SURVEY: Manufacturers Go All-In on AI

A growing number of manufacturing organizations have brought AI to the shop floor, and as usage grows, so do aspirations for its future impact, a new MLC survey reveals.

![]()

There were two open-ended questions at the close of the Manufacturing Leadership Council’s 2023 Transformative Technologies survey. The first: Which single technology is currently having the most impact on your manufacturing operations?

Of the 171 respondents to this year’s survey, 19 cited AI or machine learning, the most commonly mentioned response, with four of those mentioning generative AI specifically. Not far behind were manufacturing execution systems, with 13 responses. Rounding out the pack were automation and data analytics with about 10 responses each. Honorable mentions went to cobots, vision systems and ERPs. Some respondents elaborated on the power of system consolidation and broader data access.

Far more consensus was seen, however, on the second open-ended question: What technology do you believe will have the most future impact on your manufacturing operations? For this question, 79 respondents mentioned AI or machine learning (or their cousin, predictive analytics), with robotics and digital twins also receiving multiple, if far fewer, mentions.

This tracks with the 40% of respondents who said they have adopted AI widely or at least on a pilot basis, with another 53% saying they were either researching use cases of developing a plan for implementation.

The MLC has been closely following the AI groundswell in manufacturing, with more use cases continuing to emerge. Most are currently using it for process improvement or predictive maintenance, and many plan to broaden its use in their supply chain, distribution, and sustainability efforts.

Read more below on the results of this survey:

Part 1: Strategy and Organization

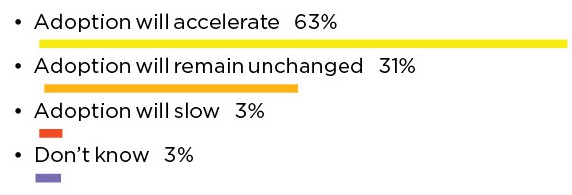

While almost 90% of respondents to last year’s Transformative Technologies survey said they expected M4.0 technology adoption to increase, this year’s response shows a more measured approach to investment – possibly due to economic headwinds faced by many manufacturers.

1. Do you expect your company’s rate of M4.0 technology adoption to increase or decrease over the next two years? (Check one)

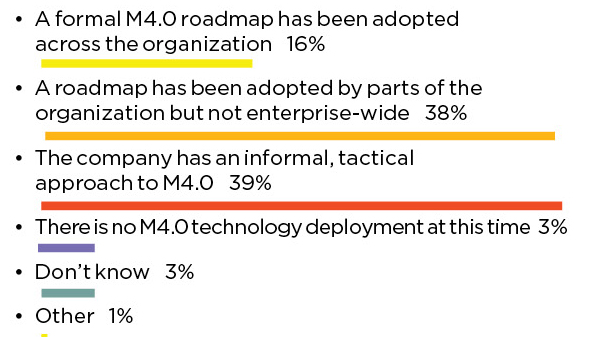

Many companies continue to take a fragmented approach to M4.0 – just 16% say they have an organization-wide technology roadmap. Far more either only have partial strategies or an informal approach to M4.0 deployment.

2. Which statement best describes the current status of your company’s M4.0 technology roadmap or strategy? (Check one)

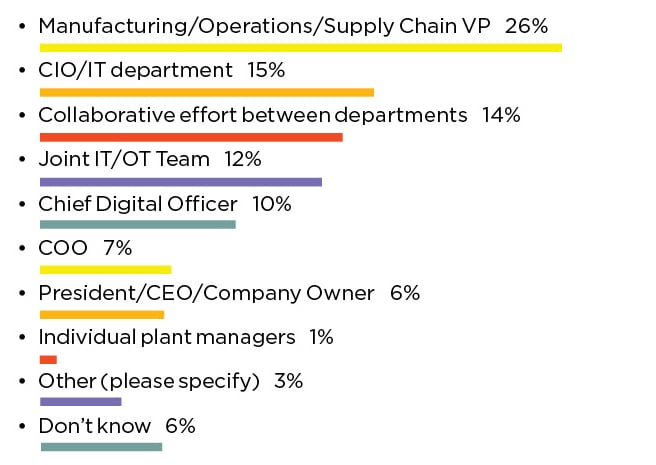

The person in charge of M4.0 strategy is most frequently an operational VP, followed by the CIO/IT department or a collaborative effort between teams.

3. Who is responsible for leading and implementing your M4.0 strategy? (Check one)

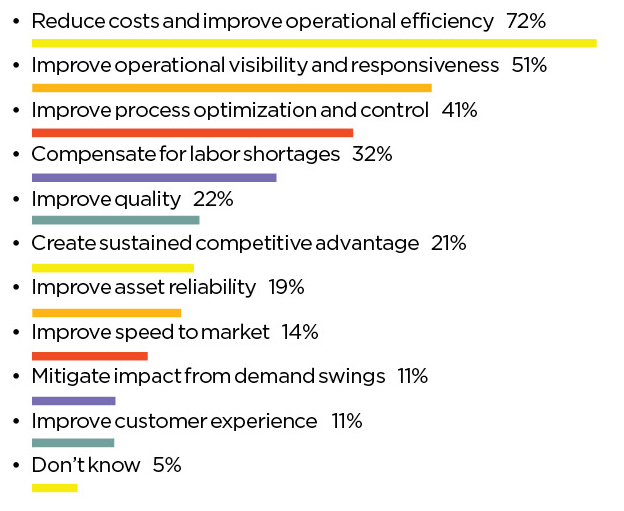

At the end of the day, the bottom line rules – most respondents said that reducing costs and improving efficiency were the top reason for investing in M4.0.

4. What are the most important reasons your company invests in transformative M4.0 technologies? (Check top 3 reasons)

Part 2: Technology Investment Plans

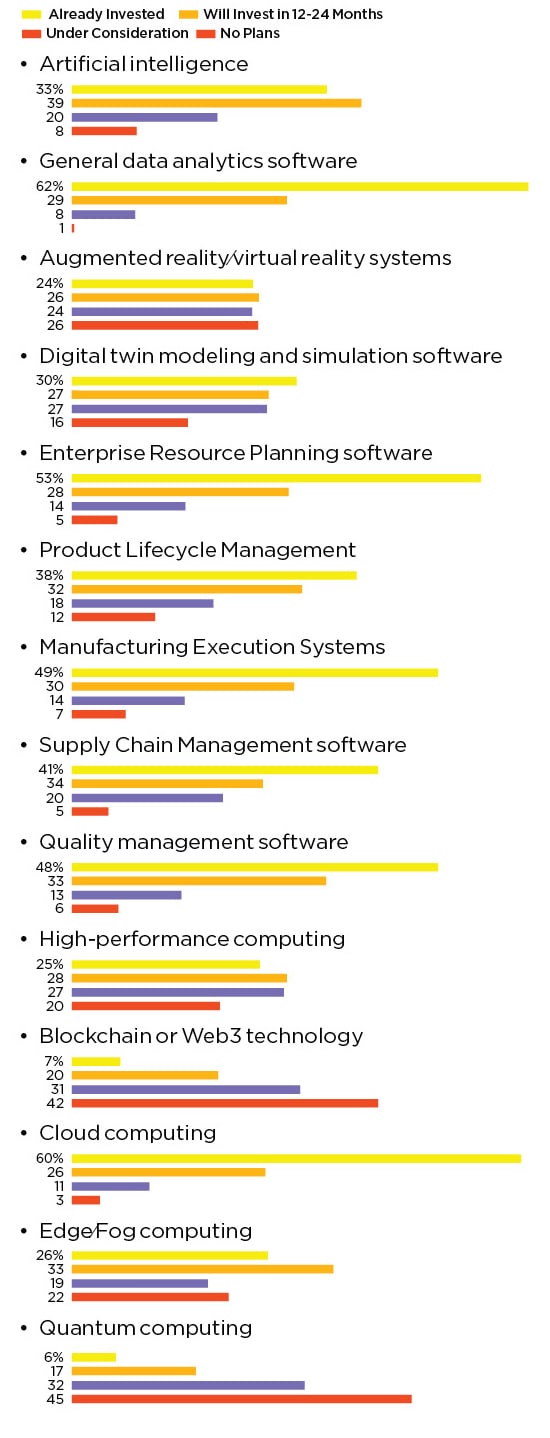

Presently, the most common OT/IT investments are data analytics software, cloud computing, ERP planning software, and MES. Strongest near-term plans (12-24 months) are in AI and supply chain management software followed by edge computing and product lifecycle management. Additionally, about a third are considering digital twins and quantum computing for longer-range plans.

5. What are your company’s investment plans for the following OT/IT-related technologies? (Check one in each column)

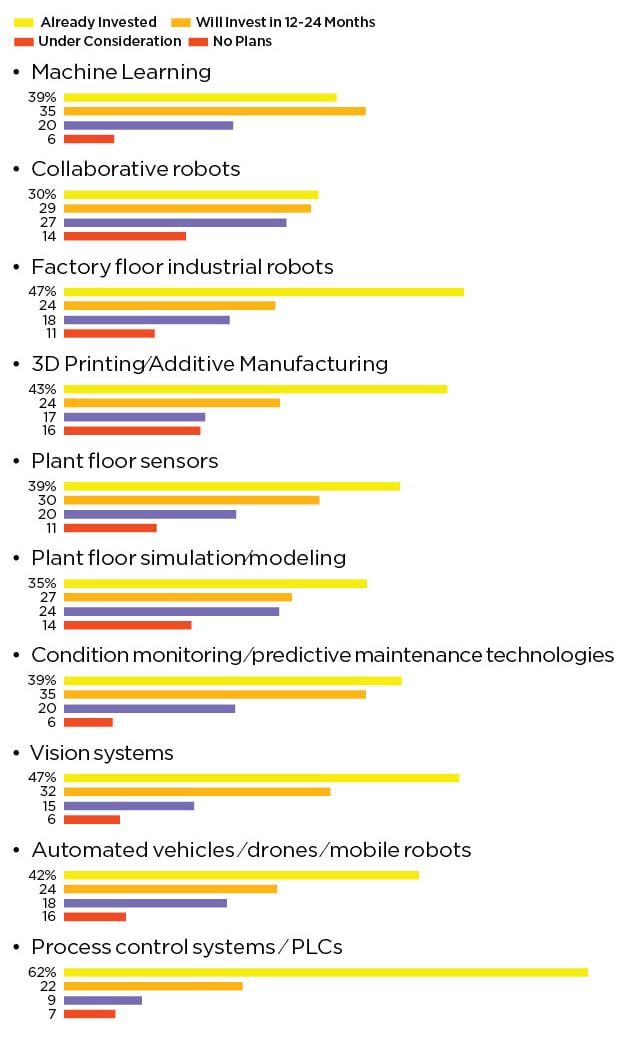

For production technologies, process control systems are in the lead for current investments while nearly half say they have industrial robotics and/or vision systems in place. Other popular technologies are additive manufacturing and AGVs or mobile robots. In the near-term manufacturers indicate plans to implement machine learning and condition monitoring technologies.

6. What are your company’s investment plans for the following production technologies? (select one)

Part 3: Adoption of AI and Machine Learning

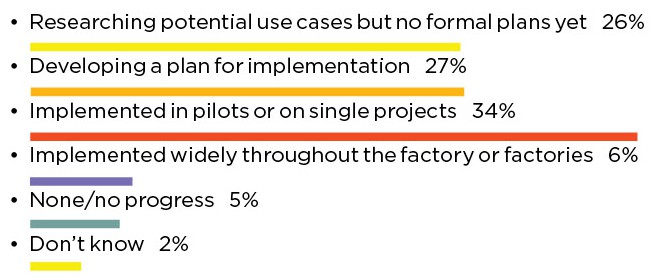

Drilling specifically into AI, over a third of respondents said they had implemented AI in pilots or on a single project (34%), with almost as many saying they were developing a plan for implementation (27%), a slight uptick compared to last year’s responses on AI usage. Very few say they have implemented it widely (6%), while even fewer said they had made no progress toward adopting AI (5%).

7. Where does your company stand today in adopting AI in manufacturing operations? (Check one)

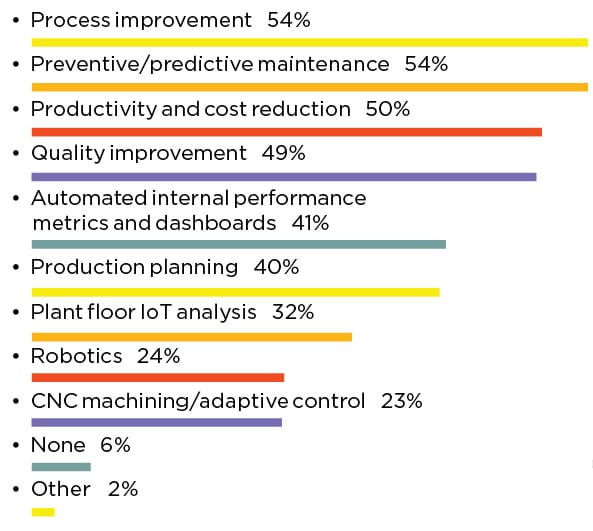

The current key applications for AI usage are process improvement, preventive/predictive maintenance, productivity/cost reduction, and quality improvement.

8. What are the key application areas for AI and Machine Learning technologies in your manufacturing operations? (Check all that apply)

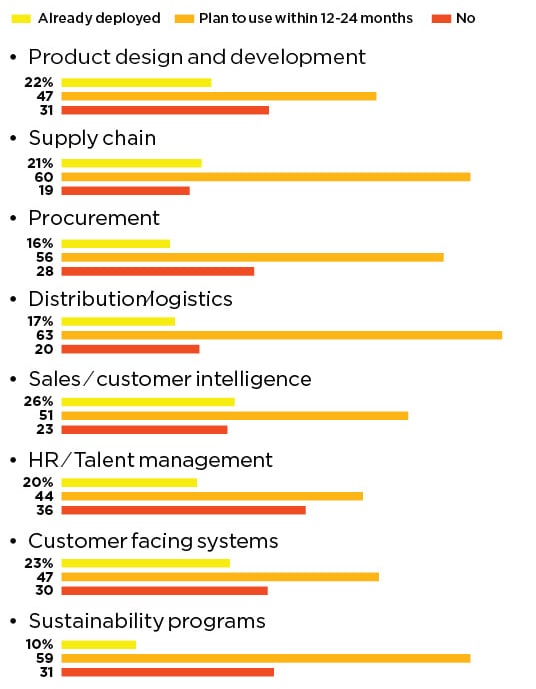

Outside of manufacturing operations, respondents say the greatest number of current AI use cases are in sales and customer intelligence followed by product design and development. Within the near term, manufacturers expect to broaden its use within distribution and logistics, supply chain, sustainability, and procurement.

9. In what other areas of the organization are you deploying AI and Machine Learning, or planning to deploy over the next two years? (Check one option for each area)

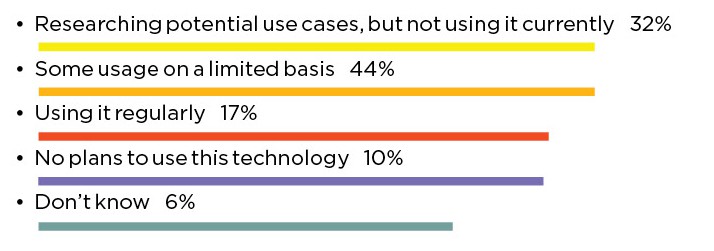

Asked specifically about generative AI technologies like ChatGPT or Bard, 44% indicated they are using it on a limited basis and 17% said they are using it regularly. 10% say they have no plans to use it at all.

10. What is your organization’s position on using generative AI like ChatGPT or Bard? (Check one)

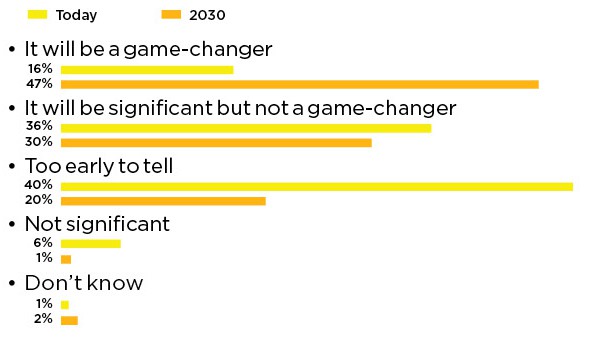

Views on the impact of AI in manufacturing show that while many already see it as significant (36%), nearly half of respondents felt it will be a game-changer by the year 2030 (47%).

11. Overall, what is your current assessment of the potential of AI and Machine Learning, both today and by 2030? (Check one in each column)

Part 4: Impacts and Challenges of Transformative Technologies

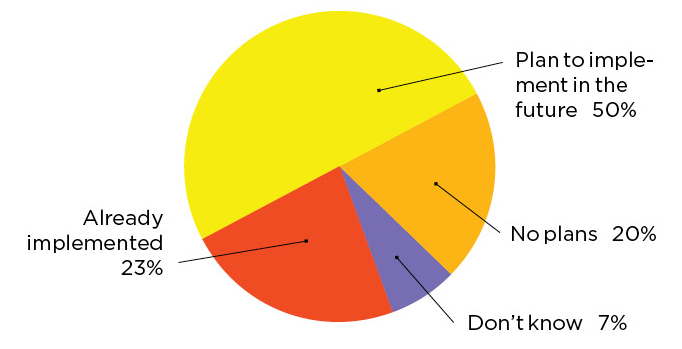

When it comes to sharing data across functions of the enterprise, the digital thread is coming –only 23% of manufacturers have one currently, but 50% say they have plans to implement it in the future.

12. Has your company implemented a digital thread to share data generated by one or more of the M4.0 technologies you have adopted across multiple functions? (Check one)

The trend toward workplace flexibility, likely emerging out of necessity during the pandemic, hasn’t fully abated – 63% say they have invested in technology meant to allow for remote operations.

13. Has your company made technology investments with an eye toward allowing greater workforce flexibility (i.e. remote operations)?

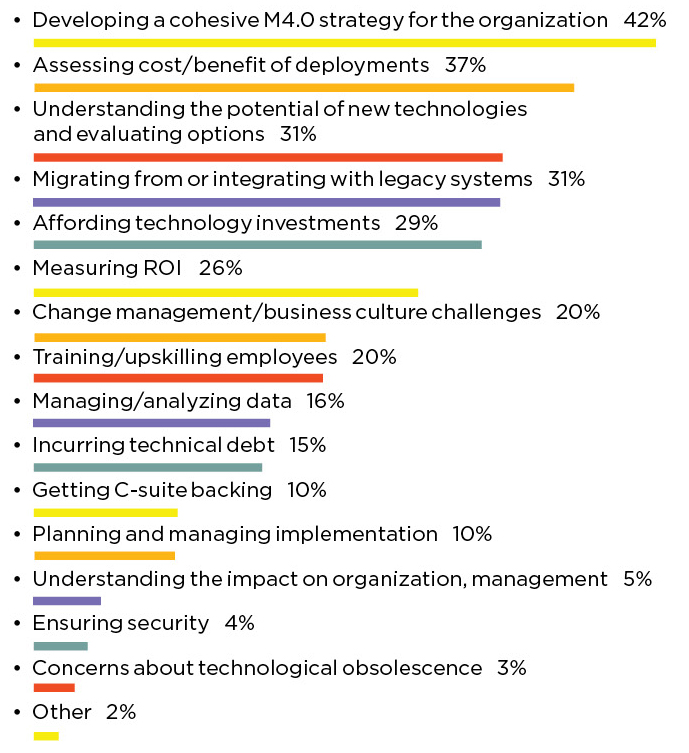

When asked what their most pressing challenges were related to M4.0 adoption, the top responses were developing a cohesive strategy (42%), assessing the cost and benefit of deployments (37%), understanding and evaluating new technologies (31%), and migrating from or integrating with legacy systems (31%). M

14. What are your top three challenges related to adopting and using M4.0 technologies? (Select top three)

About the author:

Penelope Brown is Senior Content Director for the Manufacturing Leadership Council.

