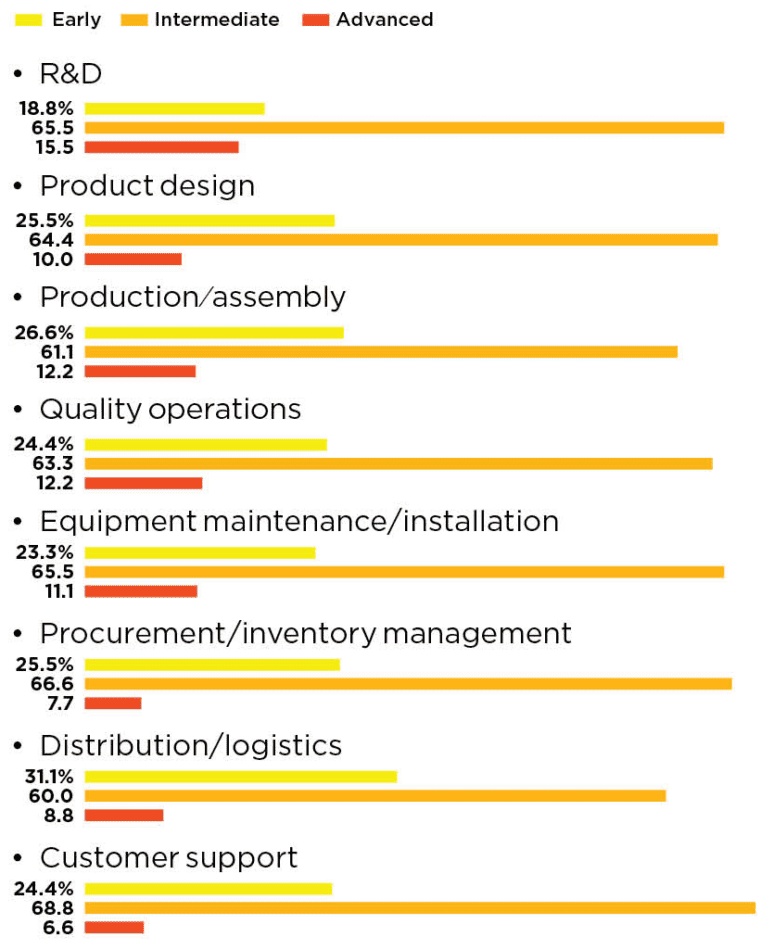

When looked at the stage of adoption functionally – in R&D, product design, and in production and assembly, for example – a strong majority of respondents say they are at an “intermediate stage” with M4.0. Those at an “advanced” stage represent only single-digit or low double-digit constituencies (Chart 4).

Overall, when respondents were asked to assess the digital maturity level of their manufacturing operations, about 58% said that, on a scale of one to 10, they are in the three to five range, which supports the view that the industry has moved beyond the initial stages of M4.0 and is approaching an early majority of those embracing the digital model (Chart 2).

1. Economy Notwithstanding, Strong Majority Sees No Change to M4.0 Investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2024?

2. Nearly Half Are in Early Stage of Digital Maturity

Q: How would you assess the digital maturity level of your manufacturing operations?

3. Readiness Assessments, Roadmaps Dominate Stage of M4.0 Efforts

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today?

4. Functionally, Most Firms Are in the Middle Stage of Digital Adoption

Q: At what stage of digital adoption are the following functions in your company?

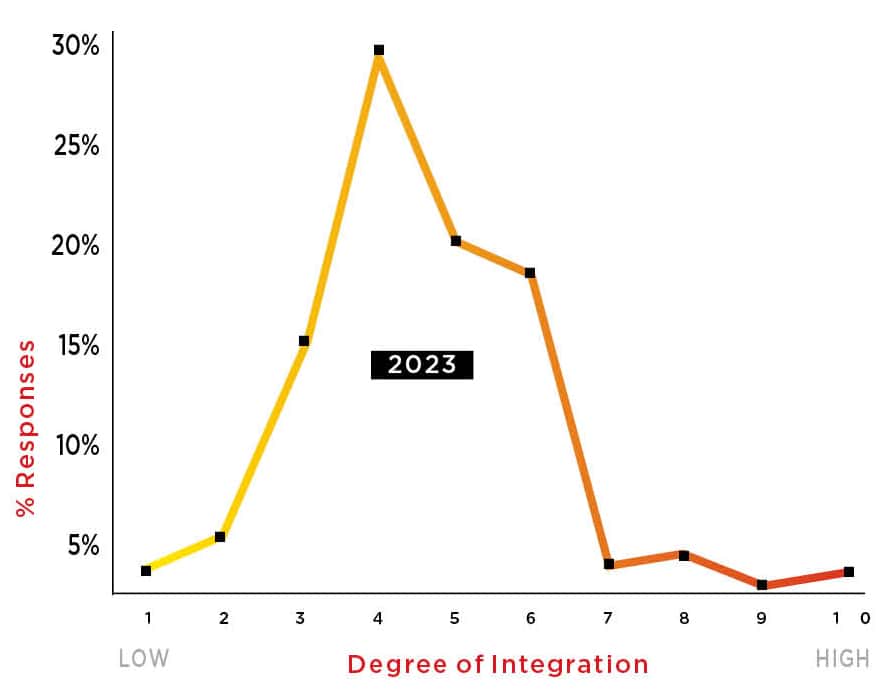

5. Few Have Fully Integrated Smart Factory Strategies With Business Strategies

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy?

Section 2: MEASURING DIGITIZATION

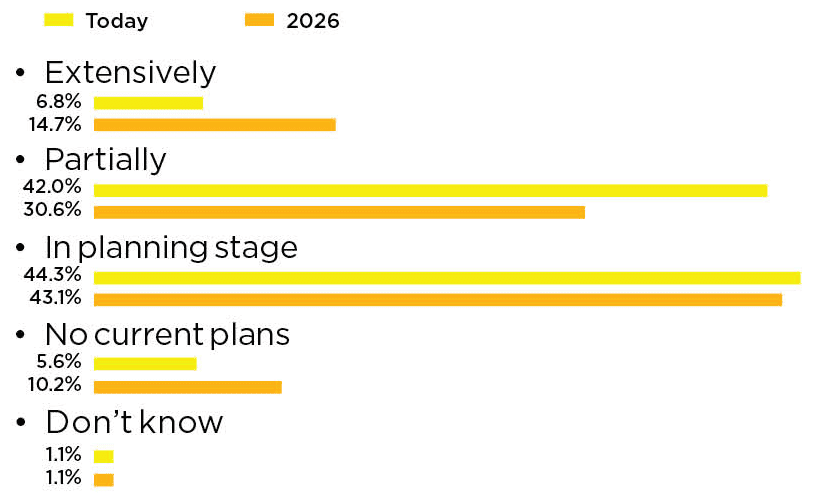

Not surprisingly, only a fraction of manufacturers, 6.8%, report that they have “extensively” digitized their factory operations today. Most have either partially digitized or are in the planning stages of doing so. But when asked to anticipate the extent of digitization by 2026, 14.7% said they expect to be extensively digitized on an end-to-end basis in that timeframe (Chart 6).