Survey development was led by the MLC editorial team with input from the MLC’s Board of Governors.

The Industrial Metaverse May Be Closer Than You Think

Nearly 80% of manufacturing executives seem confident that the metaverse will transform aspects of manufacturing in the next five years, a new Deloitte/MLC study reveals.

![]()

TAKEAWAYS:

● Executives say that the Industrial Metaverse offers new ways to solve a variety of pressing challenges they face in the near term.

● Attracting and retaining top talent and building resilience and visibility in supply chains are top goals.

● Among the chief challenges with the Industrial Metaverse are cybersecurity, data protection and IP, brand, and safeguarding personal information.

In May 2023, Deloitte and the Manufacturing Leadership Council (MLC) embarked on a study to better understand the industrial metaverse and its applications in manufacturing. This article presents some of the key highlights from the resulting publication “Exploring the industrial metaverse” (referred to as “the study” in this article), including findings that the majority of manufacturers surveyed are already progressing on their industrial metaverse journey and are deriving benefits from even partial adoption.

A Paradigm Shift

The industrial metaverse is the convergence of individual technologies that, when used in combination, can create an immersive three-dimensional virtual or virtual/physical industrial environment. As technology evolves, the industrial metaverse will likely allow access to these immersive 3D environments from any internet-connected device, including virtual reality (VR) and augmented reality (AR) devices, as well as smartphones, tablets, laptops, and equipment, from anywhere in the world.

A majority of manufacturing executives surveyed[1] are bullish on the potential of the industrial metaverse in the near term. More than 70% of surveyed executives believe that in the next five years it will have a high rate of adoption in the manufacturing industry. Nearly 80% are confident that the metaverse will transform R&D, design, and innovation and enable new product strategies.[i]

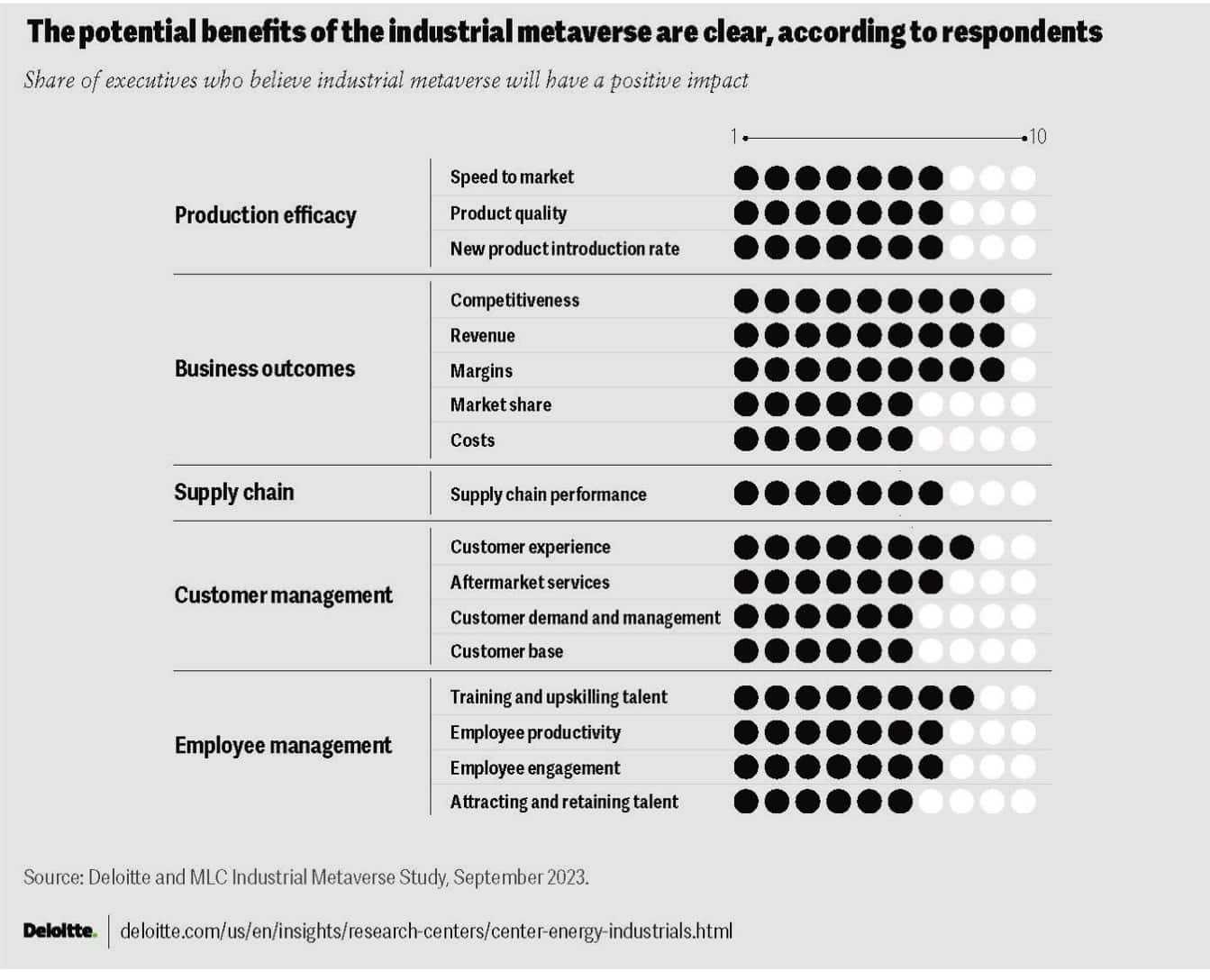

Surveyed executives generally agreed that the industrial metaverse offers new ways to solve a variety of pressing challenges they face in the near term, such as attracting and retaining top talent, and building visibility and resilience into their supply chains (figure 1). They tend to view the industrial metaverse as a pathway to future value realization through improved new product introduction rates and new customer experiences and services. Respondents also expect a broad positive impact across the business and are confident that the industrial metaverse will improve key business outcomes such as competitiveness, market share, revenue, and costs, among others.

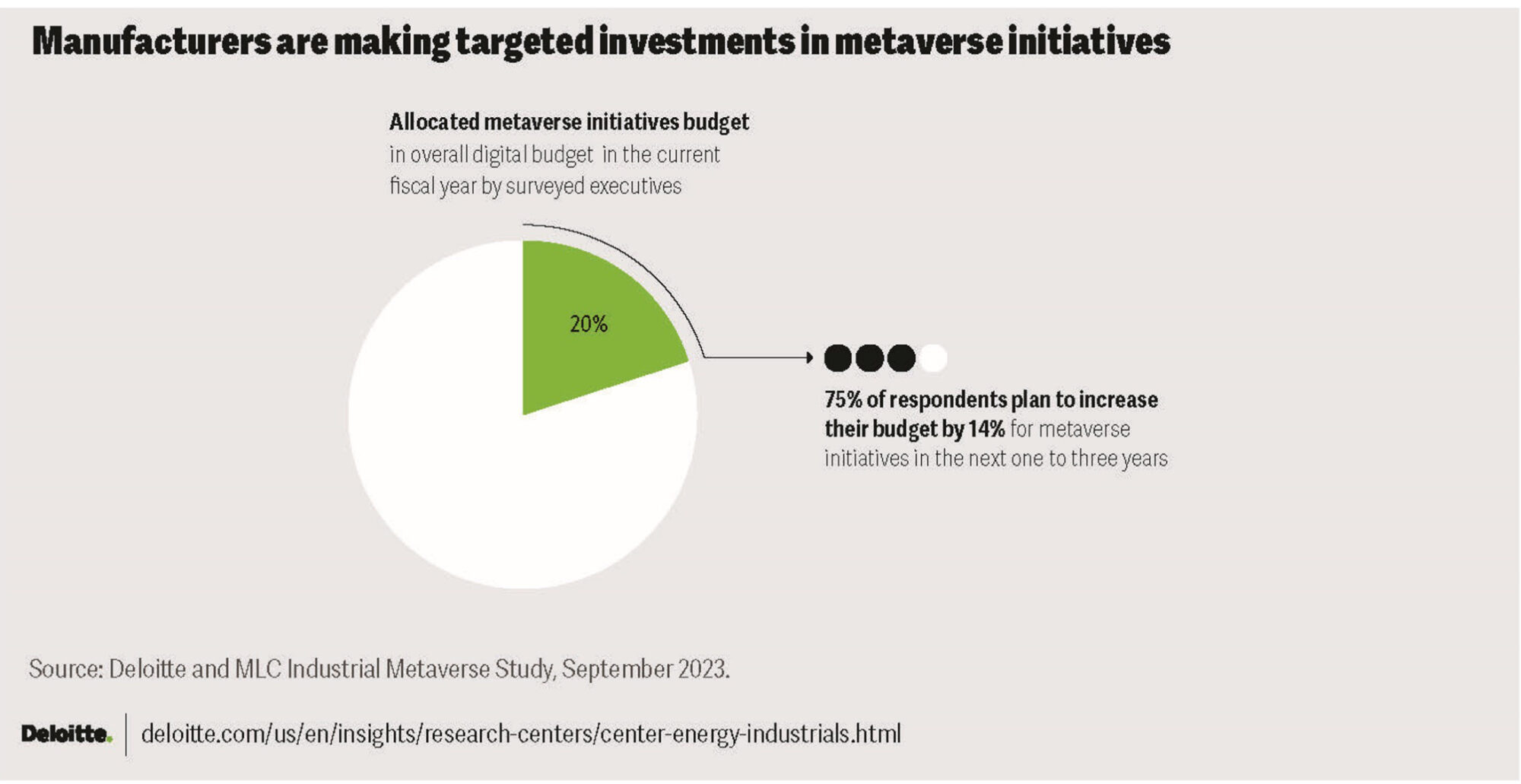

However, the study results indicate that manufacturers aren’t just betting on the future, they seem to be building it. Some respondents shared that they have already made significant investments in metaverse initiatives, and nearly three quarters plan to increase their investments over the next 1–3 years (figure 2).

Building on Smart Factory Momentum

Through digital transformation, smart factory solutions have generally allowed companies to collect important data from their processes, products, assets, and operators and perform advanced analyses to generate valuable insights, and then augment human intelligence with machine intelligence to implement significant and sustainable improvements. These advancements have resulted in greater asset efficiency, enhanced product quality, reduced costs, and increased safety and sustainability.[ii]

In a previous Deloitte paper that focused on how manufacturers can derive value from smart factory technologies,[iii] four primary ecosystems were introduced: production (quality sensing, factory asset intelligence, product development, etc.), supply chain (supply network mapping, digital warehousing, control towers, etc.), customer (aftermarket services, virtual product experiences, etc.), and talent (recruiting, training, etc.).[iv] Within the production ecosystem, a set of eight use cases were introduced, aptly named the “Great 8,” as the most prevalent use cases for smart factory technologies that manufacturers are operationalizing. Because of the scope of what the industrial metaverse can offer—connection to data-rich, immersive 3D environments from anywhere there is a broadband internet connection—its potential value stretches far beyond just the production ecosystem and the Great 8 use cases.

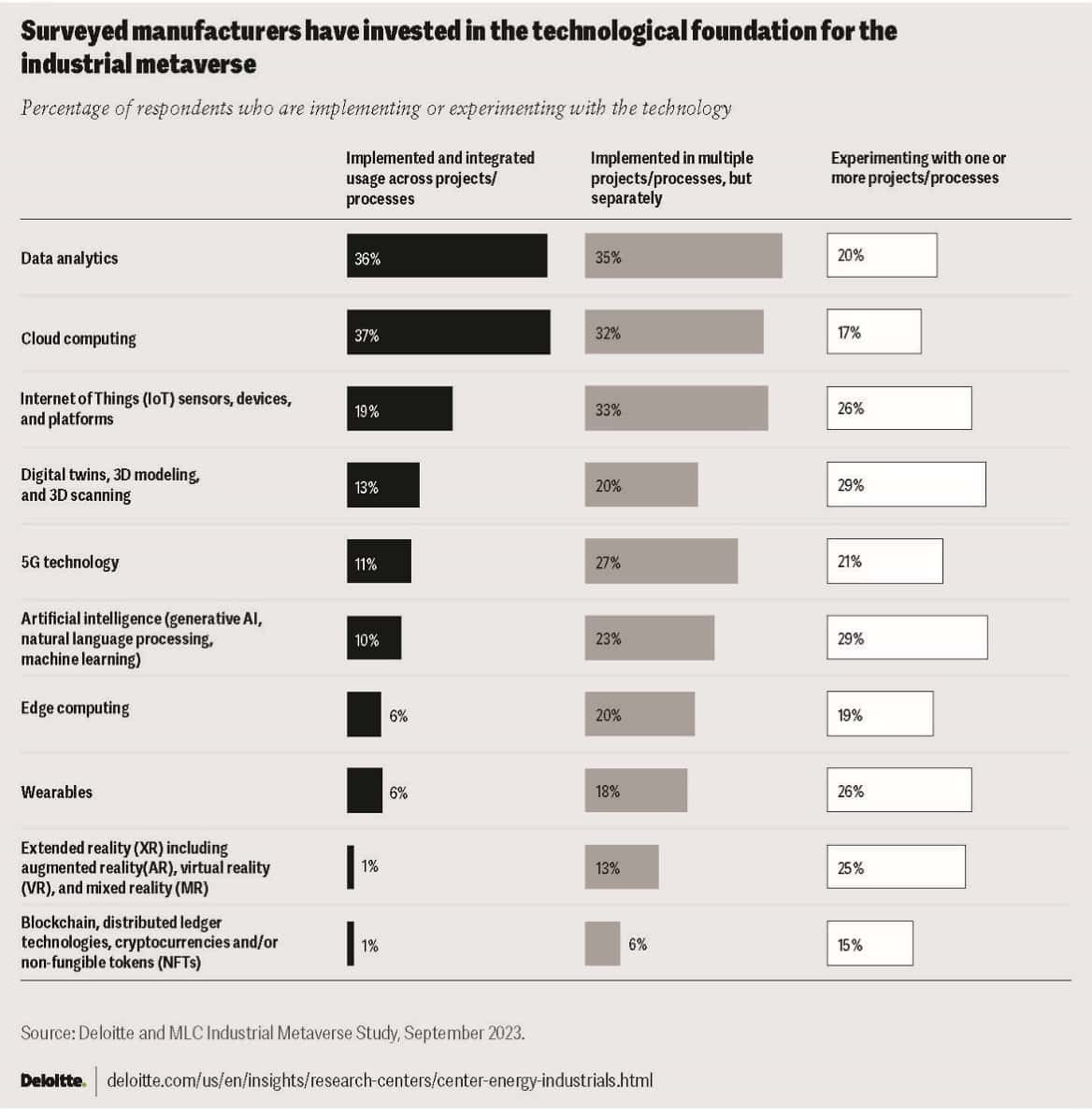

The manufacturing industry appears well-positioned for the adoption of the industrial metaverse. Given their continued focus on digital transformation and their journey toward the smart factory, the majority of companies surveyed have made significant investments and are already using the foundational technologies that power the industrial metaverse. Companies are generally either implementing technologies like data analytics, cloud computing, AI, 5G, and Internet of Things technologies across multiple projects and processes, or they are currently experimenting with one-off projects (figure 3). The same is true for digital twins, 3D modeling, and 3D scanning, which can all serve as building blocks for the immersive 3D environments of the industrial metaverse.

The study shows that not only do most manufacturers seem to have a strong technology foundation in place, many of the surveyed respondents are already combining and leveraging these technologies today to implement industrial metaverse use cases and create value.

Manufacturers Appear to be Driving Toward Adoption

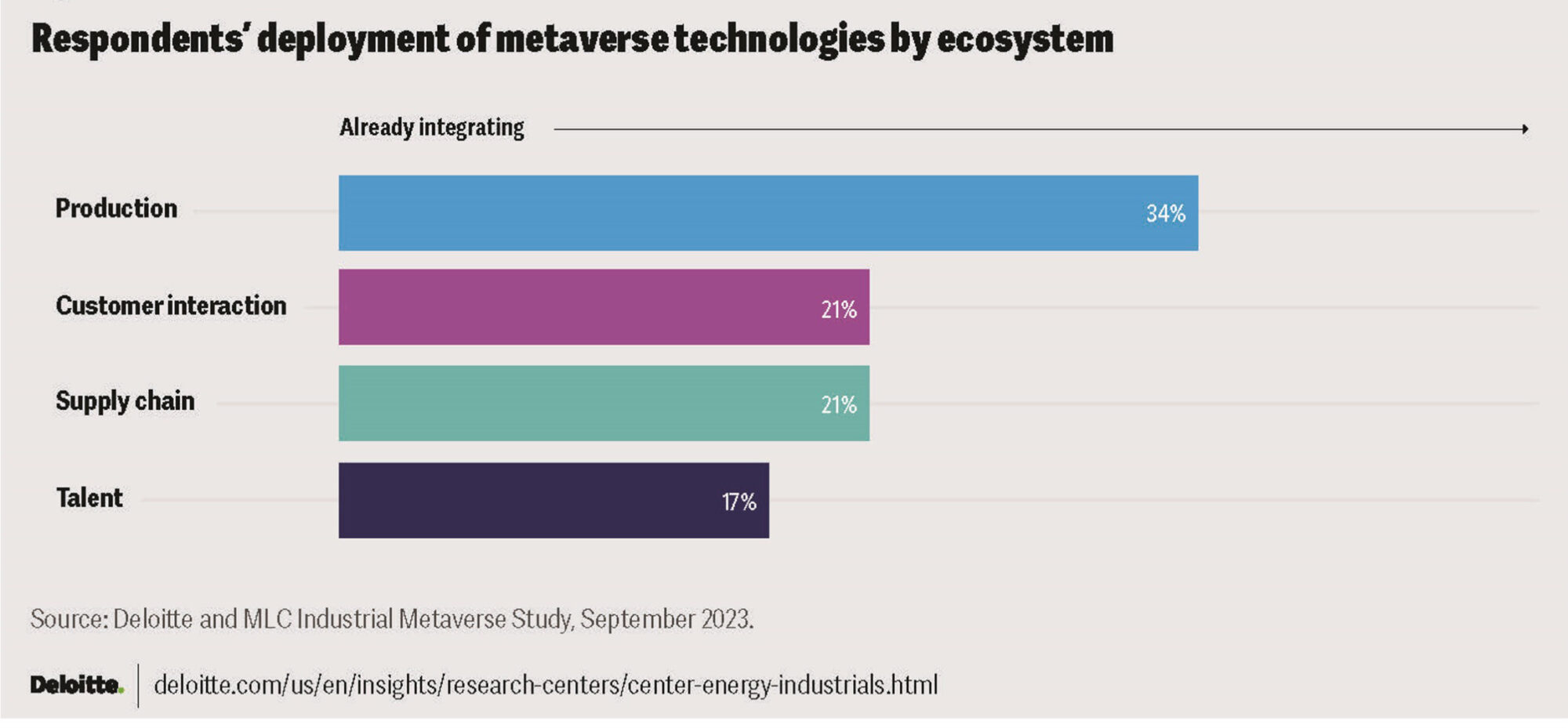

Nearly all (92%) of surveyed executives said that their company is experimenting with or implementing at least one metaverse-related use case and, on average, they are currently running more than six. Building on their smart factory efforts and leveraging the foundational technologies already in place, the production ecosystem was the most common for use case implementation, with more than one-third of respondents already integrating metaverse technologies, followed by the customer, supply chain, and talent ecosystems (figure 4).

Respondents then shared the primary use cases they are implementing using metaverse technologies. The study provides the complete details about these use cases, including their definitions, prevalence of implementation amongst surveyed respondents, the primary benefits derived, and some examples of use cases in action. Process simulation and real-time monitoring/digital twin were the two most common use cases overall, and the remaining production-focused use cases were also prevalent. Immersive training ranked third, followed by supply chain management and immersive customer experiences, demonstrating a healthy distribution of use cases across the talent, supply chain, and customer ecosystems.