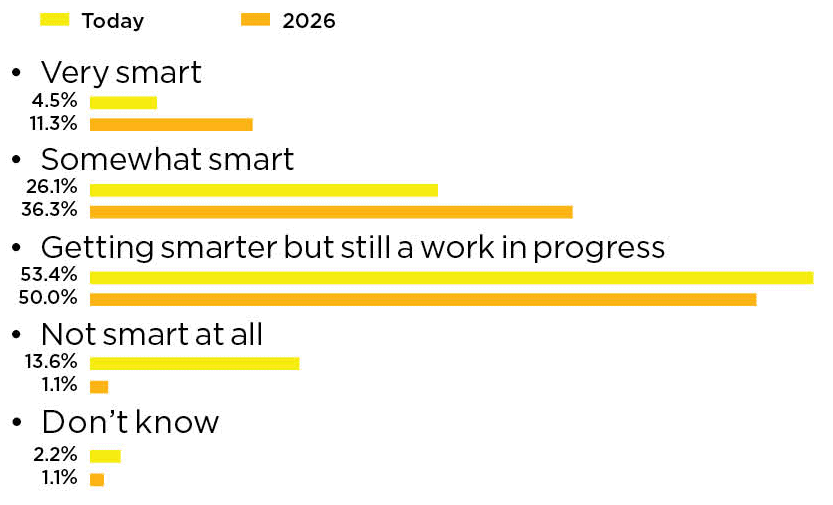

Correspondingly, only a fraction of respondents, 4.5%, would be ready to say their factories are “very smart” today, but, once again, aspirations are high. By 2026, 11.3% expect to be able to affix that label to their operations. But for the moment, a majority of respondents, 53.4%, say their factories and plants are getting smarter but are still a work in progress (Chart 7).

6. More Fully Digitized Operations on the Horizon

Q: To what extent are your factory operations fully digitized end to end today, and what do you anticipate they will be by 2026?

7. “Smart” Factories Still a Work in Progress

Q: How “smart” do you consider your factory and plant operations to be today?

Section 3: FACTORY ORGANIZATION AND MANAGEMENT

So where is all this digital work heading? What do manufacturers expect their factory models to look like in the years ahead?

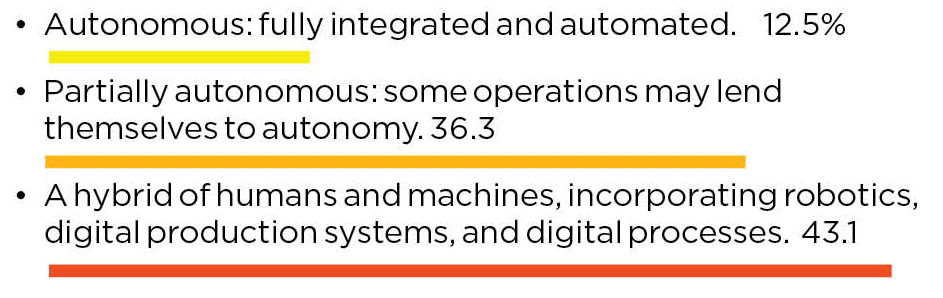

The idea and prospect of some level of autonomous operation is clearly on radar screens. Nearly half of the respondents, 48.8%, expect their future factory models to be autonomous, defined as fully integrated and automated, or partially autonomous, defined as some operations or processes conducted autonomously (Chart 8).

8. Autonomous Operations is on the Radar Screen

Q: What is the expected future state of your factory model?

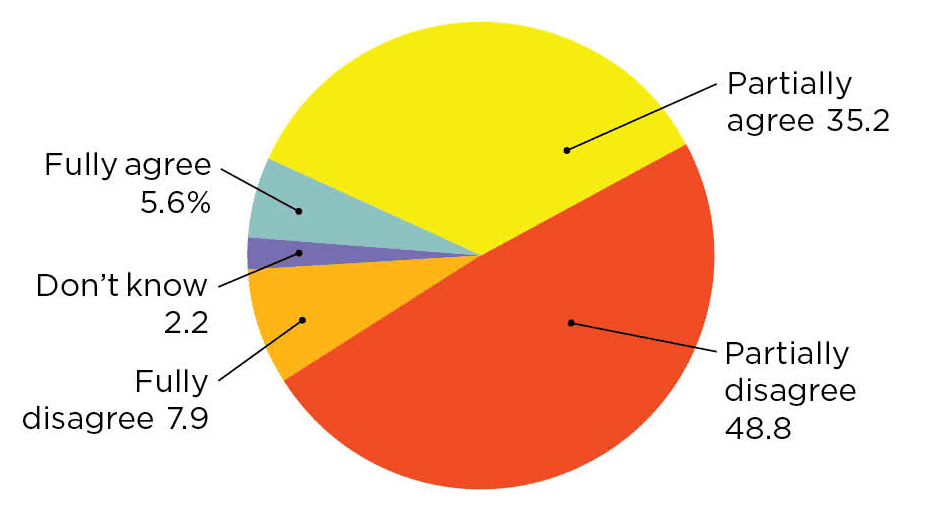

9. A Majority Does Not See Self-Learning Factories in the Future

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.”

Section 4: TECHNOLOGY USAGE

There is an expanding basket of advanced technologies manufacturers will be using to create their smart factories and plants.

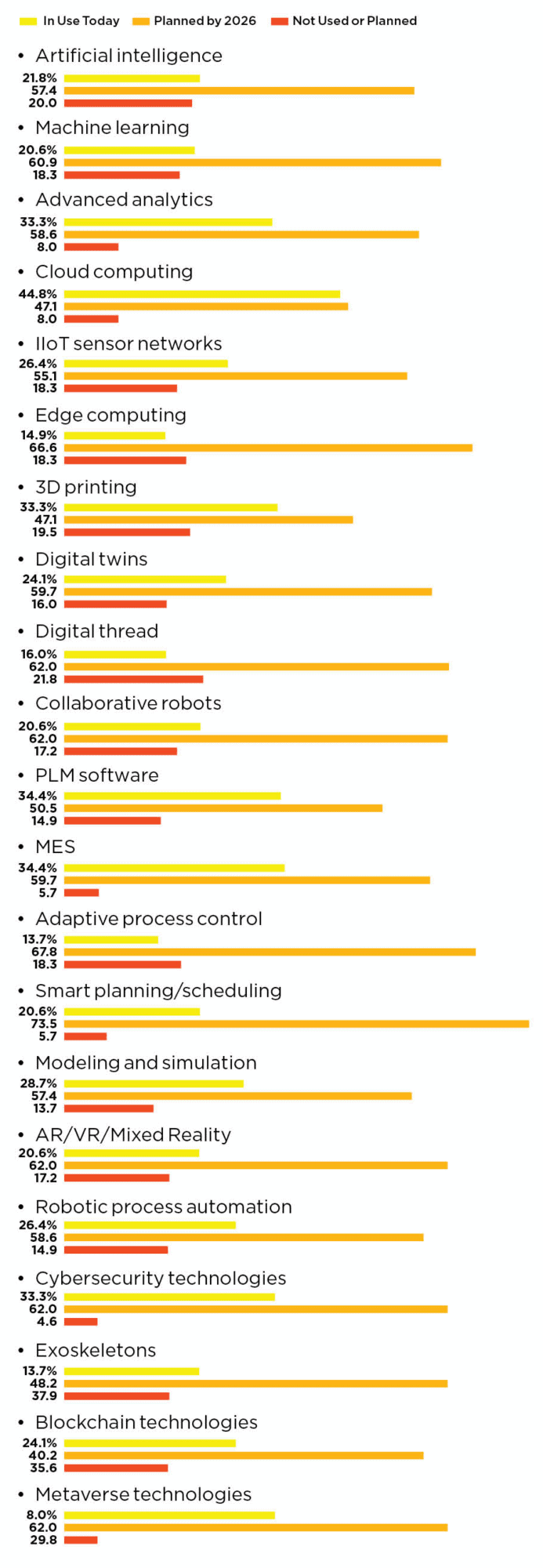

When asked about adoption status on 21 technologies, the most striking thing was how strong planned adoption was by 2026. Eight of the technologies surveyed – for example, machine learning, edge computing, digital threads, AR/VR, and Metaverse technologies – all received 60% or higher planned adoption responses. Eight others garnered 50% or higher responses (Chart 10).