The use cases and case examples that companies have reported seem to demonstrate that manufacturers are deriving value today from implementing industrial metaverse initiatives. However, they may still feel that there are challenges and risks to overcome to move toward its full adoption.

Cyber, Data Protection Are Important Risks

Cyberthreats are pervasive and can have a disastrous effect on a company if not properly mitigated. Implementing the industrial metaverse will likely bring new challenges since it derives its unique power from making proprietary 3D data about parts, products, facilities, etc., available to a variety of internal users, customers, and suppliers. It does this by allowing users to access the data through a myriad of interaction technologies over the internet, such as AR/VR devices, tablets, and phones.

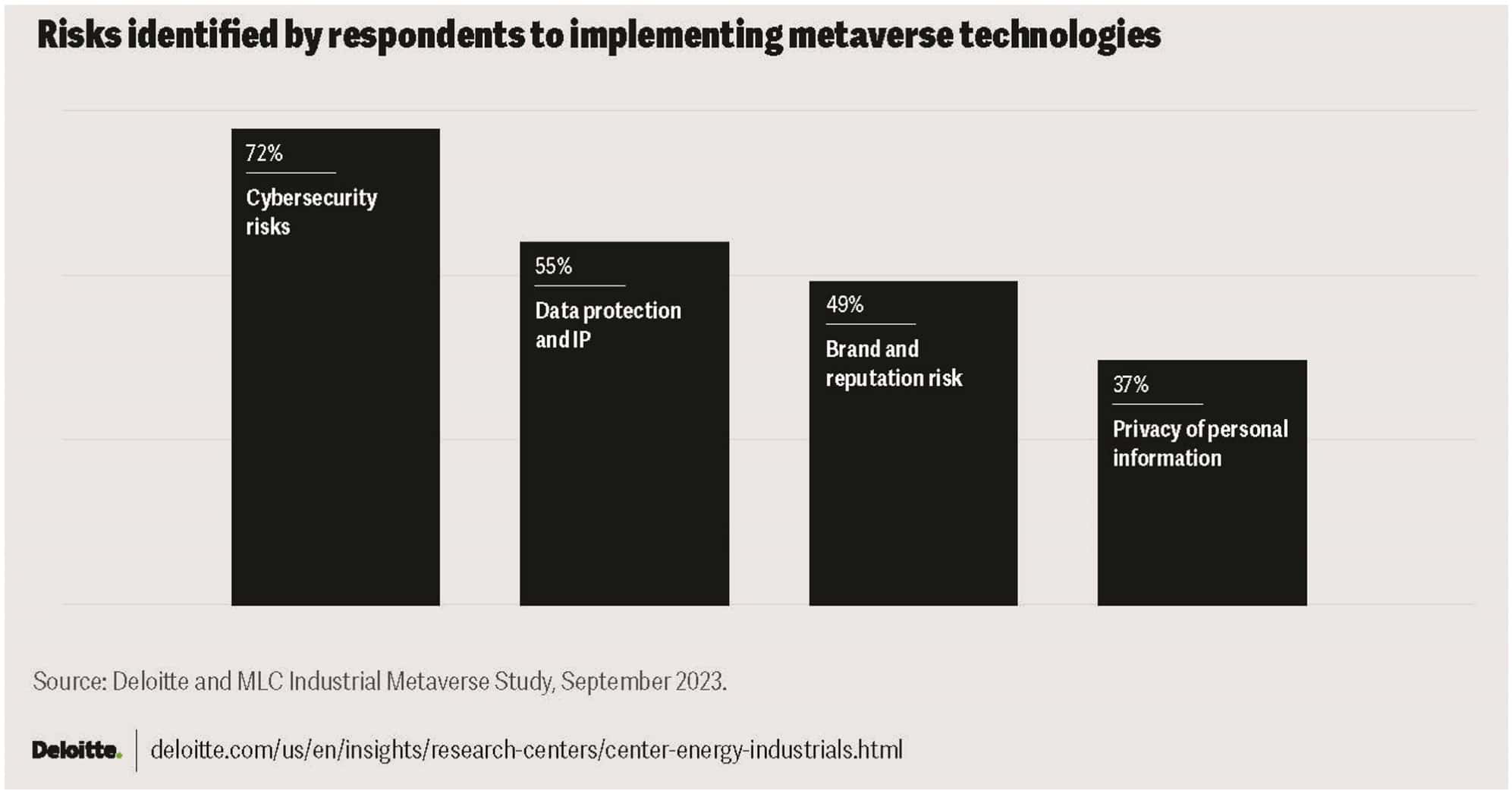

One executive mentioned that because the metaverse will require significant data management; data protection, privacy, and security is a concern.[v] In fact, more than 70% of the respondents agree that cybersecurity is one of the greatest risks associated with implementing metaverse-enabling technologies (figure 5). Rounding out the top four are respondents’ concerns about protecting data and IP, brand, and personal information, all of which can be compromised in a cyberattack.

Digitalization has required manufacturers to drive collaboration between informational technology and operational technology to create an effective cybersecurity approach.[vi] Companies should develop capabilities to identify and address risk in an information technology (IT)–operational technology (OT)–interaction technology (ET) environment. One executive explained that his company is working to establish OT security capabilities and standards for how to review equipment efficiently, following the company’s IT policies, so that the operations and engineering teams can more quickly pilot and implement new equipment. This includes ET, especially since they are typically low cost (<$5,000) and don’t rise to the same level of review priority for IT as, say, a muti-million-dollar software package.[vii]

While cybersecurity risk may increase with the industrial metaverse, the study suggests that manufacturers generally believe the value it will deliver outweighs the risk, especially with the right mitigation strategies in place.

Unleashing the Power of the Industrial Metaverse

The 2023 Deloitte and MLC Industrial Metaverse study indicates that manufacturing executives seem not only confident that the industrial metaverse may hold great promise for the industry – some are already taking what’s next and transforming it into what’s now. In many cases, they are driving forward with metaverse use cases and appear to be deriving significant value across the organization. The study identifies a three-pronged approach that can be used by a broad spectrum of companies to identify, initiate, and scale industrial metaverse initiatives.

About the authors:

Paul Wellener is a Principal within the US Industrial Products & Construction practice with Deloitte Consulting LLP. He has more than three decades of experience in the industrial products and automotive sectors and has focused on helping organizations address major transformations.

John Coykendall is a vice chair, Deloitte LLP, and the leader of the US Industrial Products & Construction practice. John has more than 25 years of consulting experience focusing on global companies with highly-engineered products in the A&D, Industrial Products and Automotive industries.

Kate Hardin, executive director of Deloitte’s Research Center for Energy and Industrials, has worked in the energy industry for 25 years. She leads Deloitte’s research team covering the implications of the energy transition for the industrial, oil, gas, and power sectors.

John Morehouse is the research leader for industrial products manufacturing in the Deloitte Research Center for Energy & Industrials. He has over 25 years of experience in manufacturing-related roles in industry, academia, and government.

David R. Brousell is the founder, vice president and executive director the MLC.

[1] On behalf of Deloitte and the MLC, an independent research company conducted an online survey of over 350 senior executives in the US manufacturing industry in May 2023. The survey findings were supplemented by a series of executive interviews with technology leaders in the industry conducted in June 2023.

[i] Deloitte analysis of the Deloitte and Manufacturing Leadership Council (MLC) Industrial Metaverse survey, 2023.

[ii] Deloitte, “Smart Factory for Smart Manufacturing,” accessed August 18, 2023.

[iii] Paul Wellener et al., Accelerating smart manufacturing, Deloitte Insights, 2020, p. 6.

[iv] Ibid

[v] Insights gleaned from manufacturing executives’ interviews conducted in June 2023.

[vi] Ibid

[vii] Ibid

SURVEY: Choppy Supply Chain Seas Making Skilled Sailors

MLC’s latest survey reveals continued disruptions and challenges but big shifts in digital technology deployments and supply network geography.

![]()

Franklin D. Roosevelt is credited with saying, “A smooth sea never made a skilled sailor.”

As we move another year away from the COVID-19 pandemic that set off a wave of supply chain disruptions, we continue to see how those initial ripples have been amplified and compounded by component and material shortages, inflation and transportation cost increases, worker shortages, military conflict, political tensions, and other complexities that have tested supply chain resiliency.

In the face of these stormy seas, the manufacturing world continues to implement technologies and solutions to help overcome ongoing disruptions while girding supply chains for a more resilient future.

The MLC’s latest Resilient M4.0 Supply Chain survey reveals manufacturing leaders’ expectations and insights related to supply chain challenges, digital technologies, partnerships, and resiliency. It is clear that disruption still abounds, and respondents expect this to continue for at least the next 12-24 months.

At the same time, this year’s survey indicates that supply chains may be less resilient than our 2022 survey found. Nearly 23% of respondents now say their supply chain is not resilient – up from 12% last year. Perhaps, this sentiment is driven by the necessary rapid digital transformation and geographic shift that many supply networks have undergone.

If the supply chain waters remain choppy, manufacturers’ efforts to implement technology, transform their supply networks, and create better partner collaboration will lead to skilled sailors who can navigate future disruptions or calm seas – whenever those arrive.

Part 1: Supply Chain Disruptions

What started with a single cause for disruption is now a mixing bowl of many disruptive factors that continue to cause issues for manufacturers. Supply chain disruptions that were initially rooted in the COVID-19 pandemic have expanded to include the Ukrainian War, tensions with China, and more.

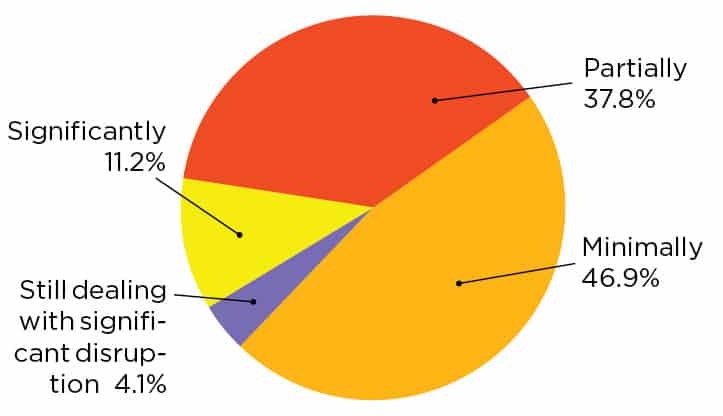

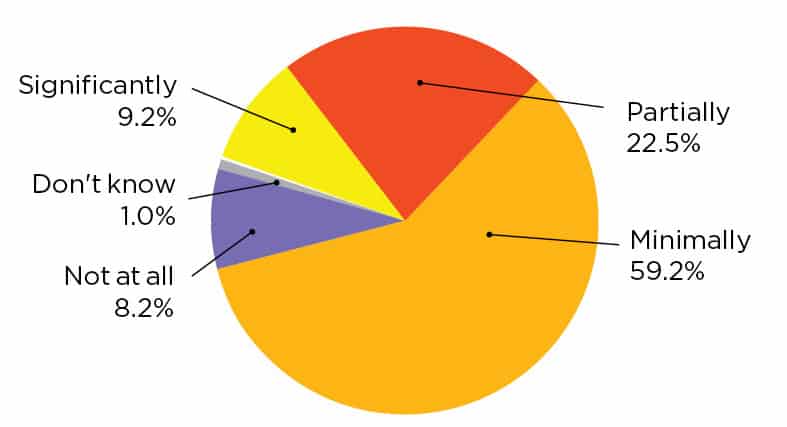

Still, survey respondents report that pandemic-induced disruptions have eased some. About half say they have eased significantly or partially while 47% say they have only eased minimally. [CHART 1] Meanwhile, other high-visibility supply chain disruptions from the Ukraine War and China tensions are not causing significant disruptions at this time, with nearly 67% of respondents reporting minimal or no disruptions from these catalysts. [CHART 2]

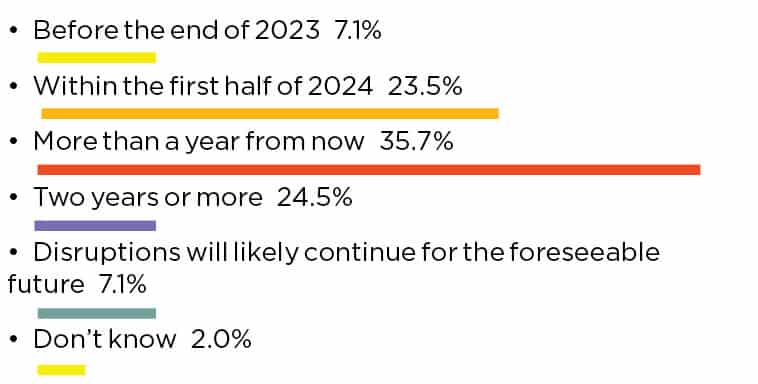

Despite the easing of disruptions from the pandemic and the reported low impact from Ukraine and China, respondents still see supply chain disruptions lingering for some time. In fact, nearly 36% believe disruptions will last for more than a year and nearly a quarter more believe the disruptions could stretch into 2025. [CHART 3]

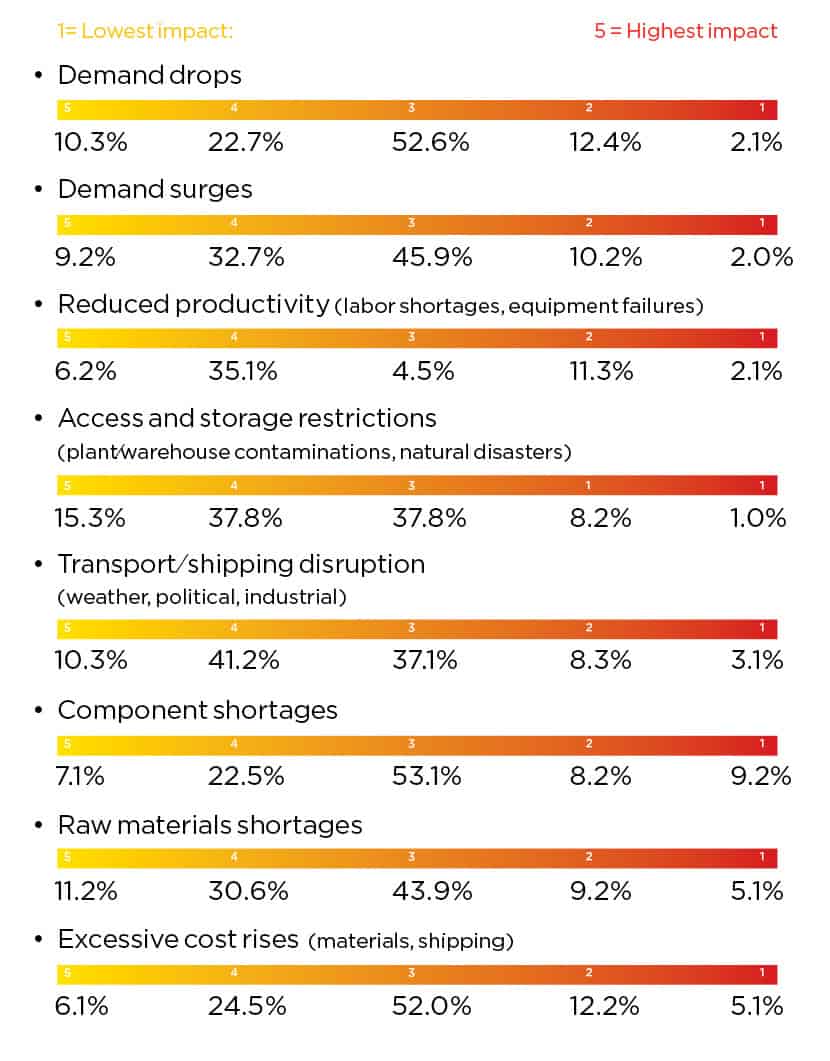

Perhaps the lingering supply chain issues stem from several disruptive forces and a synergistic effect as several supply disruptions combine to become causes for further disruption. We asked about eight different types of disruptions that manufacturers have experienced in recent years and their impact. Leading the charge, component shortages and excessive cost rises for materials and shipping both ranked as a four or five (highest level of impact) for 17% of respondents, while demand drops, raw materials shortages and reduced productivity from labor shortages and equipment failures round out the top five disruptions with the highest impact. [CHART 4]

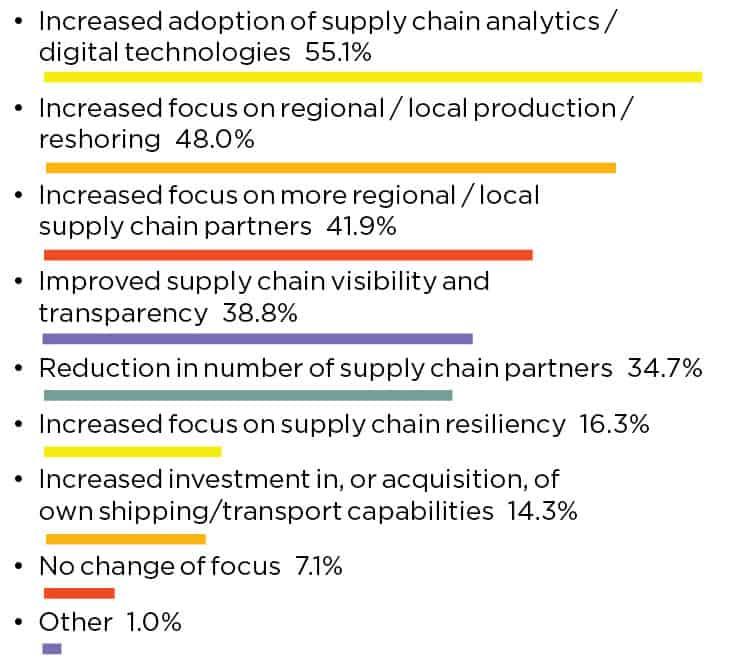

But from adversity, innovation arises, and manufactures report they are taking steps to mitigate future supply chain disruption. Among the leading new strategies, 55% say they are adopting supply chain analytics and digital technologies; 48% are increasing their focus on regional or local production and reshoring; 42% are focusing on regional and local supply chain partners; and 39% are improving their supply chain visibility and transparency. [CHART 5]

1. Pandemic-related Disruptions Persist

Q: To what extent have pandemic-induced supply chain disruptions eased for your company? (select one)

2. Global Unrest and Tension Causing Minimal Supply Chain Disruption

Q: To what extent have the Ukraine War and tensions with China affected your supply chain? (select one)

3. Most Expect Disruptions to Subside in Next 12-24 Months

Q: If you are still experiencing supply chain disruptions, when do you expect the disruptions to subside? (select one)

4. Components, Raw Materials, and Costs Causing Biggest Supply Chain Impact

Q: Over the last several years, what have been the most impactful types of supply chain disruptions you have encountered? (scale 1-5, where 5 is highest level of impact)

5. Analytics/Digital Tech and Supply Chain Geography are Biggest Strategies to Avoid Disruption

Q: What strategies are you adopting to mitigate future supply chain disruption? (select all that apply)

Part 2: Improving Resiliency

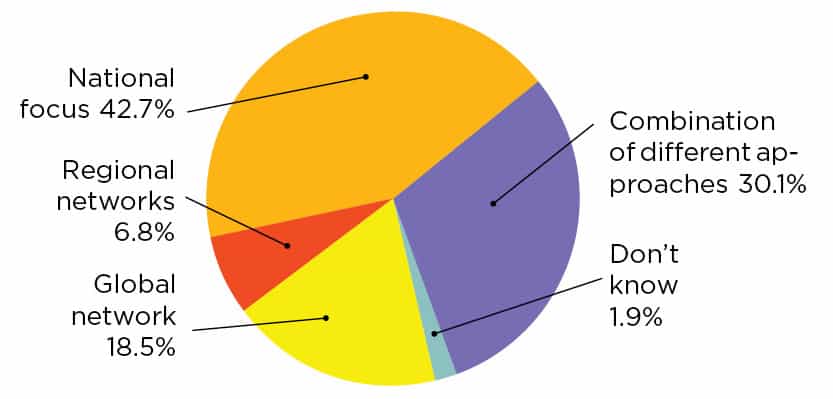

Building off these new strategies, manufacturers report a dramatic shift in their supply chain network’s geography. In MLC’s 2022 supply chain survey, 51% reported a global supply chain network. Now, just 18% of respondents report a global network. This shift has led to a significant increase in those with a national focus (43% in 2023 compared to 12% in 2022) and a combination of different approaches (30% in 2023 compared to 19% in 2022). [CHART 6]

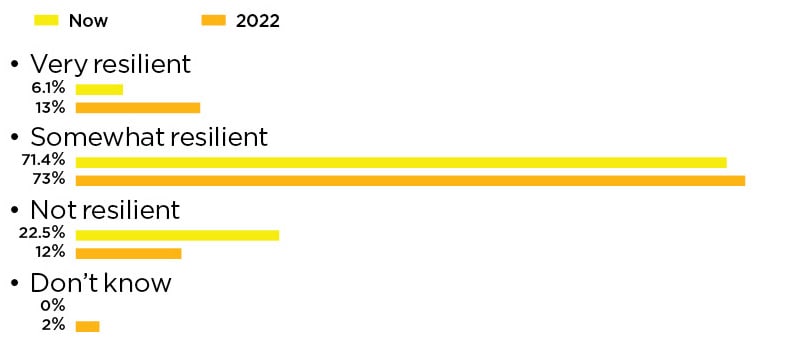

The rapid nature of this shift may be responsible for a less resilient supply chain in the short-term. While most respondents still report their supply chain is somewhat resilient (71% in 2023 compared to 73% in 2022), there has been an increase in those reporting that their supply chain is not resilient. For 2023, that number stands at nearly 23% while it was 12% in April 2022. [CHART 7] Time will tell if this is, in fact, a temporary regression as supply networks realign geographically.