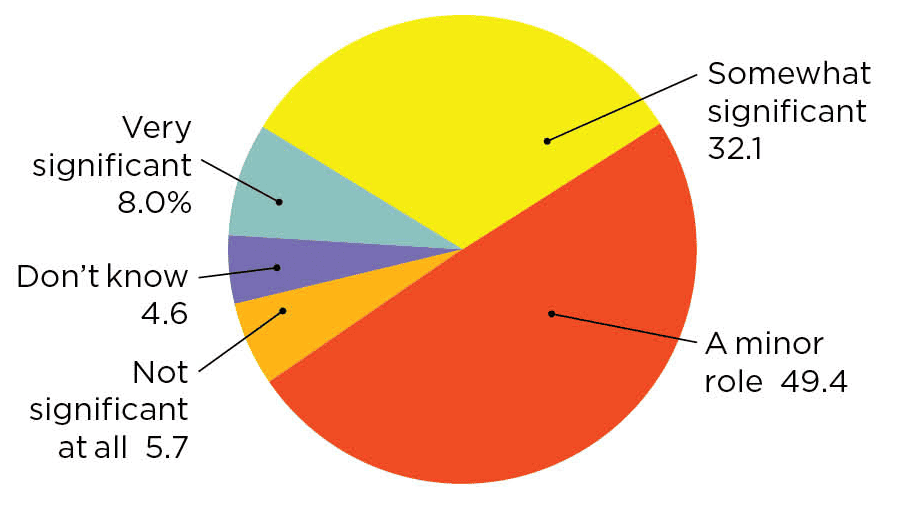

Interestingly, there is a split within the respondent base as to how significant an impact AI will have in operations, perhaps reflecting the still early stage of usage in many companies. Only 40% say that AI will be either very significant or somewhat significant, while nearly half, 49.4%, see AI as playing a minor role in the next few years (Chart 11)..

While it may be obvious that it takes a multitude of technologies to create a smart factory, the underlying message is that real power of being smart will only be realized when these technologies are integrated within the factory. That’s a whole new level of work ahead for manufacturers.

10. Strong Aspirations for a Basket of Technologies by 2026

Q: Where does your company stand in regard to the following technologies in its production operations?

11. Views on AI Significance Diverge

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations?

Section 5: M4.0 OPPORTUNITIES AND CHALLENGES

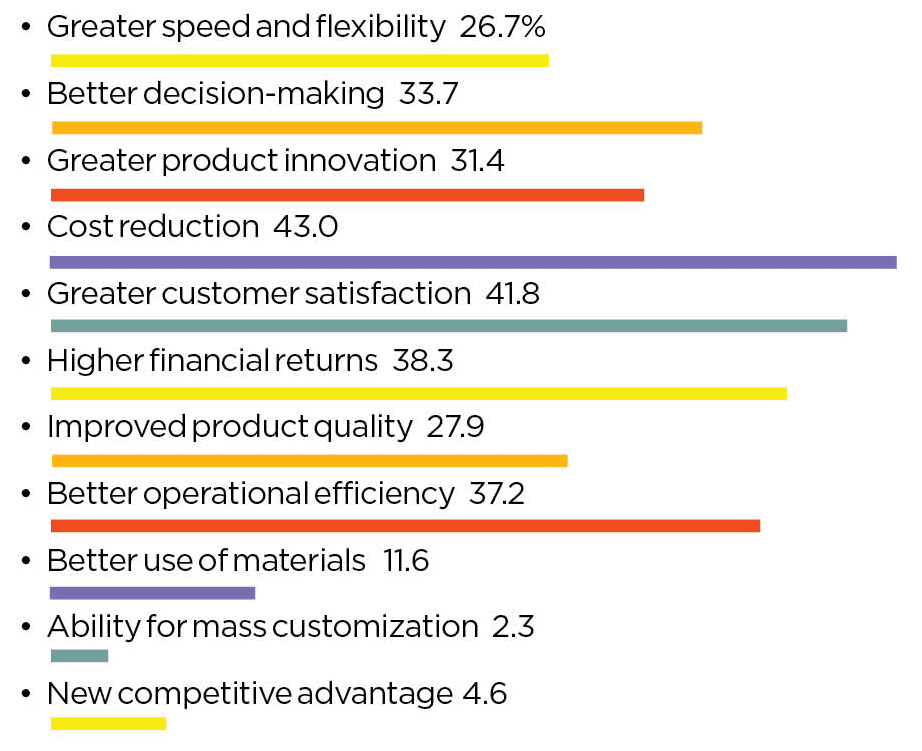

Manufacturers also expect a basketful of benefits from creating smart factories and plants. Although there is no breakout factor, cost reduction, greater customer satisfaction, and higher financial returns top the list of expected benefits.