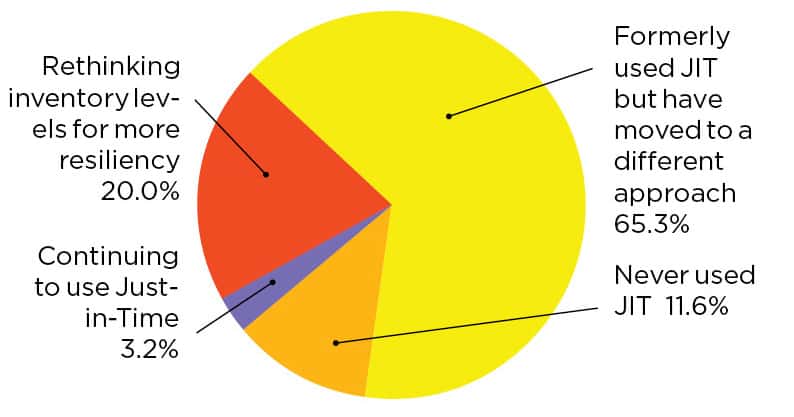

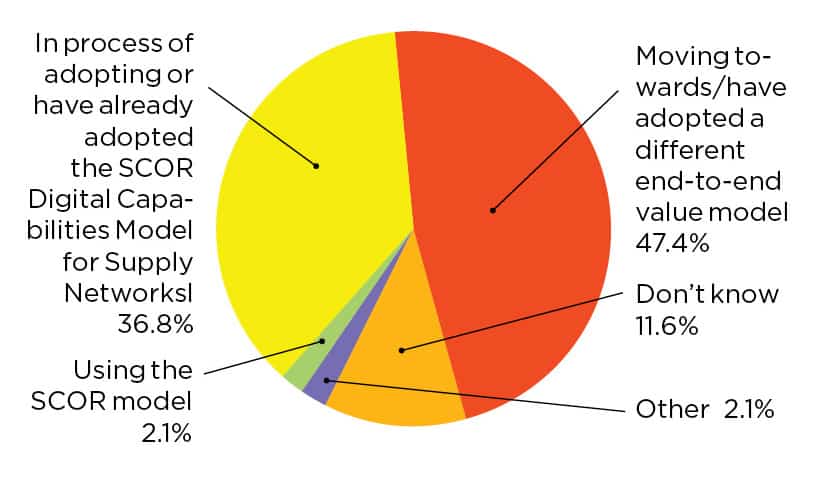

One way manufacturers may be bolstering their resiliency is reexamining traditional supply chain strategies. There is a clear move away from the Just-in-Time (JIT) approach. In 2022, 12% reported that they were continuing to use JIT, while just 3% continue to use it according to the latest survey data. Now, 65% of respondents report that they formerly used JIT, but have moved to a different approach. [CHART 8] Additionally, just under half of respondents (47%) report they are moving towards or have adopted an end-to-end value model other than SCOR. That leaves 2% that are using SCOR and nearly 37% that are adopting or have adopted the SCOR Digital Capabilities Model for Supply Networks. [CHART 9]

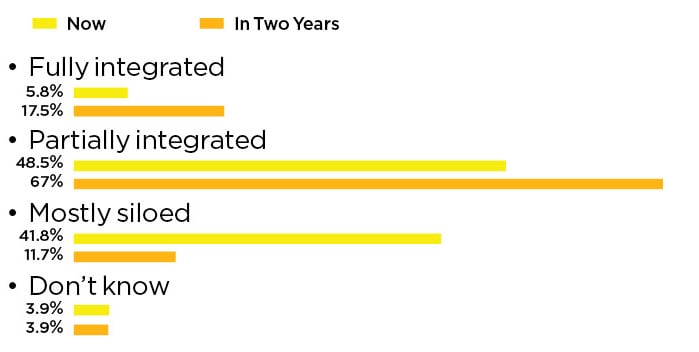

As these shifts take place, there is some optimism that the efforts will pay off in the next two years. Forty-one percent of respondents report that their supply chain functions are mostly siloed today, but that number is predicted to drop to just under 12% in 2025. At the same time, partially integrated supply chains are predicted to grow from 49% to 67% while those with a fully integrated supply chain are forecasted to increase from 6% to 18%. [CHART 10]

6. Companies Shift Away from Global Supply Chain Network

Q: Geographically, how is your supply chain network structured? (select one)

7. Still, resilient supply chains remain an issue

Q: How would you rate your current supply chain’s resiliency? (select one)

8. Just-in-Time’s Usage Continues to Fade

Q: How would you describe your company’s use of the Just-in-Time approach? (select one)

9. End-to-End Value Models Moving Toward Majority Adoption

Q: Does your company use SCOR as its basic supply chain model or are you using or moving toward a different end-to-end value model? (select one)

10. Siloed Supply Chain Functions Begin to Disappear

Q: To what extent are your supply chain functions integrated today and do you expect them to be integrated in two years’ time? (select one)

Part 3: Digital Supply Chains

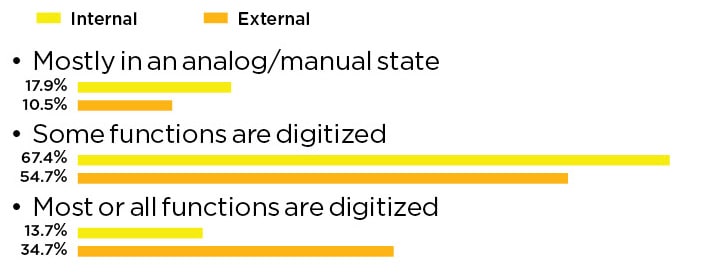

For respondents, their digital maturity for external supply chain functions is slightly outpacing their internal supply chain functions’ digital maturity. Just under 90% say some, most or all their external functions are digitized, while 81% say some, most or all their internal functions are digitized. This means that about 18% of respondents characterize their internal supply chain functions as mostly in an analog or manual state, while about 11% of respondents say the same about their external functions. [CHART 11]

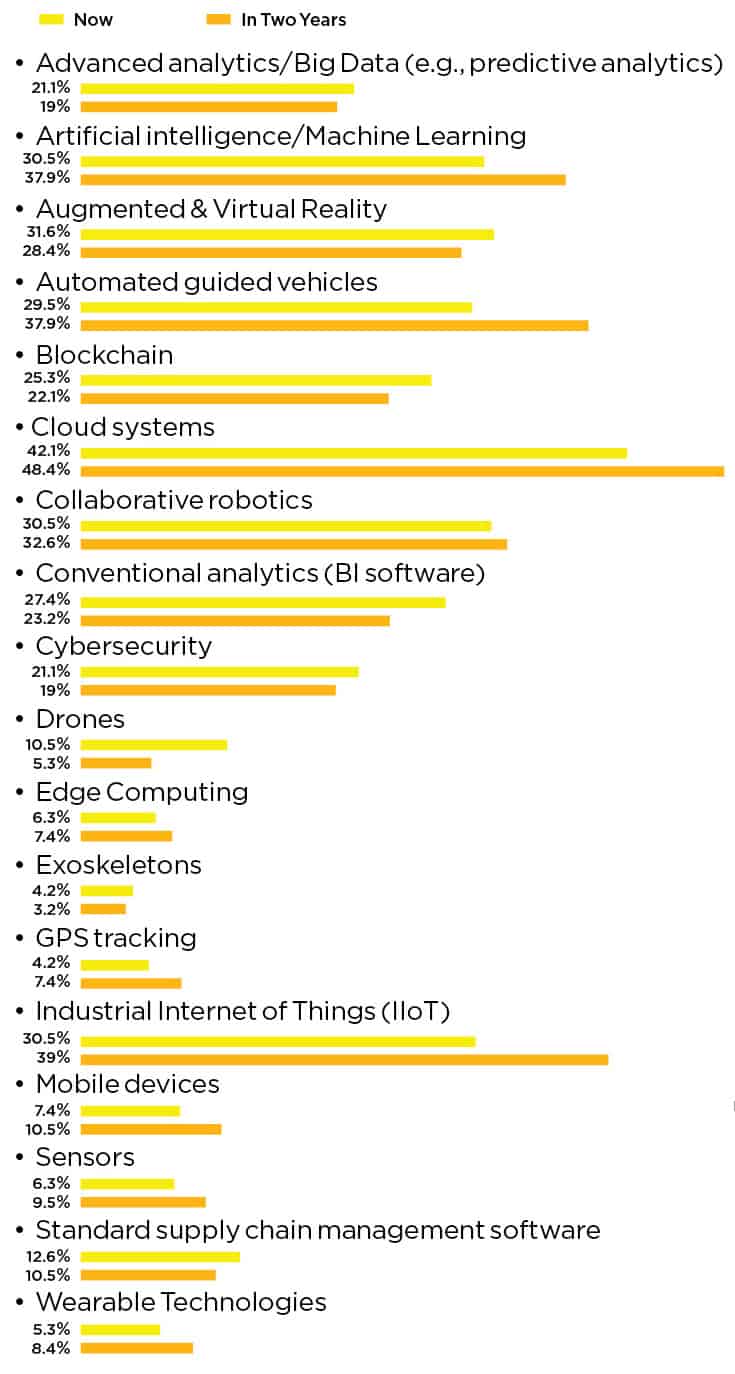

Many technologies are now in use to help digitize manufacturers’ supply chains. Currently leading the pack are cloud systems (in use for 42% of respondents) and augmented and virtual reality (32%). Rounding out the current top five, are artificial intelligence/machine learning, collaborative robotics, and Industrial Internet of Things (IIoT), all of which are being used to digitize just under 31% of respondents’ supply chains. Looking ahead to 2025, use of these technologies will most likely increase. Cloud systems are expected to be in use for 48% of respondents; IIoT is expected to be employed by 39% of respondents; cobot deployments will grow slightly and be in use in 33% of respondents’ supply chains; and AI/ML is expected to be in use for 38% of respondents. Our respondents also expect automated guided vehicle usage to grow from 30% now to 38% in 2025, while augmented and virtual reality usage will slip to 28% in two years’ time. [CHART 12]

As digital technology adoption grows, companies are no longer taking the opportunity to also redesign their supply chain processes. This may be because so many reported that they were redesigning their processes in the 2022 survey. At that time, 72% said they were redesigning their processes as they adopted more digital technologies. In the most recent survey, however, that number has dropped to just 26%. [CHART 13] If AI adoption grows as expected by 2025, it will be interesting to keep an eye on supply chain process redesigns to see if there is a corresponding increase.

11. Digital Maturation Continues

Q: Which description best characterizes the digital maturity of your internal and external supply chain functions today (plan, source, make, deliver)? (select one)

12. Cloud Systems, AI/ML and AGVs are the Present and Future of Digital Supply Chains

Q: What technologies are you currently using and do you expect to be using in two years to digitize your supply chain? (select all that apply)

13. Digital Adoption Not Driving Supply Chain Redesigns

Q: As you adopt more digital technologies across your supply chain, are you also taking the opportunity to redesign your supply chain processes? (select one)

Part 4: Supply Chain Partners

Perhaps driven by more localized supply networks, companies are making an effort to help their supply partners accelerate their digitization efforts. In 2023, 54% of respondents say they are helping their supply partners. This is up significantly from 2022 when just 19% reported they were supporting this effort. [CHART 14] Eventually, these efforts may ensure a more effective end-to-end digital supply network including multiple supplier tiers.

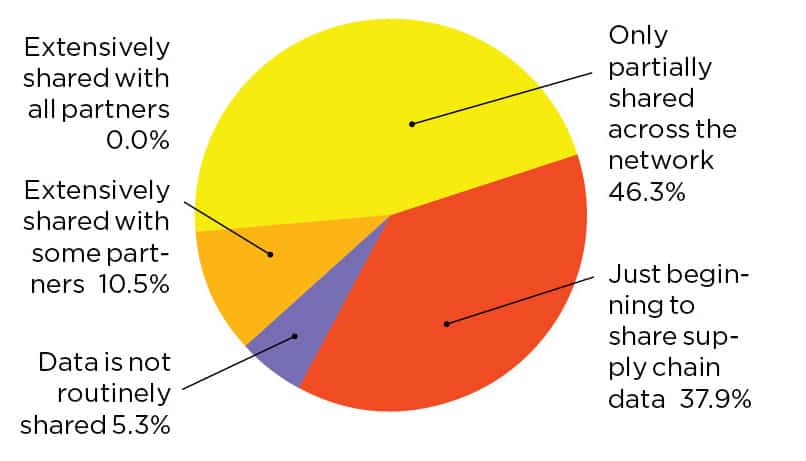

A potential area for growth with partner collaboration is data sharing. Just under 11% of respondents say they share data extensively with some partners while 5% say data is not routinely shared. But there is a light at the end of the tunnel: 38% say they are beginning to share supply chain data among partners and another 46% say they are partially sharing data across their networks already. [CHART 15]

14. More than Half Aid Supply Chain Partners’ Digital Maturity

Q: Has your company made any specific efforts to help support your supply chain partners accelerate the maturity of their digitization efforts to ensure a more effective end-to-end digital supply network? (select one)

15. Nearly All Respondents Share Some Data Between Supply Chain Partners

Q: To what extent is data routinely shared between any or all of your supply chain partners? (select one)

Part 5: Challenges, Goals and Outcomes

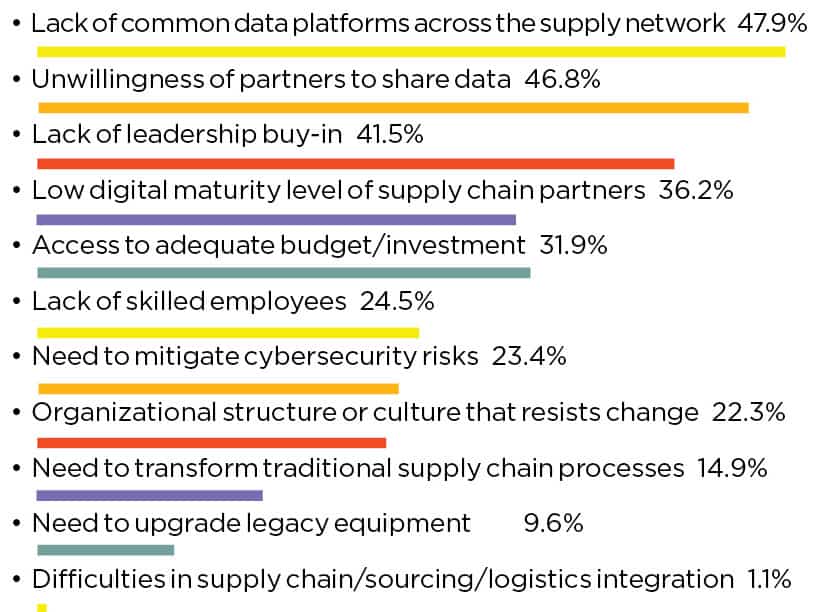

To implement an end-to-end digital supply chain strategy, significant challenges exist that must be addressed with organizational and people changes or new technologies. Respondents were asked to identify their top three challenges. Lack of common data platforms across the supply network led the way in the 2023 survey with 48% of respondents identifying this challenge. This is down slightly from 2022 when it appeared in 53% of respondents’ top three. Trailing just behind, 47% of respondents labeled the unwillingness of partners to share data as one of their biggest challenges. Beyond data hurdles, 42% say a lack of leadership buy-in and 36% say low digital maturity of supply chain partners are holding back their digital supply chain strategy. Meanwhile, 32% say that access to an adequate budget or investment is one of their top three challenges. [CHART 16]

Survey respondents are seeking several business goals related to their digital supply chain transformation. Increased supply chain resiliency, improved customer experience, and new business model/competitive advantage rank as the top three most important goals. These were identified as high importance on 43%, 33%, and 31% of the surveys, respectively. [CHART 17]

16. Data Issues Pose Biggest Challenge to End-to-End Digital Supply Chain Strategy

Q: What are your company’s primary challenges in implementing an end-to-end digital supply chain strategy? (select top three)

17. Customer Experience, Resilience Biggest Goals of Digital Supply Chain Transformation

Q: How important are the following business goals associated with your digital supply chain transformation? (rate as low, moderate or high importance)

About the author:

Jeff Puma is Content Director for the Manufacturing Leadership Council

Survey development was led by the MLC editorial team with input from the MLC’s Board of Governors.

Survey: On Board with Technology, At Sea with Strategy

Manufacturing executives want to know what digital transformation can do for their businesses, but an overall plan to find out is lagging for most.

![]()

George Westerman, Principal Research Scientist with the MIT Initiative on the Digital Economy, describes digital transformation’s immense opportunity and potential pitfalls with the following analogy: “When digital transformation is done right, it’s like a caterpillar turning into a butterfly, but when done wrong, all you have is a really fast caterpillar.” He contends that business leaders are often thinking only in terms of “fast caterpillars” without focusing on the butterfly that could emerge instead.

The results of the Manufacturing Leadership Council’s Digital Leadership survey seem to indicate that leadership teams are piecemeal in their efforts around digital transformation – they want to know what technology is out there and how it’s used, but for many organizations there is seldom a focus on building or developing a comprehensive digital strategy, there is no change management strategy in place, and no formal training plan to educate workers and leadership on digital transformation.

The takeaway is that many feel their organizations’ future success is vulnerable because of this lack of preparedness – and that an overall lack of strategy may indeed be creating more “fast caterpillars” than digital butterflies.

In terms of overall approaches to leadership, though, most say that there is no significant difference in skills required to be a leader in the digital era vs. prior ones – which could indicate that the tried-and-true qualities of fairness, innovation, assessing competitiveness, and having a clear vision for the future are still what most see as the hallmarks of effective leadership.

Below are more detailed results for the 2023 Digital Leadership survey.

Part 1: M4.0 Organizational Preparation

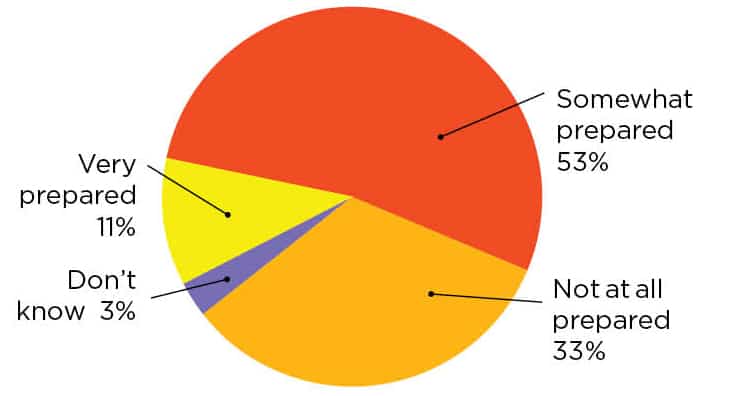

While the majority of survey respondents said their executive management team is at least partially prepared to lead in the era of digital transformation, a whopping one-third said that team was “not at all prepared” for such change. When this survey was previously conducted in 2022, only 10% said that their executive leadership was in such a precarious position. What may account for this?

Q: How prepared do you think your company’s executive management team is to lead and manage digital transformation? (Select one)

As many job roles of the future do not yet exist, it is understandable that many manufacturers feel they have only a partial understanding of the skills that will be needed in the coming years.

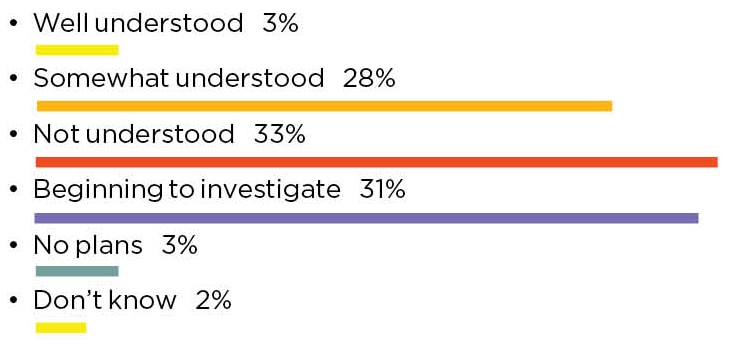

Q: How well prepared do you think your company is in understanding the new digital roles and skills that you will need in the next few years? (Select one)

Change management strategies are still lacking at many organizations – perhaps reflecting an overall lack of understanding on the changes that will be necessary.

Q: Has your leadership team created an organizational change management strategy to help support its digital strategy? (Select one)

Formal training for digital technologies is also nonexistent at many organizations, perhaps unsurprising given the lack of a change management strategy to underpin such transformation.

Q: Does your company have a formal training plan to educate workers and leadership around the requirements of digital transformation?

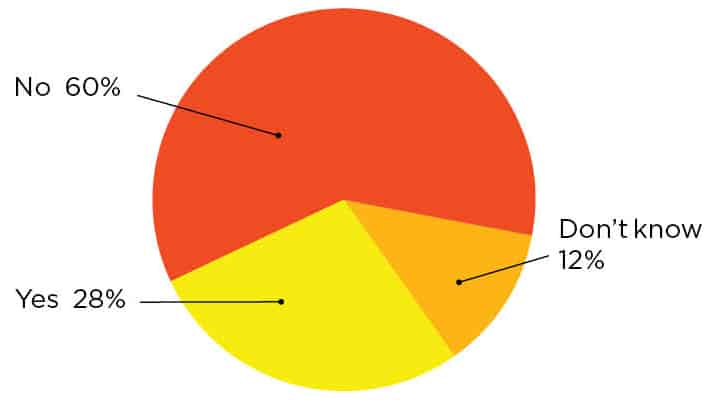

There is a measured level of anxiety around organizational vulnerability due to digital preparedness level (or lack thereof) – though a slight decrease from the 13% who felt their organization was “very vulnerable” in the 2022 survey.

Q: How vulnerable will your company’s future success be as a direct result of your company’s current level of preparedness for digital transformation? (Select one)

PART 2: The Current State of Digital Transformation Leadership

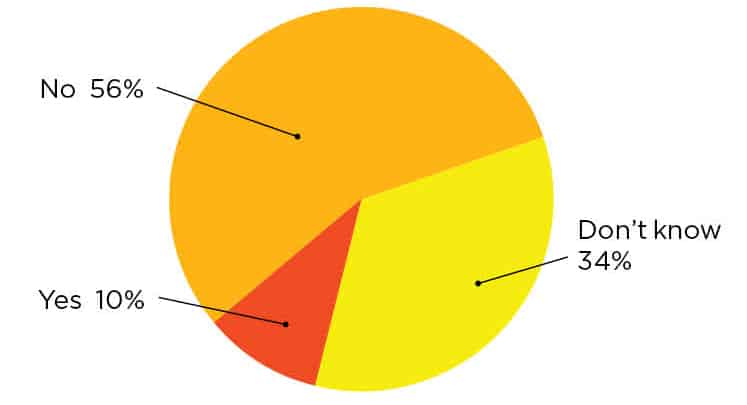

The most common person in charge of digital transformation typically resides in the C-suite, with the Chief Operations Officer coming in on top with the Chief Executive Officer not far behind..

Q: Who is leading the charge around your digital transformation efforts in your organization? (Select one)

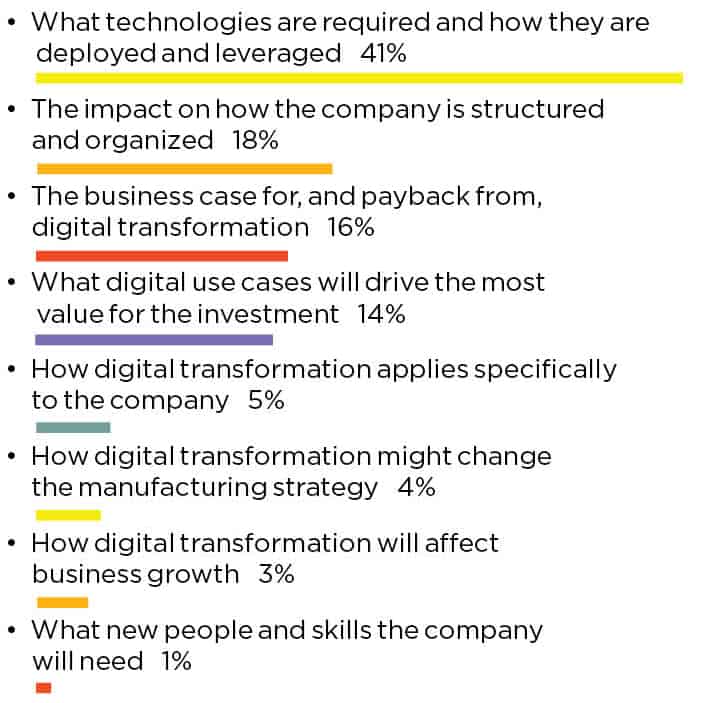

As technology evolves and the associated use cases become more understood, it’s not surprising that executive leadership most frequently wants to know which technologies are best for their operations and how they can be leveraged to their best capabilities.

Q: What’s the most important thing your company’s executive management team wants to know about digital transformation? (Select one)

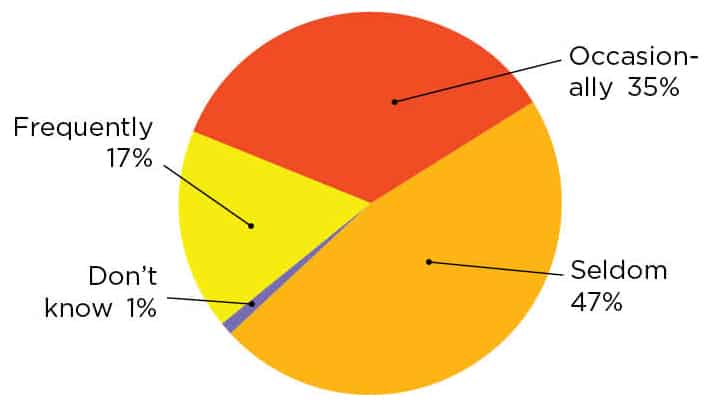

In addition to the related responses on a lack of change management strategy and lack of formal training for digital transformation, the vast majority of respondents also report that their leadership teams only occasionally or seldom devotes time or attention to developing or updating a digital strategy.

Q: How much time and attention does your leadership team devote to creating and/or updating its digital strategy? (Select one)

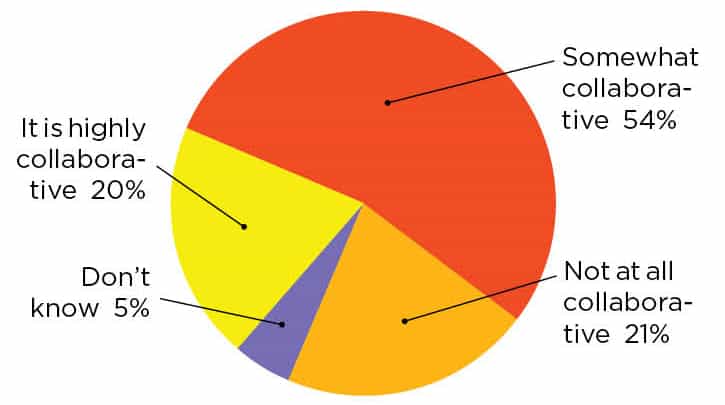

Collaboration may be something of a bright spot for digital strategy, as most say that their leadership team is at least somewhat collaborative in this area, with one-fifth saying they are highly collaborative.

Q: How collaborative is your leadership team across multiple areas of the organization in the development and assessment of its digital strategy? (Select one)

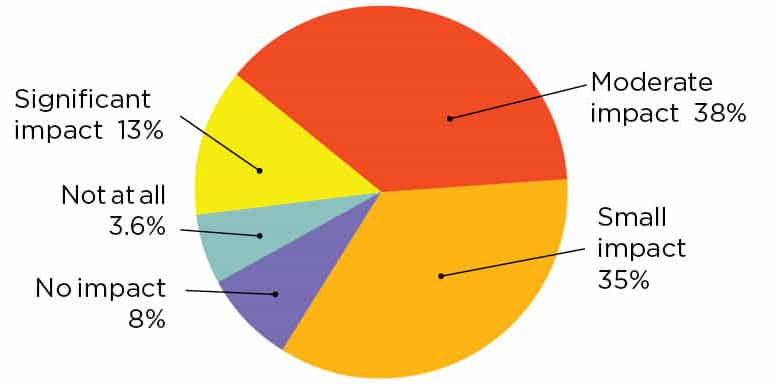

It appears that even with an increase in automation and other technologies that can contribute to a reduced headcount, most respondents feel their organization will still have a “help wanted” sign out front. Only 13% see technology having a significant impact on reducing unfilled job openings.

Q: What impact do you think the increasing adoption of automation and advanced digital technologies will have on reducing unfilled job openings in your company in the future? (Select one)

PART 3: A New Era for Manufacturing Leadership

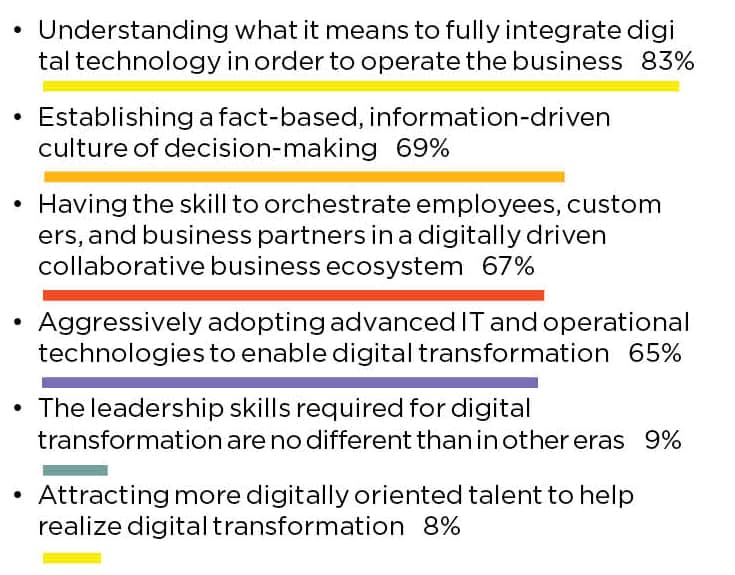

Understanding of technology and its operational integration is cited by far as the best description of what leadership means in the digital era. Using data to make decisions, developing digital ecosystems and acting as a “digital evangelist” for aggressive technology adoption followed closely behind.

Q: Which statements best describe what leadership means in the digital era? (Select top 3)

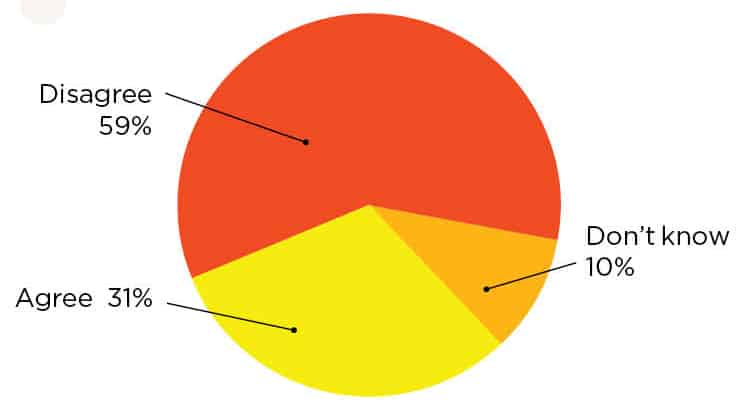

The more things change, the more they stay the same? Only about a third of respondents felt that digital operations require a significantly different leadership approach vs. any other era.

Q: Do you agree or disagree with this statement: “The emergence of digitally driven operations and business models will require a substantially different approach and set of skills on the part of manufacturing company leadership.” (Select one)

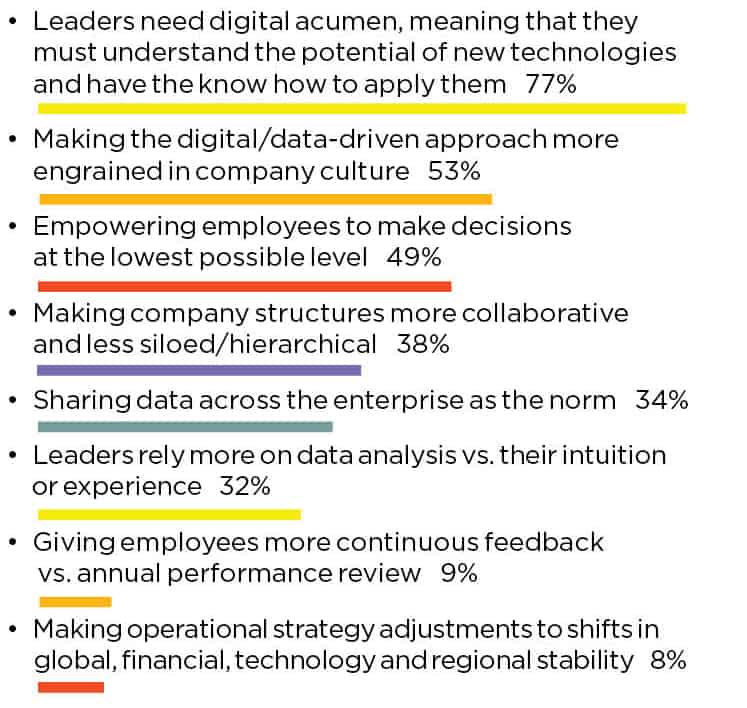

Technological understanding is cited as the most important aspect of a digital leadership approach, followed by instilling a data-driven approach to decision-making throughout the company culture.

Q: Which leadership approaches do you feel are most important in the digital era? (Select top 3

PART 4: What Leaders Need for the Future

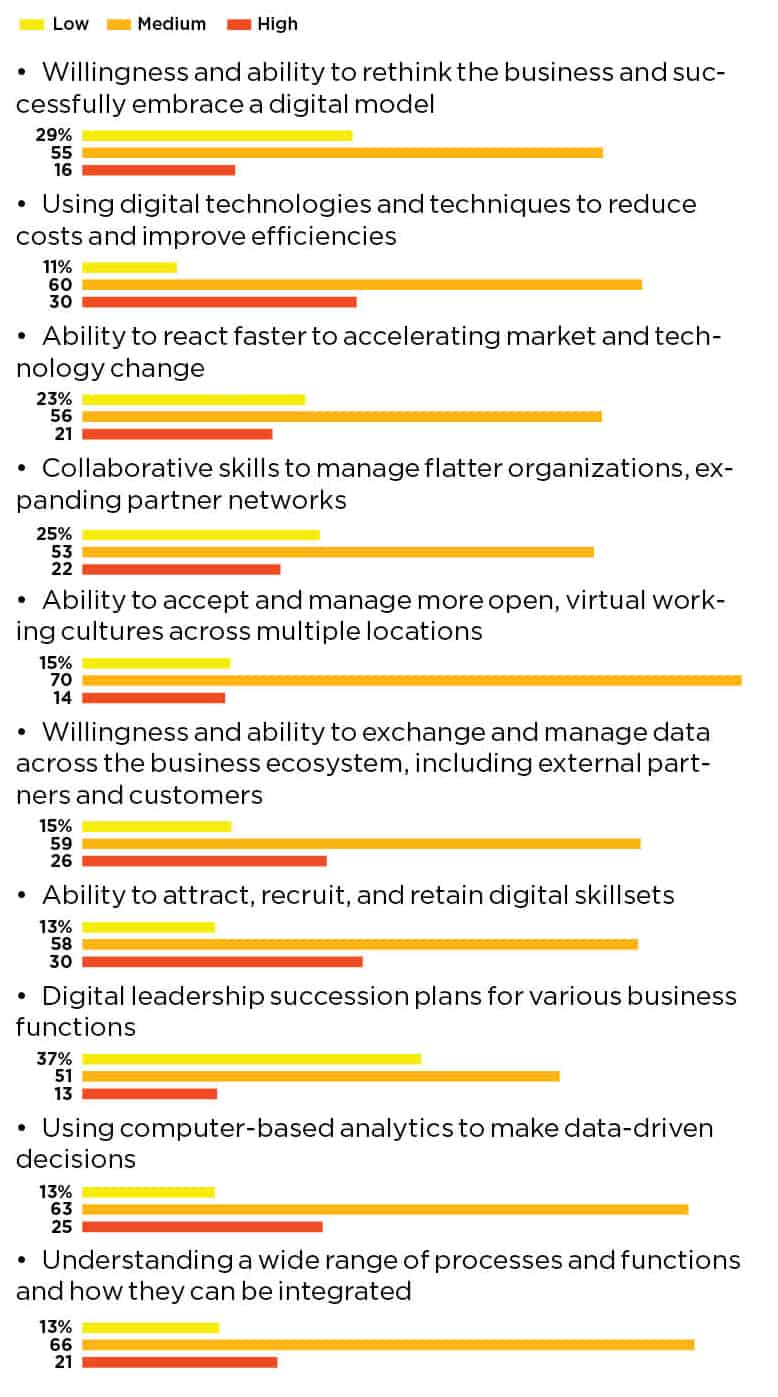

The ability to manage virtual and remote teams ranked among one of the more important skills that leaders will need for the future, followed by using data to make decisions and understanding process and functional integration across the organization.