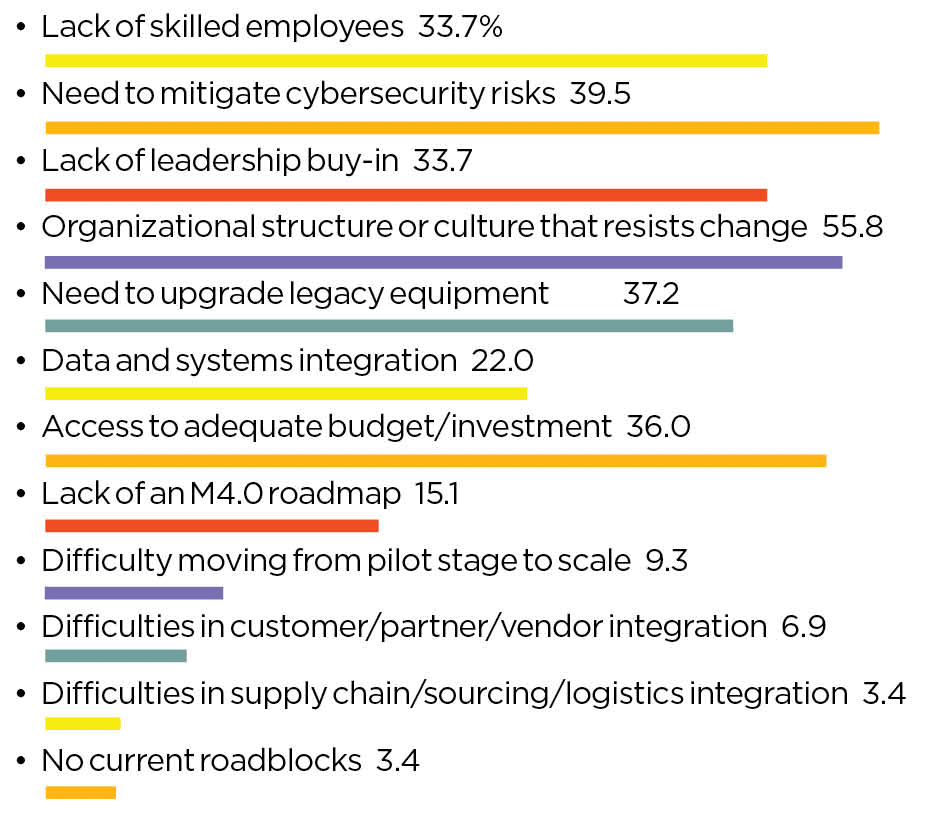

But when it comes to roadblocks in implementing a smart factory strategy, there is clearly a breakthrough factor – organizational structure or culture that resists change. More than 55% of respondents cited this factor as the primary issue in realizing their smart factory vision, considerably higher than a lack of skilled employees, cybersecurity issues, or the need to upgrade legacy equipment (Chart 12).

This may be why, when asked how well their smart factory strategies have been integrated with their company’s business strategy, very few respondents indicated that these two things were fully integrated (Chart 5).

As the famed management consultant Peter Drucker once said: “Culture eats strategy for breakfast.”

Is that glacier moving? M

12. Culture is Biggest Roadblock to Smart Factories

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top 3)

13. Cost Reduction, Customer Satisfaction Chief Desired Benefits

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top 3)

About the author:

David R. Brousell is Founder, Vice President, and Executive Director at the NAM’s Manufacturing Leadership Council.