Q: Looking ahead, what degree of importance would you assign to the following digital leadership skills and abilities? (Rate each on scale of Low/Medium/High)

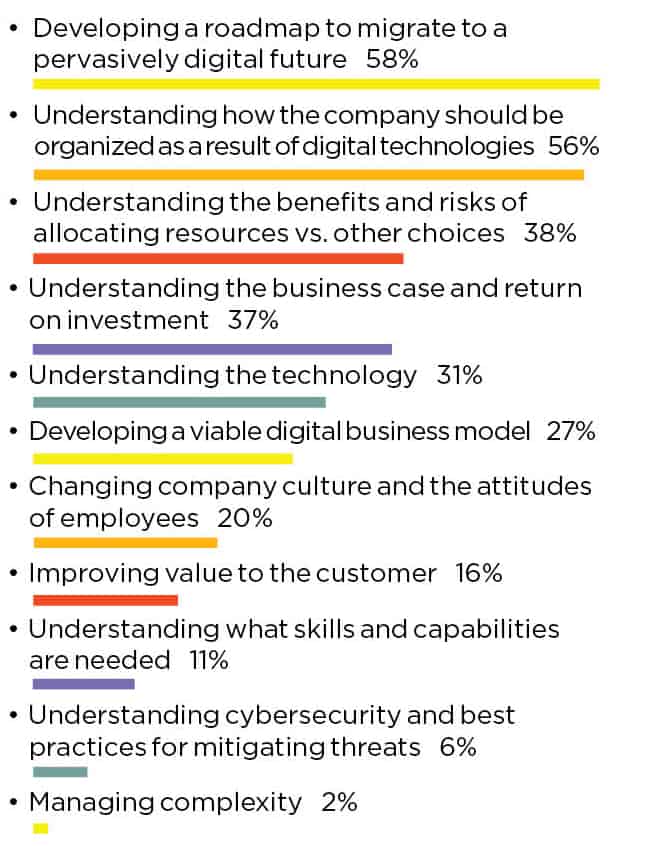

While many respondents said that their organization did not currently have a clear digital strategy for the future, they clearly felt that developing such a roadmap was important for navigating the future, in addition to understanding how the company should be structured and organized to best take advantage of digital technologies.

Q: In thinking about the requirements and implications of digital transformation, what do you think are the most important challenges for leadership? (Select top 3)

About the author:

Penelope Brown is Senior Content Director for the Manufacturing Leadership Council

Survey development was led by the MLC editorial team with input from the MLC’s Board of Governors.

Survey: Data Mastery is Slow to Mature but Essential

Manufacturers show some progress with data mastery efforts, but much opportunity for growth exists.

![]()

When MLC last fielded its Data Mastery survey in 2021, senior content director Penelope Brown wrote of the results, “Manufacturing data mastery is in its tween years for most enterprises – certainly past its infancy, but still awkward and gawky and not quite fully formed.”

If data mastery was a tween then, the effort is on the final stages before becoming a teenager now. Like a tween, there has been some maturation but also some regression in how companies are accessing and using data and analytics. Likewise, companies can see dramatic development in specific areas of data utilization, but each organization seems to mature at its own pace while encountering a wide array of challenges and pursuing various desired outcomes and focus areas.

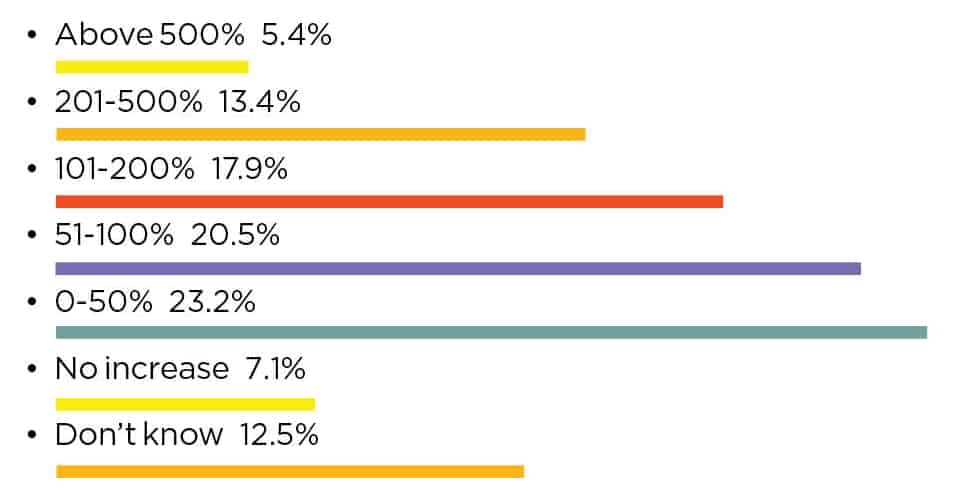

Why is progress slow? To further the tween metaphor: perhaps it is growing pains. More than one-third of respondents tell us that the volume of data they’re collecting has at least doubled. Nearly 20% say the amount of data has at least tripled. Before this exponential growth came into play, companies were already dealing with an uphill climb to verify and analyze data. Given this rapid growth – like in tween years – there’s bound to be some awkwardness and slower progress.

Still, it is clear from the 2023 MLC Data Mastery and Analytics survey that mastering manufacturing data will be essential to future competitiveness. Presently, 91.1% of respondents report that data has allowed for more accurate or timely decisions, both of which are essential to overcome the pressures that businesses face now and those they will face as their data mastery skills continue to mature.

Read on for key findings and selected graphs from the 2023 Data Mastery and Analytics survey.

Part 1: Data Strategy and Governance

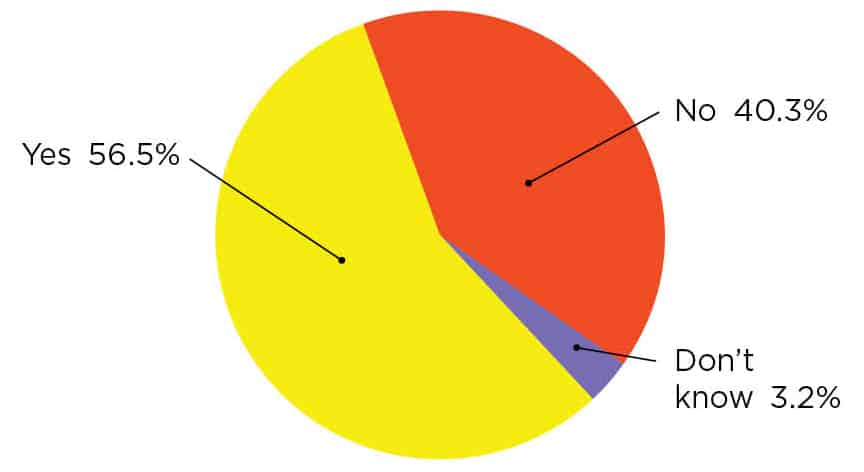

The majority of respondents have a formal data plan and guidelines in place, but there has been little change since the last time we fielded this survey in 2021. Currently, 56.5% of respondents say they have a corporate-wide plan, strategy, or formal guidelines for how data is collected and organized. This number sat at 55% in 2021.

Q: Does your company have a corporate-wide plan, strategy, or formal guidelines for how data is collected and organized across the enterprise, including manufacturing operations? (select one)

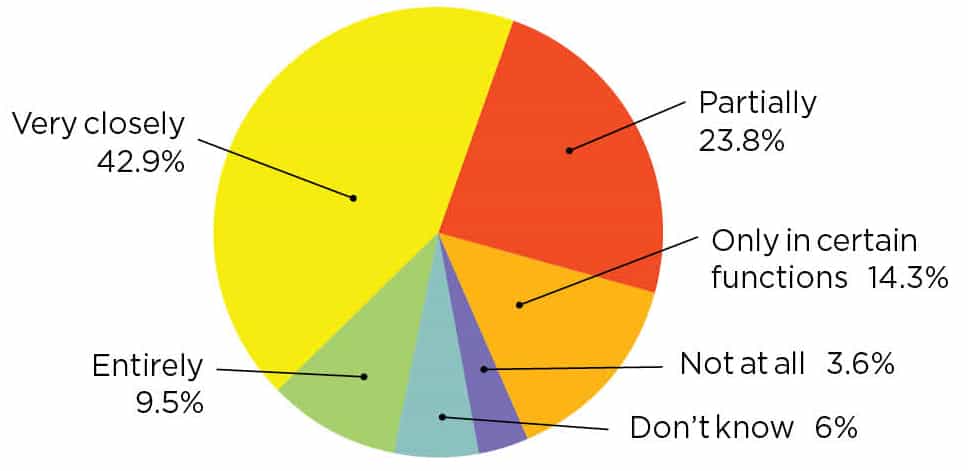

For those with a formal corporate-wide data strategy, nearly all (90.5%) see at least some alignment to overall business strategy, but only 52.4% say it aligns entirely or very closely.

Q: If your company has a corporate-wide plan, strategy, or formal guideline for how data is collected and organized, how closely do you feel this data strategy is aligned to your company’s overall business strategy? (select one)

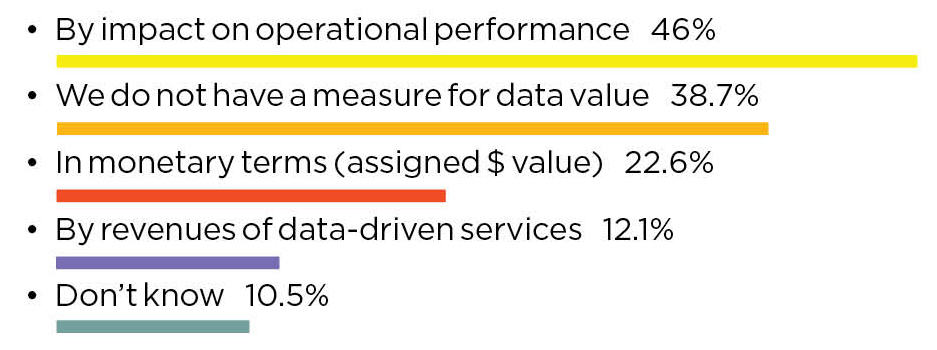

Measuring data’s value is still elusive to many organizations. However, there’s been increases in assigning monetary value and measuring revenues of data-driven services in the past two years. In fact, 22.6% of respondents now say they measure the value of data in monetary terms compared to 4% in 2021. Meanwhile, 12.1% say they measure data’s value by revenues of data-driven services compared to 3% in 2021.

Q: How do you measure the value of the data in your organization? (select all that apply)

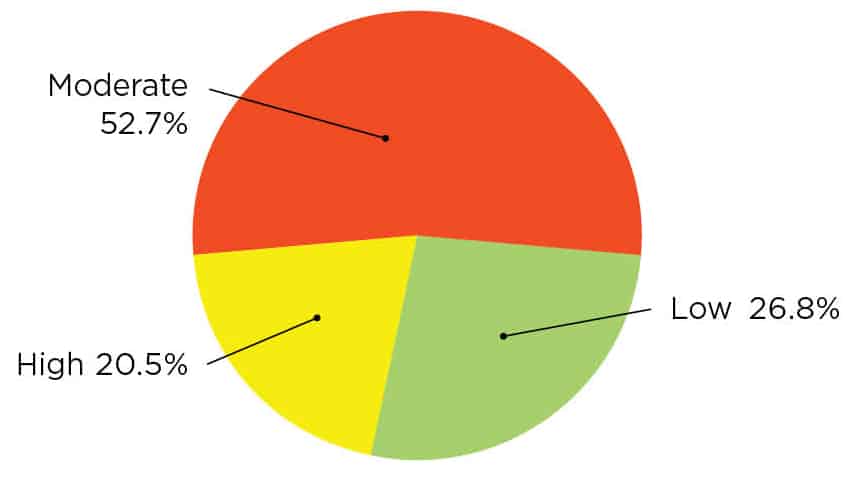

Manufacturers see a slight positive shift in their ability to collect the right data the business needs. In 2021, 16% of survey respondents ranked their company as highly able to collect the right data. In the latest survey, that number has climbed over 20%. On the low end of the spectrum there was only minimal change moving from 26% in 2021 to 26.8% in 2023.

Q: How would you rank your company’s ability to collect the right data the business needs from your manufacturing operations? (select one)

Part 2: Data Collection, Use, and Analysis

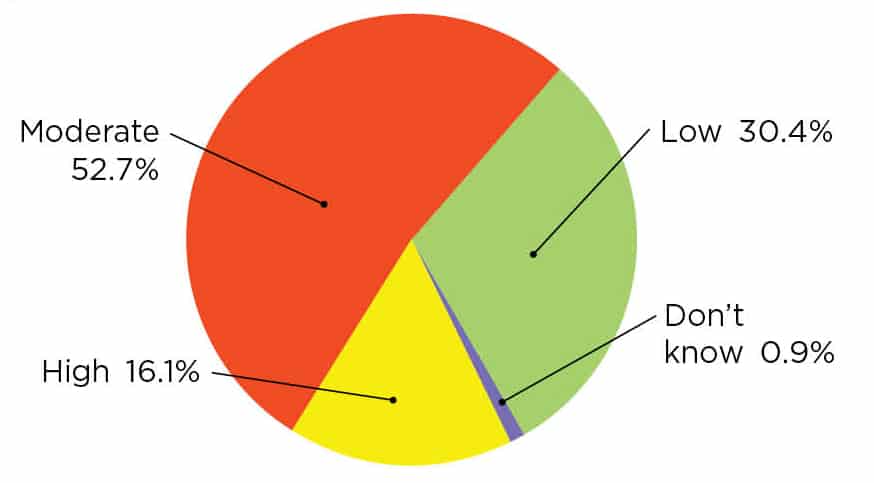

The ability to analyze manufacturing operations data is an opportunity for growth. Just over half of respondents report their company is moderately able to analyze the data, while 30.4% say they have low competency.

Q: How would you rank your company’s ability to analyze the data from your manufacturing operations? (select one)

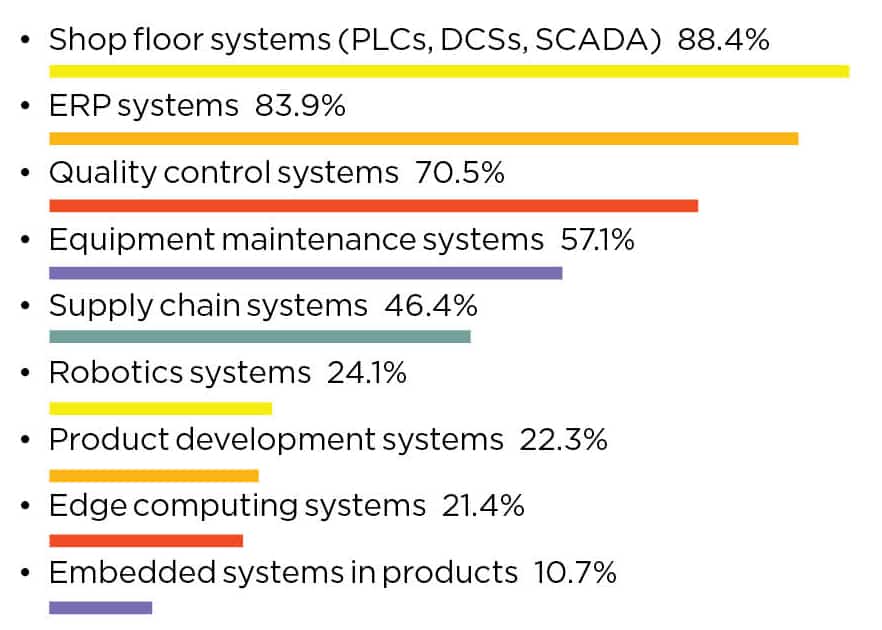

Shop floor systems and ERPs remain the primary data sources. In fact, shop floor systems use increased from 79% in 2021 to 88.4% in 2023, while ERP systems increased from 77% in 2021 to 83.9% in 2023. Quality control systems, equipment maintenance systems, supply chain systems, and robotics systems saw similar increases since the previous survey, but product development systems fell 16 percentage points to 22.3%.

Q: What are the primary systems that generate your manufacturing data today? (select all that apply)

The survey revealed that there is considerable room for growth in real-time data collection. Less than half of respondents report their company’s data is comprised of 51% or more real-time or near real time data.

Q: What proportion of the data you collect today is real-time or near real time, not batch or historical? (select one)

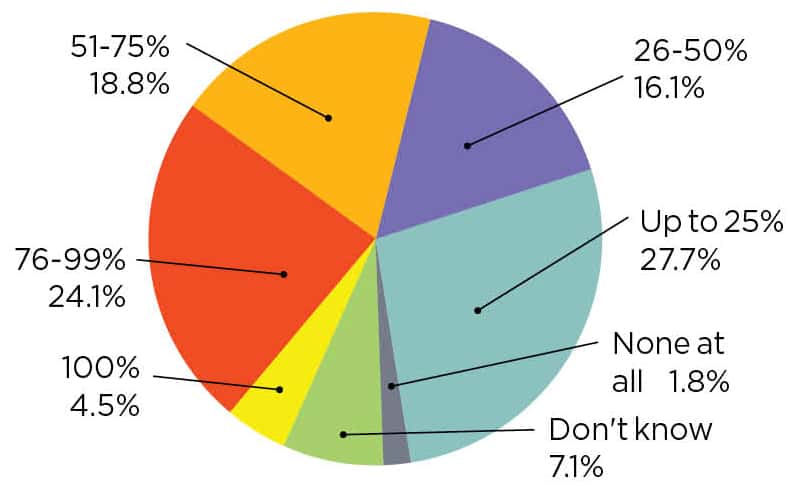

In the past two years, companies are collecting more manufacturing data. Eighty percent report they’ve seen at least some increase in the amount of data collected. Meanwhile, more than one-third of respondents say the amount of data has at least doubled in that time.

Q: What has been the percentage increase in the amount of manufacturing data you are now collecting compared to two years ago? (select one)

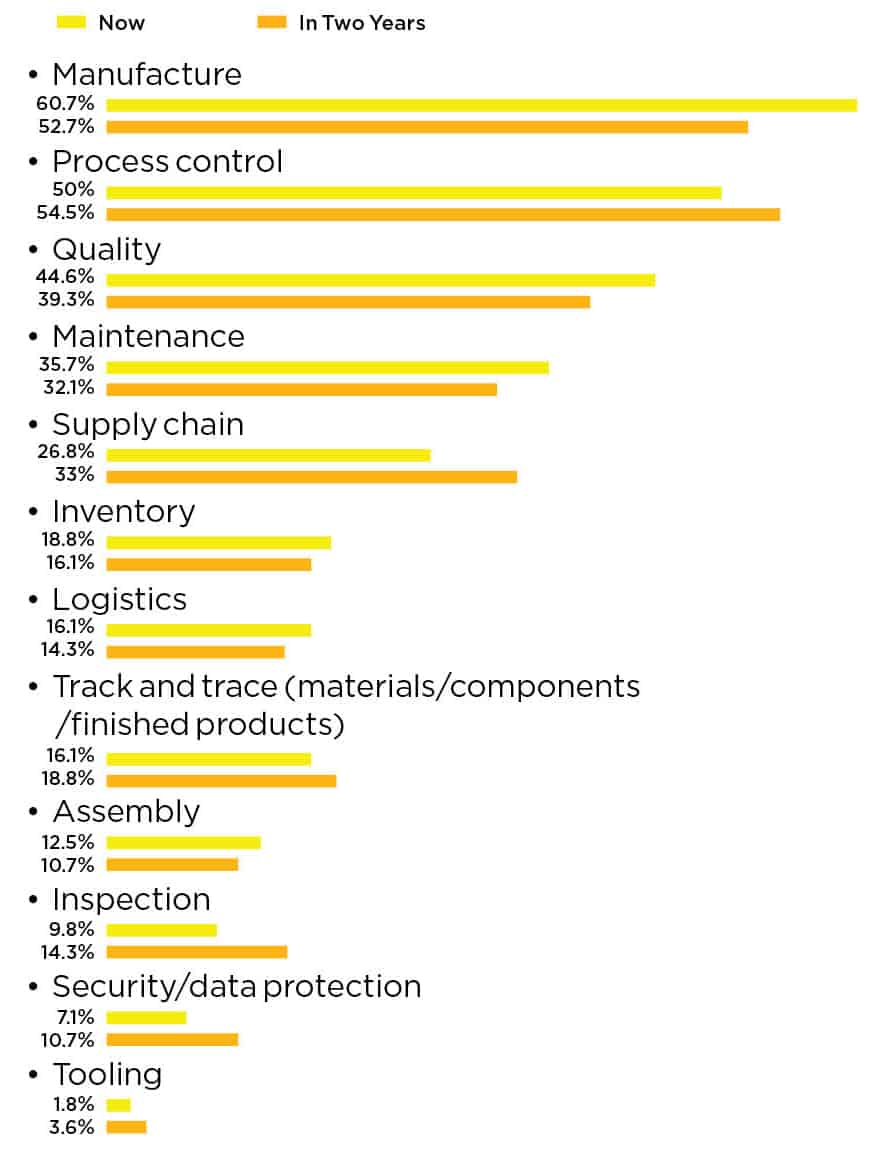

Looking ahead at the operational focus for data projects in two years, respondents foresee a varying shift from manufacture, quality, maintenance, inventory, logistics, and assembly to process control, supply chain, track and trace, inspection, security/data protection, and tooling.

Q: What are your primary areas of operational focus for data projects today and what do you expect the primary focus will be in 2 years’ time? (select top three)

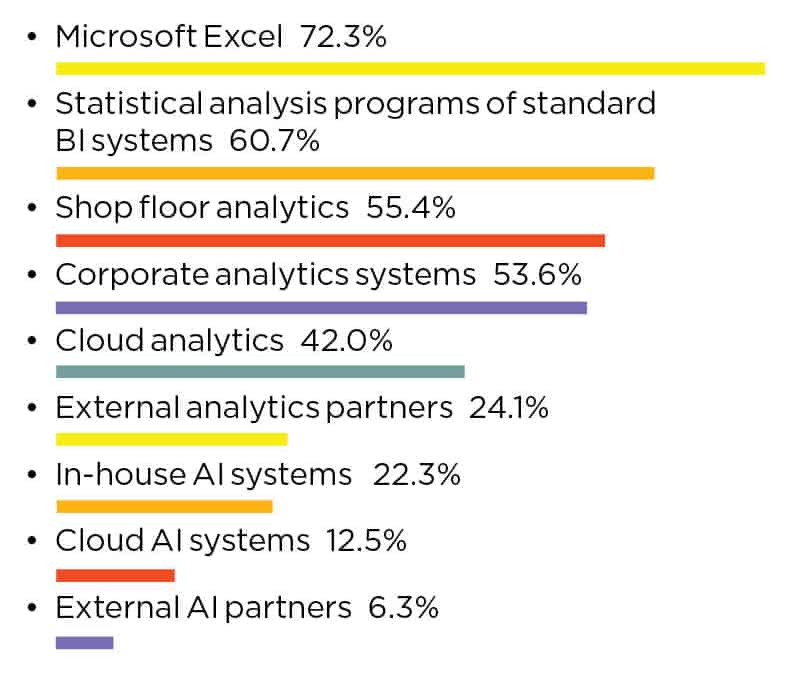

Microsoft Excel remains the reigning champion of data analysis tools. In 2021, 71% of survey respondents reported that Excel was in their data analysis toolkit. That number rose slightly in 2023 to 72.3%. Statistical analysis programs of standard BI systems jumped from 47% in 2021 to 60.7% in 2023. This moved it from the fourth most used tool in 2021 to second place this year. Meanwhile, manufacturers are increasingly outsourcing analytics, with 24.1% utilizing external analytics partners this year compared to 14% in 2021. Somewhat surprising, the use of AI systems has decreased from 48% (when taking in-house, cloud and external AI partners in aggregate) to 41% in 2023.

Q: What systems do you use to analyze the manufacturing data you collect? (select all that apply)

Respondents’ companies are evenly split when asked about verifying the accuracy and quality of raw data. About 46% report they have a process while approximately 45% say they do not. In the 2021 survey, for comparison, 49% reported they had a process while 46% reported they did not.

Q: Does your company have a process to verify the accuracy and/or quality of the raw data before decisions are made on it? (select one)

Part 3: Outcomes and Challenges

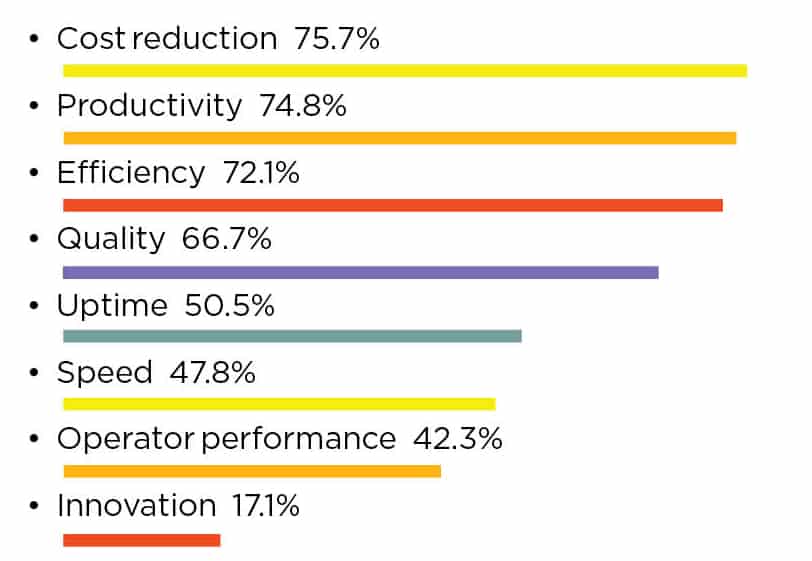

Increased data access has resulted in a variety of operational improvements. Leading the charge are cost reductions, productivity improvements, efficiency, quality, and uptime – all of which were cited as an improvement seen by 50% or more of survey respondents.

Q: In what ways has increased access to manufacturing data helped you to improve your manufacturing operations? (select all that apply)

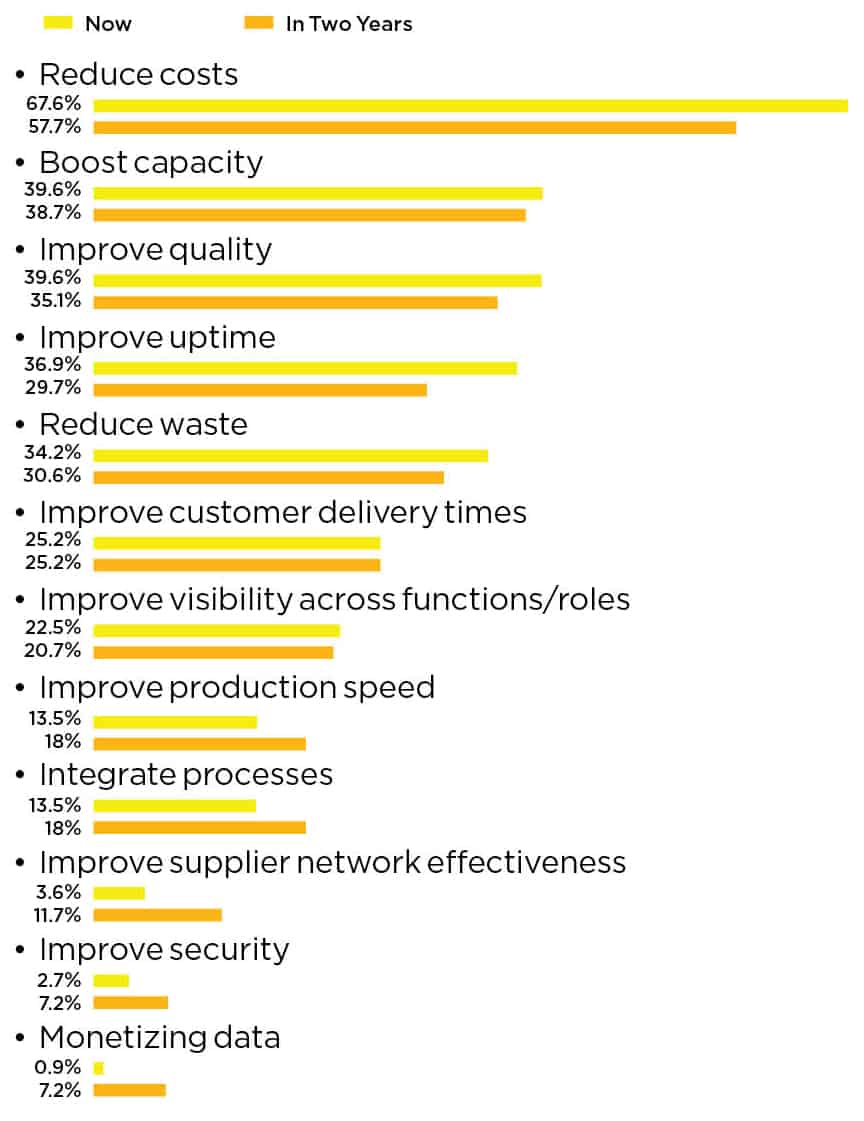

Cost reductions are the primary motivator for new manufacturing data projects now, and this is expected to remain constant in two years. In fact, 65% of 2021 survey respondents anticipated that reduced costs would be a key business outcome objective this time around – a number that tracks closely with the 67.6% that listed reduced costs on this year’s survey. While reduce costs is anticipated to lead the charge again in 2025, the number is anticipated to decrease by 10 percentage points in that time. The biggest upward movers by 2025 are expected to be improved production speed, integrated processes, improved supplier network effectiveness, improved security, and monetizing data.

Q: What are your key business outcome objectives for embarking on new manufacturing data projects today and what do you expect the outcome objectives will be in 2 years’ time? (select top three)

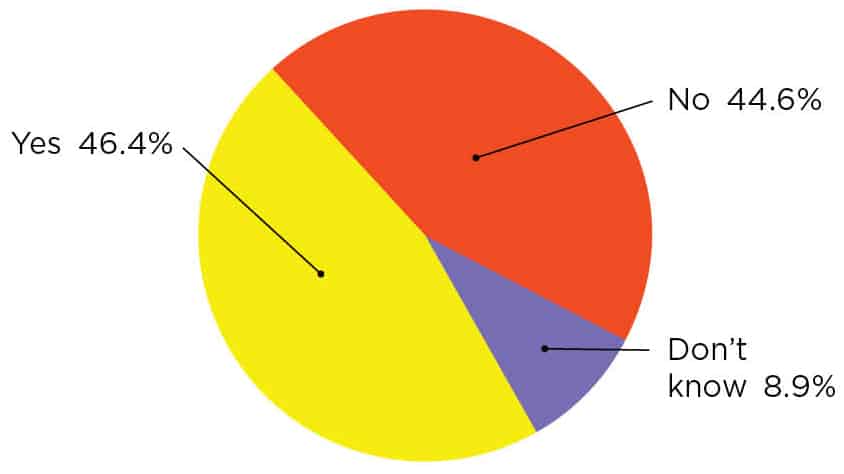

Data improves accuracy and speed of decisions. Half report that decisions have been more accurate and 40% point to more timely decisions. Only 6.3% of respondents report that there has been no change in their company’s decision-making because of data availability, while less than 2% of respondents, respectively, cite slower or worse decisions as the most prevalent way that data has affected their decisions.

Q: What is the most prevalent way that data has affected your company’s decision-making? (select one)

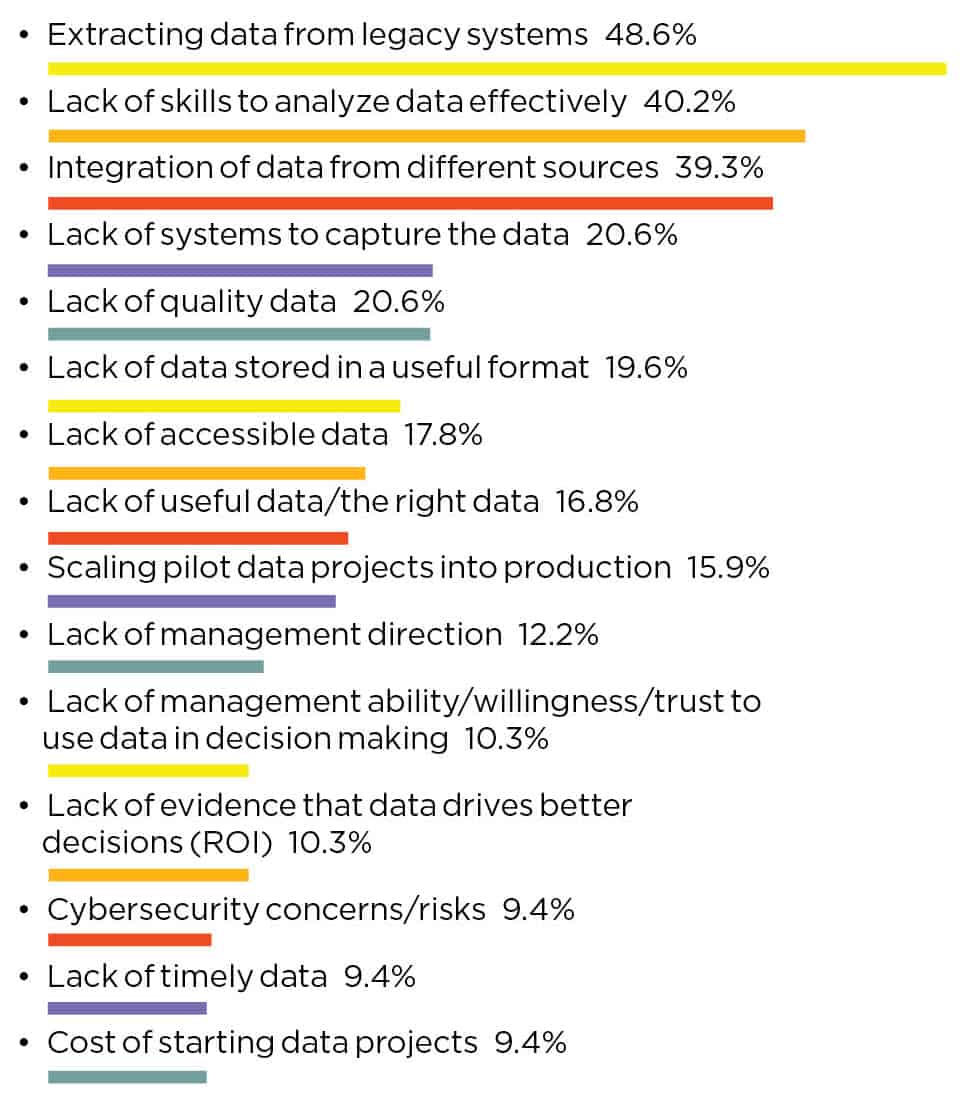

Survey respondents report that many challenges or obstacles are hindering their company from making more data-driven decisions. The leading challenges – each cited by 39-49% of respondents – are extracting data from legacy systems, lack of skills to analyze data effectively, and integration of data from different sources.

Q: What are the most important challenges or obstacles hindering your organization from making more data-driven decisions? (select top three)

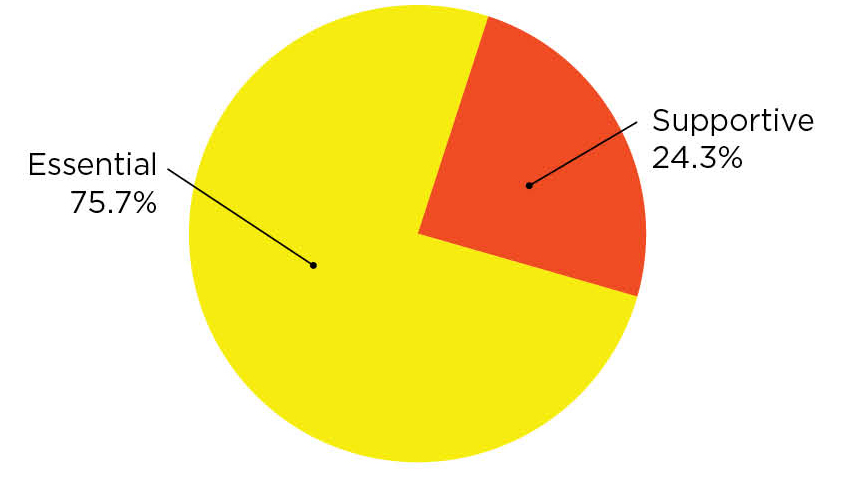

Three out of four respondents report that data mastery is essential to their business competitiveness in the future. This 75%/25% split remains consistent with responses to the 2021 survey.

Q: Looking forward, how important will mastering manufacturing data become to your competitiveness as a future business? (select one)

About the author:

Jeff Puma is Content Director for the Manufacturing Leadership Council

Survey development was led by the MLC editorial team with input from the MLC’s Board of Governors.

Survey: Smarter Factories Are on the Way

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

Survey: Sustainability Momentum Surges Dramatically

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

Survey: More Expect M4.0 Tech Adoption to Increase

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.

SURVEY: Manufacturers Get Tough on Cybersecurity

More companies are taking a disciplined approach to dealing with the growing threat of cyber attacks, a new MLC survey finds.

![]()

The message has been received.

After years of mounting warnings about the risks of being hacked or worse and now faced with a sharply rising number of cyber attacks in the industry, manufacturers have taken concrete steps to fortify their defenses and protect themselves against what is widely assumed will be an even larger threat in the years ahead.

More manufacturers than ever before have put in place formal cybersecurity plans in their companies to deal with threats and attacks. They are significantly increasing their levels of confidence that they have the internal expertise in place to deal with cybersecurity issues. And a majority of companies now have dedicated cybersecurity budgets, including provisions for cyber insurance, and are providing cyber awareness and technical training to their employees.

These are some of the most important findings of the Manufacturing Leadership Council’s new survey on cybersecurity. More than 160 companies expressed their views on cybersecurity strategy in their organizations, whether they have been attacked and what the nature of those attacks were, what measures they have adopted to defend themselves, and how the growing problem of cybersecurity may be affecting their adoption of Manufacturing 4.0 and their transition to the digital model of manufacturing.

Formal Planning Takes Off

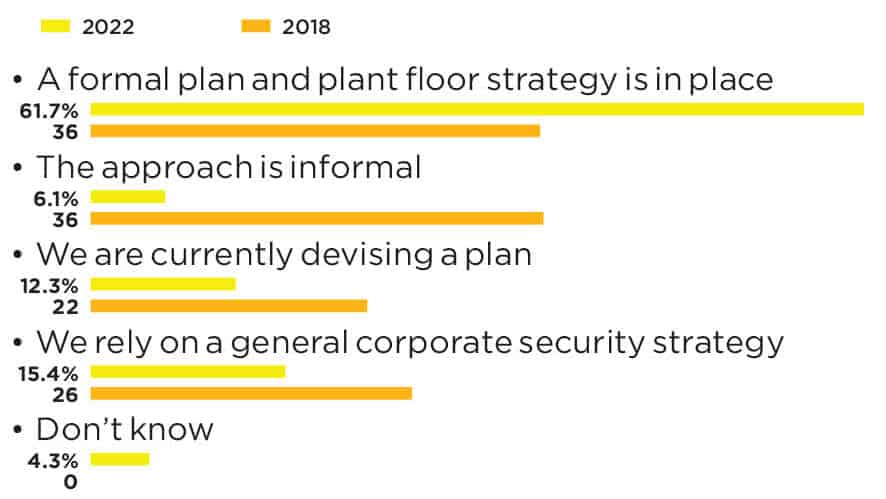

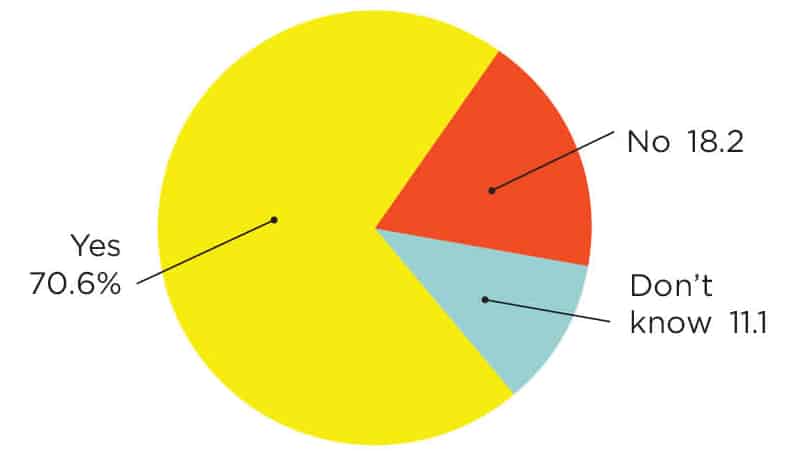

A sea change in how seriously manufacturers consider the cyber threat has occurred at the strategy level. Just four years ago, according to MLC’s 2018 cyber survey, barely one-third of manufacturers had devised and adopted formal cybersecurity plans that encompassed their plant floors. Today, the new MLC survey shows that nearly 62% have put such plans in place (Chart 1).

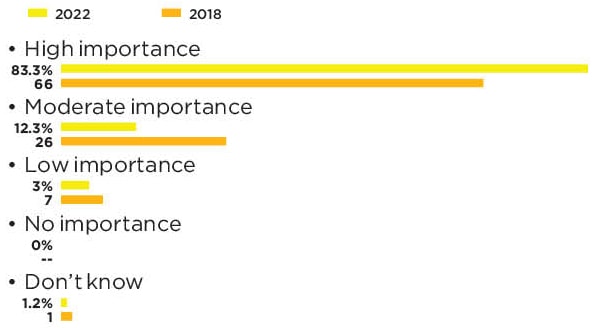

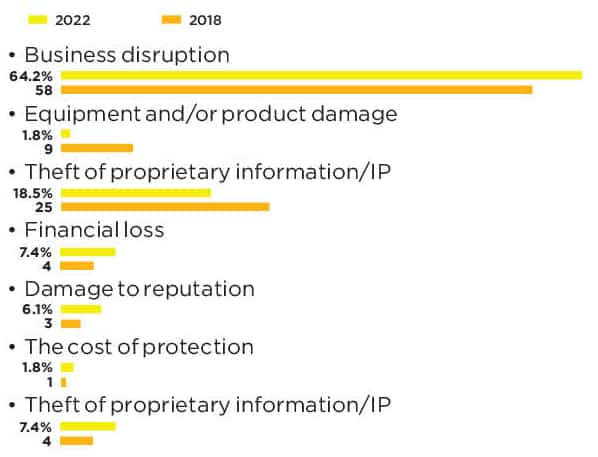

The more serious attitude is directly related to the perceived consequences of cyber attacks. When asked how important cybersecurity is as a business issue, 83% of survey respondents said it is of high importance, compared with 66% saying so in 2018. Moreover, 64% said this year that business disruption is the most significant cybersecurity-related risk to their companies, compared with 58% in 2018. Interestingly, very few fear equipment or product damage from cyber attacks and only 18% this year are worried about the theft of proprietary information (Charts 2,3).

The advent of connected business ecosystems will test current cyber strategies.

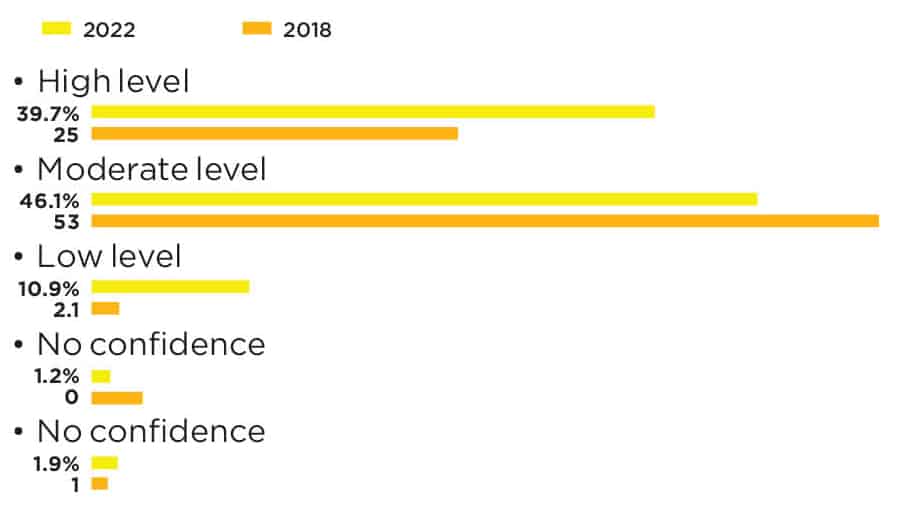

Bolstered by the greater focus on formal planning and now regular awareness and technical training for employees on cybersecurity, a growing number of manufacturers feel confident that they have the internal expertise to deal with manufacturing-related cyber issues. This year, nearly 40% of survey respondents said they had a high level of confidence about their internal expertise, compared with 25% saying so in 2018. Another 46% assessed their confidence levels as moderate this year (Chart 4).

More Attacks Expected

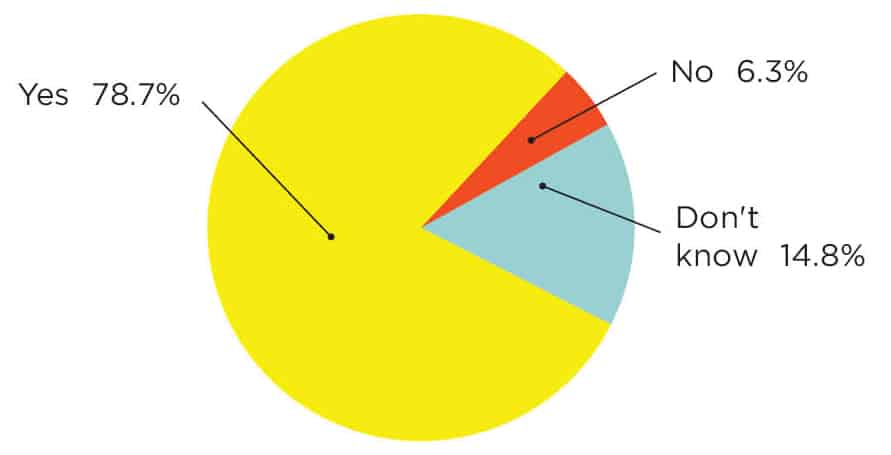

Even as better cybersecurity strategies are put in place and confidence in internal capabilities to deal with threats and attacks grows, an overwhelmingly large number of manufacturers expect more attacks in the year ahead, a perception that is no doubt driving much of the greater emphasis on defensive measures.

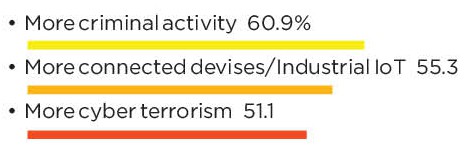

This year, nearly 79% of survey respondents said they expected more attacks in the next year, compared with 64% expressing that feeling in 2018 about 2019 (Chart 8). The three most cited reasons for this expectation are more criminal activity; greater connectivity in their operations, particularly with Internet of Things technologies; and more cyber terrorism (Chart 9). Of least concern: insider- or supply chain-originated attacks. Phishing, malware, and ransomware are the most prevalent methods of cyber attack cited by respondents overall.

When asked to assess the cyber battlefield and its most important points of vulnerability, survey respondents painted an interesting picture of where conflict is most likely to play out.

Mobile devices, e-mail servers, and laptop computers were cited by respondents as having the highest level of cyber vulnerability – not plant floor equipment or plant floor control systems. Looked at from a business function or activity perspective, a similar dynamic – vulnerabilities caused by external connections – was revealed in the survey data. Social media networks, partner and distribution networks, and supply chain networks were the most cited points of vulnerability – not plant floor networks, design and innovation networks, or field service operations. In addition, respondents said their best protected systems are their ERP and MES systems.

More manufacturers than ever have adopted formal cybersecurity plans.

What these findings suggest is that, as manufacturers go about forging so-called business ecosystems of partners, suppliers, and customers that are increasingly digitally connected, they will have to extend existing cyber strategies and tactics or even create new ones to protect these networks in the future. This is perhaps the next frontier in cybersecurity.

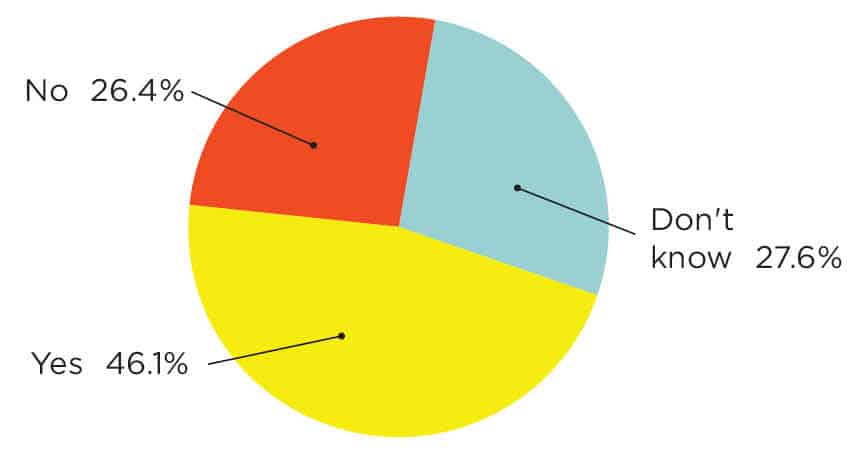

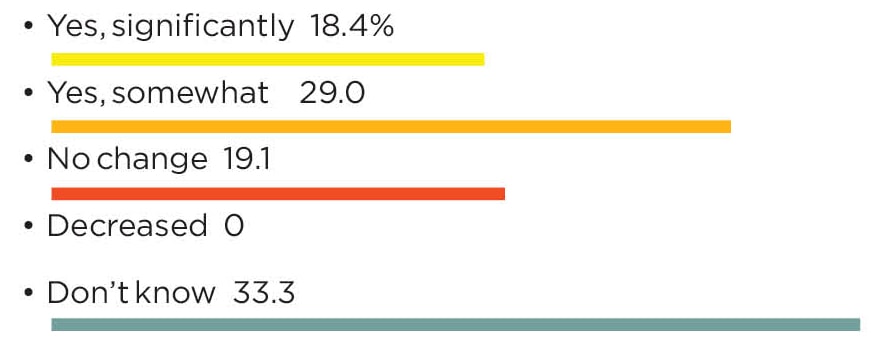

Manufacturers are starting to decode these signals. When asked in this year’s survey whether they have introduced or changed cybersecurity requirements for external partners and vendors with which they share data, 48% said that they had. In addition, 70% said the increase in remote working spurred by the pandemic has caused them to make adjustments to their cyber policies.

The Effects on M4.0

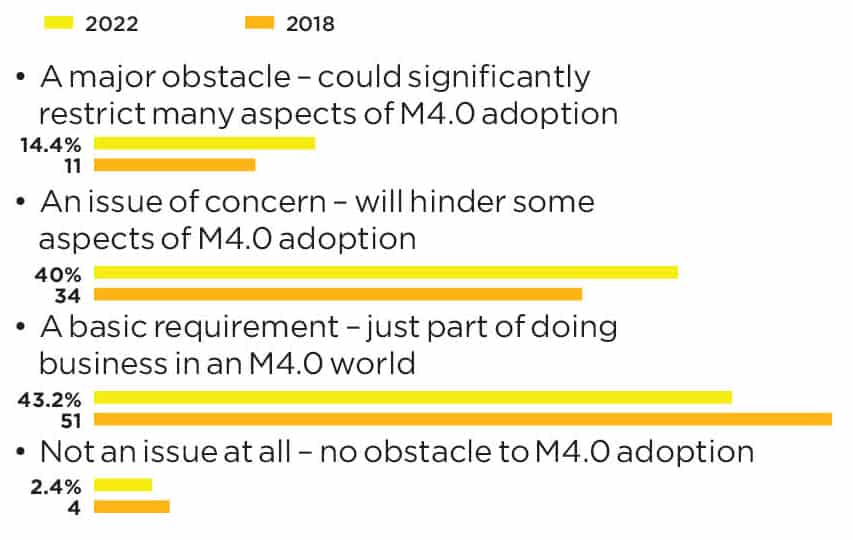

Based on their perception that cyber attacks will increase in the years ahead, more than half of survey respondents expressed concern that cybersecurity issues could affect the speed and scope of adoption of Manufacturing 4.0. Fourteen percent said cyber could be a major obstacle in the next five years, with another 40% describing it as “an issue of concern”. A significant percentage, 43%, consider cyber to be just part of doing business in an M4.0 world (Chart 13).

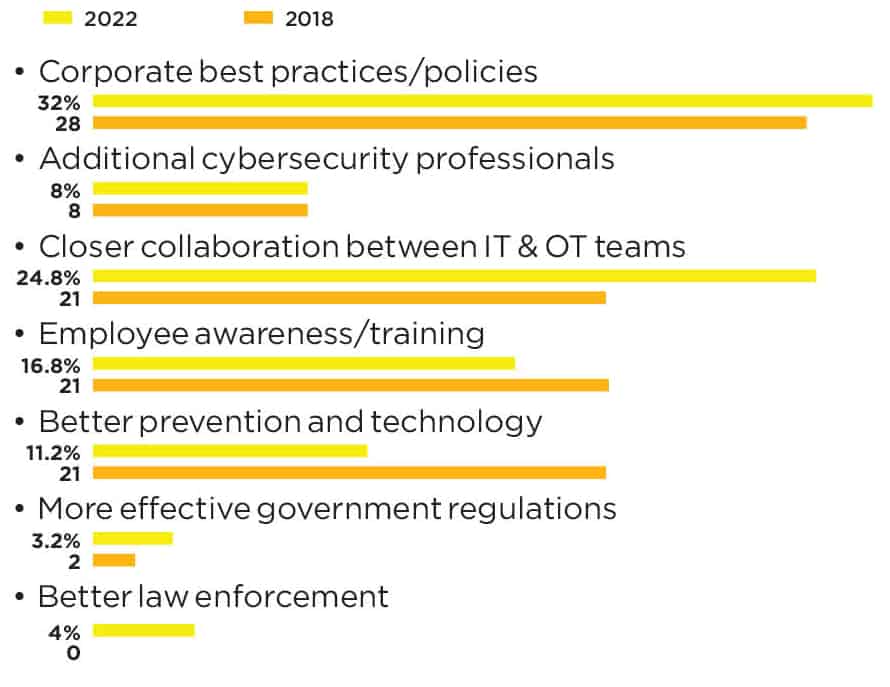

As they devise their defenses, manufacturers are relying more on internal mechanisms, such as corporate best practices and policies and closer collaboration between IT and OT teams, rather than law enforcement or government regulations (Chart 10).

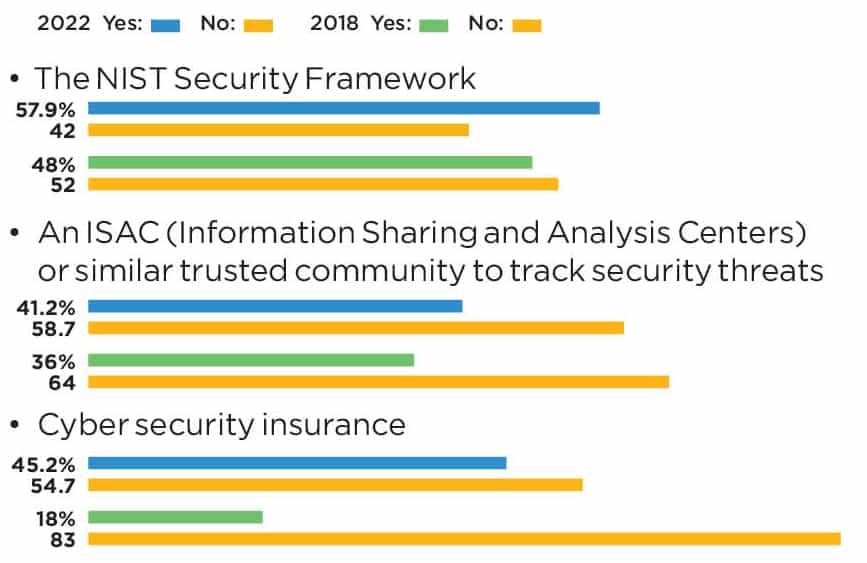

Moreover, more are taking advantage of publicly available approaches, such as the NIST Security Framework, to underpin their strategies. This year, almost 58% of survey respondents said they have adopted the NIST framework, up from 48% in 2018. In addition, there has been a sharp rise in those subscribing to cyber insurance – 45% today, compared with only 18% in 2018 (Chart 12).

All in all, manufacturers have been moving on multiple fronts to combat the growing cyber problem. The challenge for industrial companies going forward will be to try to stay one step ahead as the number and sophistication of attacks increase even as they expand their digital networks outside the four walls of their business. M

Part 1: CYBERSECURITY STRATEGY AND ORGANIZATION

1. Strong Majority Now Have Formal Cyber Strategies

Q: How would you characterize your company’s approach to dealing with manufacturing cybersecurity?

2 Business Issue Concerns Rise

Q: How important is cybersecurity as a business issue to your company, in terms of securely interconnecting systems or exchanging operating data within, or across, your manufacturing sites and partner companies?

3 Business Disruption Still Leads Cyber Risks

Q: What is the most significant cybersecurity-related risk to your company’s manufacturing operations?

4 Internal Expertise Confidence Rises Sharply

Q: What level of confidence do you have that your company has the internal expertise to deal with manufacturing-related cybersecurity issues?

Part 2: MANUFACTURING CYBER ATTACKS AND EVALUATION

5 Nearly Half Have Suffered Cyber Attacks

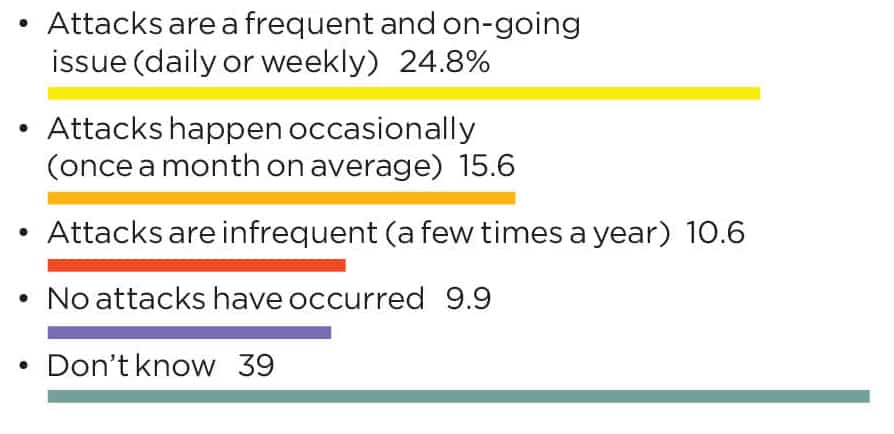

Q: Have your company’s manufacturing sites ever been a target or a victim of a cyberattack?

6 Nearly Half Also Say that Attacks Have Increased in the Last Year

Q: Have attacks directed at your company’s plant systems and networks increased over the past year?

7 Frequency of Attacks is Significant

Q: How would you characterize the frequency of attacks?

8 More than Three-Quarters Expect More Attacks Ahead

Q: Do you expect your company to experience more attacks in the year ahead than in the past year?

9 Criminal Activity Cited as Top Reason for More Attacks

Q: If yes, what’s driving the increase?

Part 3: POLICIES TO DEAL WITH CYBER ATTACKS

10 Corporate Polices Seen as Best Defense

Q: What do you think will help the most in improving manufacturing cybersecurity in an M4.0 world?

11 Remote Work Has Forced Cyber Policy Changes

Q: Has an increase in remote work required any new changes or adjustments to your cyber policies?

12 NIST Framework is More Widely Adopted

Q: Are you engaged in, or have adopted, any of the following approaches as a way to better protect your company or mitigate cyber risks?

Part 4: THE FUTURE ORGANIZATION

13 Concerns Rise on Effect of Cyber on M4.0

Q: Over the next 5 years, how much of an obstacle will cybersecurity issues be to the speed and scope of adoption of Manufacturing 4.0 technologies and approaches?

About the author:

David R. Brousell is the Co-Founder, Vice President & Executive Director of the Manufacturing Leadership Council.

Survey development was led by David R. Brousell, with input from the MLC editorial team and the MLC’s Board of Governors.

SURVEY: Digital Leadership Playbook Still Work in Progress

Manufacturing Leadership Journal content and MLC resources are exclusively available to MLC members. Please sign up for an account or log in to view this content.